Big Slowdown in Chinese Economy Calls for Tweaks to ‘Rebalancing’

Chinese economic figures released August 1 show a slowdown in growth. New Omicron outbreaks — in the context of the zero-Covid policy — the housing slump and heat waves have been decelerating the nation’s pace.

Chinese economic figures released August 1 show a slowdown in growth. New Omicron outbreaks — in the context of the zero-Covid policy — the housing slump and heat waves have been decelerating the nation’s pace.

This is another step in the trend of gradually declining rates that has accompanied the “great rebalancing” since the early 2010s. One major difference is the perception of exhaustion from waves of overinvestment in real estate and infrastructure.

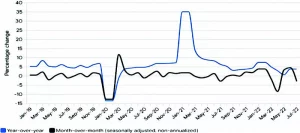

The economy started out strong in January-February, but negative shocks led to a contraction in GDP by an estimated 5.4 percent in the second quarter. Industrial production grew 3.8 percent in July over the previous year, below the expected 4.5 percent (Figure 1). GDP growth estimates by several international banks for the world’s second-largest economy this year have been revised down to levels between 2.5 and 3.3 percent.

A scorching, dry summer is stressing energy supplies and leading to production cuts in some provinces and energy-intensive sectors.

The real estate crisis continues to undermine economic performance. Housing is an important component of fixed investment. It grew by just 5.7 percent in the first seven months of 2022, compared to the same period in 2021. Last year, that number was 10.3 percent higher year-on-year.

Property sales are expected to decline about seven percent, and construction to fall about 30 percent, in the second half of this year. The real estate slowdown was driven by the policy choice to reduce developers’ leverage and achieve a long-term objective “for housing, not for speculation”. Banks, regulators, and local governments will have to stick to this policy — and a general bailout is not on the cards. There is an expectation that adjustments to balance sheets of companies and customers and suppliers in the sector will not result in systemic crises, despite occasional defaults and bankruptcies.

-

- Figure 1: China’s Industrial Production Growth Declined Last Month. Industrial production growth declined in both year-over-year and month-overmonth terms in July. Source: NBS. CEIC. Goldman Sachs Research.

-

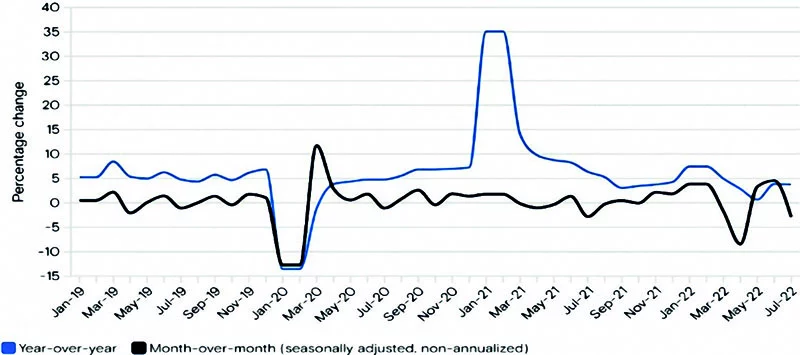

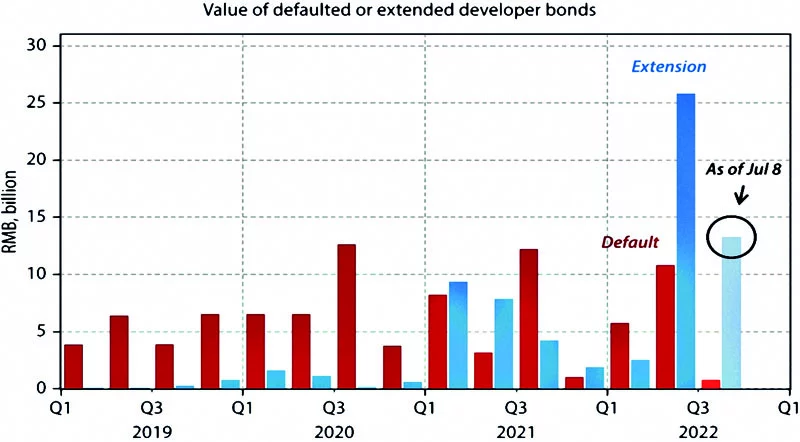

- Figure 2: China – developer bond repayment bond issues are not getting better. Source: Zhang, X. (2022). The Financial Stress from Property Spreads, Gavekal Dragonomics, July 13th.

-

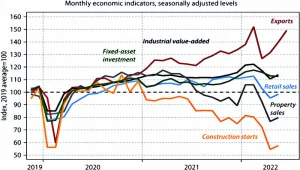

- Figure 3: Exports aside, the rebound of lockdowns has been very lackluster. Source: CEIC, Gavekal Dragonomics Macrobond, July 14th, 2022 (Thomas Gatley, Webinar on China).

-

- Figure 4: China – credit and M2 money supply (% increase on a year earlier).*Total Social Financing. Source: The Economist, August 18th, 2022.

-

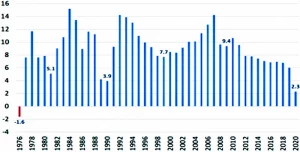

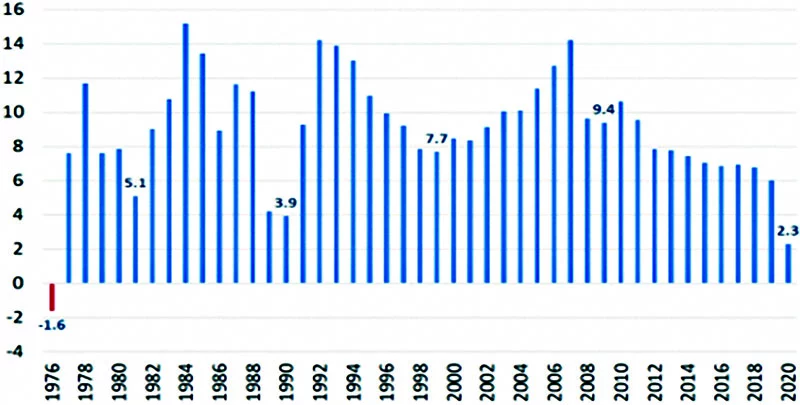

- Figure 5: China – annual GDP growth rates. Source: CEIC.

-

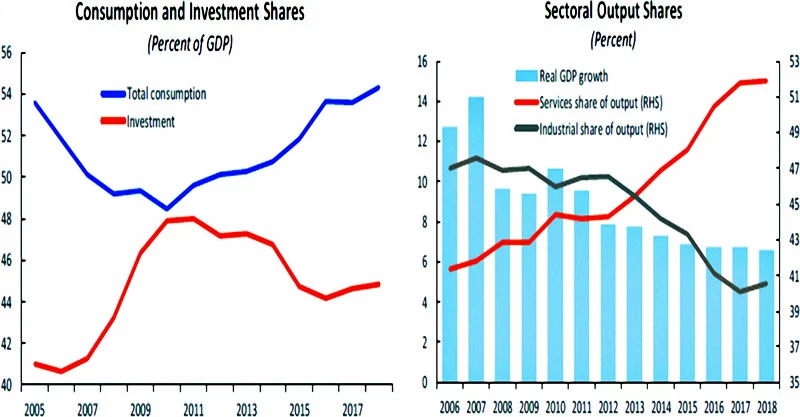

- Figure 6: China’s rebalancing toward consumption and services. Source: Aasaavari, N. et al (2020).

-

- Figure 7: China’s rebalancing toward less export-dependence. Source: IMF (2020).

-

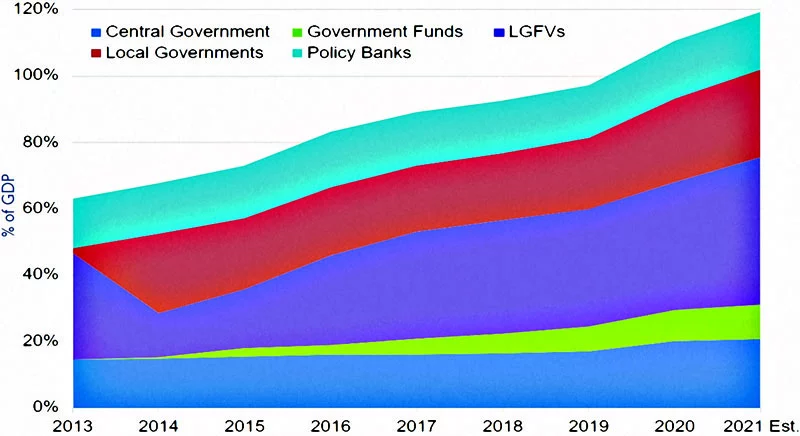

- Figure 8: China’s total government debt, by source 2013–2021 (Est.). Source: Borst (2022).

-

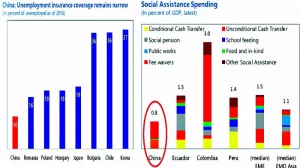

- Figure 9: Unemployment insurance coverage and social assistance spending. Source: IMF (2020).

-

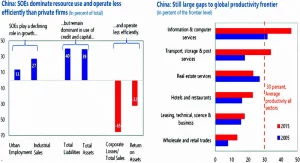

- Figure 10: China’s rebalancing – SOEs and POEs. Source: IMF (2020), People’s Republic of China, Staff Report for the 2020 Article IV Consultation, November.

Financial stress on highly indebted property developers has increased over recent years. Many were unable to refinance in bond markets in 2021, and several have either negotiated repayment extensions with creditors or defaulted. As shown by Zhang, many creditors have agreed to negotiate repayment extensions ahead of potential defaults to give developers more time. (Figure 2).

The impact of the Omicron wave on China’s economic growth was significant, especially in regions subject to lockdowns. Retail sales in July were up just 2.7 percent year-on-year, far below expectations of five percent. New Covid outbreaks and the risk of confinement affected retail trade and domestic tourism.

Since 2020, household consumption has remained weak, persistently below the 2017-19 trend (Gatley, 2022). The labour market has been very soft, which does not help.

Strictly speaking, only exports maintained a good pace (Figure 3). Trade has recovered faster than domestic activity since the reopening began with streamlined logistics and transport. Production and investment are outpacing consumption and services; factory reopening has been a higher priority than the relaxation of individual mobility restrictions.

Factory activity has rebounded more quickly than expected, with exports posting the highest growth rate in a year this June. In contrast, indicators of the purchasing decisions of households have lagged. Such a pattern runs against the “rebalancing” pursued by Chinese authorities since the beginning of the last decade.

Despite the slowdown, the measures taken by the government can be considered modest. The People’s Bank of China cut two major interest rates in mid-August — the repo interest rates on one-year and seven-day open market operations — by 10 basis points. On August 22, it announced a 15bp cut in the five-year interest rate, lowering it to 4.3 percent, while the one-year rate was reduced by another 5bp to 3.65 percent.

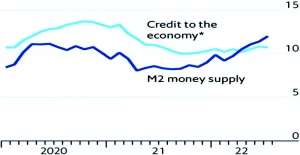

Analysts do not believe such rate reductions, or other newly announced incremental fiscal measures, could significantly boost economic growth. The increases in the monetary base (M2) since last year have not been accompanied by an equivalent expansion of domestic credit (Figure 4), denoting the presence of dampening factors underlying the slowdown in investments – certainly in the real estate area, given the fragile situation of firms in the sector and the demand for its products.

China’s Great Rebalancing

To understand Chinese economic growth, it is necessary to go back to December 2011. At that time, I was one of the vice-presidents of the World Bank, and attended a ceremony in Beijing in which then-president Hu Jintao made one of the first statements on the need for that “rebalancing”.

There would have to be a gradual redirection towards a new pattern of growth, in which domestic consumption should increase in relation to investments and exports. An effort would also be made to consolidate value added in global value chains. Services should also increase their weight in GDP relative to manufacturing. China would no longer have the double-digit GDP growth rates of previous decades (Figure 5), but growth would no longer be, as Premier Wen Jiabao had said in 2007, “unstable, unbalanced, uncoordinated and unsustainable”.

High and sustained growth rates had been based on elevated investment-to-GDP ratios — which were only possible with low shares of wage income and domestic consumption, as well as with cheap and repressed finance.

Another factor was that dynamic markets abroad were willing to absorb an expansion of Chinese exports. The combination of high investment and low domestic consumption (a flipside of high profits relative to wages) was only possible because of current-account surpluses in global trading.

Growing income disparities were the domestic flipside of that, a potential source of social strain along with changes in the external environment.

Three mutually reinforcing paths of transformation were seen ahead in 2011, with a structural growth slowdown on the cards.

First, those gains had, to a large extent, already happened by transferring resources from low-productivity agriculture activities to industry. On the demographic front, the old-age-dependency ratio had started to rise. Gains in economic efficiency and technological progress — based on the absorption of existing, imported technologies — would have to be replaced with local innovation. The set of second-generation policy reforms necessary for that would require time.

As a second path of change, a rebalance in the sector structure and in aggregate-demand-composition was expected. Higher shares of services and consumption, following rising wages, with a decrease in exports, savings, and investment ratios-to-GDP, should accompany the increased reliance on domestic sources of aggregate demand.

The income gap between coastal areas, where special zones were created and extended, and middle and western regions should fall with the shrinking labour pool. Despite lower GDP growth and total factor productivity increases being harder to obtain, the popular perception of rising prosperity would probably be higher than before, with increasing purchasing power by the population.

The third path of structural transformation would be a shift up the value chain in tradable and non-tradable activities. That should underpin the directions of change in the sector structure and components of aggregate demand. A transition to more sophisticated production processes was under way.

While moving in a less spectacular trajectory, China would morph into a mass-consumer market economy, combined with supply capacity increasingly reliant on the growth of “total factor productivity”.

Having a clear roadmap did not mean an easy ride. Given the low level of domestic consumption in GDP and the dependence on investments and trade balances, the transition risked experiencing an abrupt slowdown. Waves of credit-driven over-investment in infrastructure and housing followed in a bid to allay fears of a downturn.

The second round of such over-investments came in 2015–2017, in response to a downturn in real estate and the stock market. These were the expansion policies adopted during the pandemic crisis in 2020.

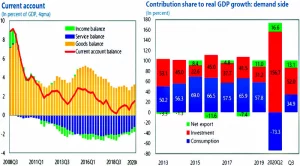

A decline in GDP growth rates, to six percent in 2019, headed towards levels expected after the pandemic (Figure 5). And the gradual reduction of dependence on investment and trade surpluses can be seen in Figures 6 and 7.

The left-hand panel of Figure 6 depicts how domestic demand started shifting away from investment and towards consumption. The right-hand panel shows services outgrowing manufacturing as the production structure became more complex, integrated, and with higher added value.

That is a challenge, and a transition to a less investment- and export-dependent growth model has been coming from a starting point of exceptionally low consumption-to-GDP ratios. No wonder rebalancing toward a consumption-based growth model was expected to be only gradually pursued — GDP growth rates might collapse. The change in growth pattern would require time-intensive structural reforms.

The left-hand panel of Figure 7 displays the decrease of the role played by current-account surpluses with the rest of the world as part of China’s growth rebalancing. 2020 was a point off the curve. China’s current-account surplus narrowed in Q1, but widened again to 1.5 percent of GDP over four quarters ending in Q3, reflecting a more robust trade balance and a collapse in outbound tourism. The right-hand panel shows how rebalancing towards consumption regressed as public investment drove the 2020 first phase of after-pandemic recovery — and the reopening after the Q1 lockdown favoured industrial activity.

A harder question is how the gradual evolution of GDP growth and changes in composition since 2010 would have performed in the absence of real estate over-investment. It counted only on the rebalancing, an increase in wages and mass domestic consumption, and the transition to greater weights of services and higher technology.

This matters — there is a perception that over-investment, as a growth lever, has declined in importance. Not only because of the debt levels, particularly via local government financing vehicle debt (LGFVs in Figure 8), but also because its returns in terms of GDP growth showed a lower contribution.

Chinese authorities are now choosing to safeguard their economy from financial vulnerabilities, even at the price of GDP growth below official targets.

Growth Challenges Ahead

The domestic consumption-to-GDP level remains low, which is a challenge. In addition to the high proportion of profits concerning wages, low levels of public spending on the social safety net have led to high household savings. As depicted on the left-hand panel of Figure 9, the coverage of the unemployment insurance system is minimal — even thinner in rural areas. Only 10 percent of 23 million unemployed workers received benefits in 2016.

Spending on social assistance and public health care is low. China’s aggregate welfare and health expenditures are only about 3.5 percent of GDP, less than the average of its emerging market peers (Figure 9).

Another challenge will be in climbing the tech and value-added ladder. China has done its homework in terms of investments in education, infrastructure, etc., to absorb this. In priority sectors, firms have continued to increase their capital expenditure. China has now reached the top of the ladder in many sectors, where “tacit and idiosyncratic” technology content must be locally developed. The new normal of the global economy — post-pandemic and with the war in Ukraine — is an environment less friendly for China to delve in overseas technology.

China should resume the rebalancing between public and private companies (SOEs and POEs) in service sectors (Figure 10, right-hand panel).

The rebalance has stalled, and progress in reforming SOEs has seen limited progress. Credit is still preferentially channelled to state businesses, which enjoy implicit guarantees. Competition between private firms and state-owned enterprises remains uneven. While large state-owned banks keep lending to SOEs, infrastructure and real estate investments had been supported by shadow finance.

SOE “deleveraging” has paused, reflecting the pandemic effect. What matters here is to call attention to the fact that the performance indicators on the left-hand panel of Figure 10 suggest that the absence of significant reform of SOE businesses has come at a cost in terms of productivity and real returns. According to the IMF, the average productivity gap between SOEs and private enterprises across sectors is about 20 percent.

China has seen remarkable growth over recent decades, but average sectoral productivity remains at about one-third of the global frontier. Productivity gaps are huge in the services sector. Business services productivity stands at just 17 percent of the frontier level, largely because of high entry barriers. Addressing these gaps would mean opening non-strategic sectors such as services to private firms — domestic and foreign. Removing regional regulatory barriers would help to increase competition and factor allocation by facilitating firm entry and mobility across regions and sectors.

These productivity gaps have significant implications for the level of GDP considering the SOE sector’s dominance in the use of resources. The IMF refers to a staff analysis suggesting that reforms closing productivity gaps between SOEs and POEs across sectors could raise output by around four percent.

It is worth recalling the debt legacy of the three previous waves of over-investment in housing and infrastructure. Safeguarding against financial crashes will mean less use of them to boost growth ahead.

Bottom Line

China’s economic growth will keep sliding. The rest of the world can no longer count on it as an engine of growth. But given the size of its economy and its growth rates at the margin, it will remain a fundamental component of the global economic dynamics. i

First appeared at Policy Centre for the New South.

About the author

Otaviano Canuto, based in Washington, D.C, is a senior fellow at the Policy Center for the New South, a nonresident senior fellow at Brookings Institution, a visiting public policy fellow at ILAS-Columbia, and principal of the Center for Macroeconomics and Development. He is a former vice-president and a former executive director at the World Bank, a former executive director at the International Monetary Fund and a former vice-president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at University of São Paulo and University of Campinas, Brazil. Otaviano has been a regular columnist for CFI.co for the past ten years.

Follow him on Twitter: @ocanuto

You may have an interest in also reading…

Could Elon Musk Revolutionise Social Media by Acquiring TikTok?

The U.S. operations of TikTok face an uncertain future as the Supreme Court prepares to rule on a potential ban

China Syndrome: A Wilting Economy, Financial ‘Long-Covid’, a Collapsing Property Sector — and the Spectre of Deflation Hovering Nearby

The global economy is supported by four pillars; two are wobbly, reports Wim Romeijn, and one is being rebuilt. The

On Freeters and Other Exotic Creatures in a Land of Plenty

The sustainability of Japan’s society is in doubt for various reasons, writes Wim Romeijn. China, Europe, and even the United