Otaviano Canuto, IMF: How Commodity-Dependent Are Latin American Economies?

The end of the upswing phase of the commodity price super-cycle, after its peak in 2011, has lowered economic growth prospects in most of Latin America. While that broad statement can hardly be disputed, Chapter 3 of the latest IMF Western Hemisphere Regional Economic Outlook calls attention to underlying significant differences among countries in the region. Growth implications of the commodity price evolution have varied substantially as a result of commodity-specific price patterns and country-specific exposures and composition of commodity specialisation.

The end of the upswing phase of the commodity price super-cycle, after its peak in 2011, has lowered economic growth prospects in most of Latin America. While that broad statement can hardly be disputed, Chapter 3 of the latest IMF Western Hemisphere Regional Economic Outlook calls attention to underlying significant differences among countries in the region. Growth implications of the commodity price evolution have varied substantially as a result of commodity-specific price patterns and country-specific exposures and composition of commodity specialisation.

Commodity-Specific Super-Cycles

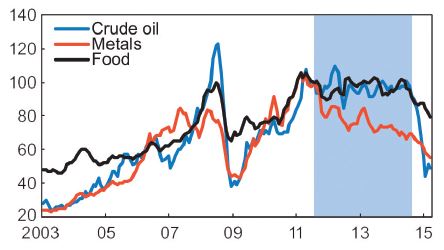

Figure 1 depicts the three broad groups of commodity prices as following an overall common cyclical path since 2002. After a strong upswing lasting until the 2008 financial crisis, and a subsequent recovery from the plunge, mid-2011 has been dubbed the “sunset of the super-cycle”. Prices definitely ceased to climb during the plateau period (shaded area) and the three groups have all moved to lower levels after mid-2004.

However, Figure 1 also shows that evolution is taking place with different intensities. As we highlighted two years ago (Canuto, 2013), the dynamics of fundamentals in terms of relative supply and demand trends in the markets for each group were then divergent enough to lead to differences like those identified during the plateau period. In the case of crude oil, sector-specific supply-side developments were responsible for the sudden fall during the second half of 2014. The differentiation is starker when one disaggregates the three groups.

Figure 1: Commodity prices. (Index: July 2011 = 100) Note: The shaded area corresponds to the plateau period referred to in the text. Source: IMF, World Economic Outlook database.

A net exporter (importer) of a commodity enjoys (suffers from) a manna-from-heaven gain (thunder-from-heaven loss) when its price increases. The extent to which that price retreats back after the end of the upswing phase determines how much of that gain (loss) is reduced – or even possibly reversed. Therefore, country-specific impacts of the commodity price super-cycle have depended on which commodities – and how much of each of them – a country exports and imports.

The IMF Regional Outlook brings estimates of country-specific “commodity terms of trade” (CTOT) indices across the region. Those are indices in which price changes of individual commodities are weighted according to their (net) export value, and are then normalised by GDP. A certain increase (decrease) in CTOT is thus a way to gauge the net gain (loss) of commodity price movements in GDP terms.

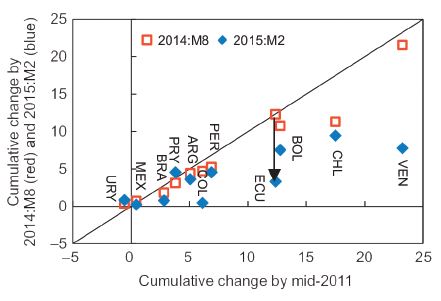

Figure 2 exhibits cumulative changes in CTOT indices from average levels in 2002 to mid-2011 (the sunset of the super-cycle), August of 2014 (when the sudden plunge of oil prices started), and February of 2015. At least four aspects come to the fore:

Figure 2: Commodity Terms of Trade, 2013-2015. (Cumulative change in CTOT indices from average levels in 2002; percentage points of GDP) Note: CTOT = Commodity Terms Of Trade. Source: IMF, World Economic Outlook database; UN Comtrade; and IMF staff calculations.

- As one can see on the horizontal axis, except for Uruguay, all Latin American countries therein derived GDP gains from the upswing phase. The ascent stage of the cycle was a potential economic blessing for most of Latin America.

- Baskets of commodity exports and imports determined how much of that gain was retained during the plateau period (red squares) and afterwards (blue diamonds). This follows from different compositions of commodity specialisation regarding metals, food, and oil and their diverging price patterns over time.

- Commodity prices have not in general declined to levels below those in 2002 and, therefore, the manna-from-heaven gains accrued until now have not been completely reversed. However, those gains were accrued in past and current GDP levels, while the contribution of commodity price shocks to GDP growth rates has become negative after the price peak. Positive commodity price shocks have multiplier-accelerator effects beyond changes in CTOTs. Provided that they are seen as permanent or prolonged, they spark investments that benefit directly or indirectly from them. Both potential and actual GDP move up as compared to the absence of shocks. Broad asset price hikes and capital flows may also follow. Nevertheless, once positive shocks fade out and corresponding multiplier-accelerator effects have run their course, there will be a deceleration of output growth even if prices stay high.

- Magnitudes in GDP relative of terms-of-trade gains, and their subsequent partial unwinding along the cycle, have varied substantially among countries. First-order impacts as measured in Figure 2 do not tell the whole story of implications of commodity price cycles for a country’s economy. Second-order effects – like above-mentioned investments, asset price cycles, capital flows, and others – depend on sector- and country-specific features in addition to CTOT changes. The nature of economic policies accompanying price shocks can also – positively or negatively – magnify the impacts of those CTOT movements. However, even taking these factors into account, the discrepancies in quantitative relevance of the commodity price super-cycle still look very significant between, say, Venezuela and Chile on the one hand, and Brazil, Mexico, and Paraguay on the other.

Take the case of Brazil. It is true that ups and downs in neighbours’ economies more cyclically affected by commodity prices also weighed on its performance as a consequence of their relevance as markets for Brazilian manufactured products. However, it looks hard to state that the recent performance and macroeconomic prospects of Brazil can be predominantly explained by the commodity price super-cycle.

About the Author

Otaviano Canuto is the executive director at the Board of the International Monetary Fund (IMF) for Brazil, Cabo Verde, Dominican Republic, Ecuador, Guyana, Haiti, Nicaragua, Panama, Suriname, Timor Leste and Trinidad and Tobago. Views expressed here are his own and do not necessarily reflect those of the IMF or any of the governments he represents.

Otaviano Canuto is the executive director at the Board of the International Monetary Fund (IMF) for Brazil, Cabo Verde, Dominican Republic, Ecuador, Guyana, Haiti, Nicaragua, Panama, Suriname, Timor Leste and Trinidad and Tobago. Views expressed here are his own and do not necessarily reflect those of the IMF or any of the governments he represents.

Mr. Canuto has previously served as vice president, executive director and senior adviser on BRICS economies at the World Bank, as well as vice president at the Inter-American Development Bank. He has also served at the Government of Brazil where he was state secretary for international affairs at the ministry of finance. He has also an extensive academic background, serving as professor of economics at the University of São Paulo and University of Campinas (UNICAMP) in Brazil.

Note from the author: adapted from my presentation at the Workshop on Commodity Super Cycles, jointly organised by the Bank of Canada and Federal Reserve Bank of Dallas, Ottawa, at the Bank of Canada Headquarter on 27-28 April 2015.

The views expressed are those of the author and do not necessarily reflect the views of the IMF.

You may have an interest in also reading…

Finding the Inside Track to Sustainable Investment — it’s a ThirdWay Speciality

ThirdWay Partners, with offices in Kenya, London, Mozambique, South Africa and Spain, and expanding its presence in Argentina this year,

Economy has ‘Turned a Corner’ as UK Emerges from Recession

The UK economy has emerged from a recession fuelled by stronger-than-expected growth between January and March, according to official figures

Vector Casa de Bolsa: Five Decades Driving the Growth of the Mexican Economy

As Vector Casa de Bolsa approaches its 50th anniversary, it is time to reflect on the company’s remarkable journey and enduring impact