Africa

Back to homepage

Tunis International Bank: The Bank of the Region

Established as the first private non-resident commercial bank in Tunisia since 1982, TIB has earned its reputation as a local provider of high-quality products and services for internationally oriented clients. Its coverage spans corporates, financial institutions, governments and individuals in

Read More

Orchestrating the Transition: enso Group Builds the Enabling Structures for Reliable Clean Power

From Austria’s hydropower tradition to African grid-scale platforms, enso’s “system orchestrator” model fuses technology, finance and governance into investment-ready energy ecosystems that deliver dependable, independently sourced renewable power. In an energy world defined as much by complexity as by ambition,

Read More

Angola’s Transport & Infrastructure Evolution: Rebuilding a Nation, Rewiring a Region

Few African countries have pursued infrastructure renewal on Angola’s scale or under comparable historical pressure. Emerging from decades of civil conflict in the early 2000s, the country confronted an all-encompassing reconstruction agenda: roads and bridges, ports and railways, airports and

Read More

Eaglestone Management: Experience Forged in Global Infrastructure Finance

Eaglestone’s leadership team reflects the firm’s positioning at the intersection of banking discipline and real-economy delivery. With deep roots in international project finance and a long track record across infrastructure, energy, transport and concessions, the management combines capital markets fluency

Read More

The Pivot: Unlocking the Central African Republic’s Substantial Resource Frontier

The narrative of the Central African Republic (CAR) has long been confined to the periphery of global financial discourse, often cited as an example of a fragile state marked by landlocked isolation and instability. However, developments in early 2026 indicate

Read More

From Penetration to Inclusion: How CRC Credit Bureau Is Re-Engineering Nigeria’s Credit Ecosystem

Nigeria’s journey towards broad-based financial inclusion has accelerated markedly in recent years, with credit penetration emerging as one of the most telling indicators of structural progress. Once constrained by fragmented data, limited formal participation, and low consumer awareness, the country’s

Read More

Leadership at the Helm of Kenya’s Renewable Power Champion

KenGen’s executive team brings together deep technical expertise, financial discipline, legal rigour and strategic foresight to steer East Africa’s foremost electricity generator through an era of energy transition, sustainability and growth. Eng Peter Njenga Managing Director and CEO Born in

Read More

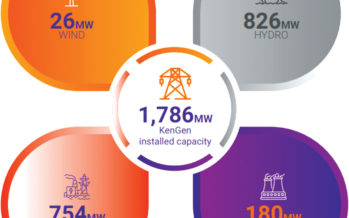

KenGen Powering East Africa’s Clean Energy Future

Kenya Electricity Generating Company PLC (KenGen) stands as East Africa’s leading power producer, entrusted with the mandate to develop, manage and operate the power plants that underpin Kenya’s economic and social life. The company’s vision is to be the market

Read More

Africa Finance Corporation: Powering Africa’s Future Through Pragmatic Investment and Infrastructure

The Africa Finance Corporation is redefining development on the continent by championing bankable, climate-resilient, and inclusive infrastructure projects. With US$17bn invested across 36 countries, AFC is a model of how strategic capital and partnerships can catalyse Africa’s sustainable growth. In

Read More

Samaila Zubairu: Championing Africa’s Economic Transformation Through Infrastructure Investment

Under the stewardship of Samaila Zubairu, the Africa Finance Corporation has become a driving force for industrialisation, clean energy and pan-African prosperity. Samaila Zubairu, President and Chief Executive Officer of Africa Finance Corporation (AFC), has established himself as one of

Read More