Otaviano Canuto: The Multiple Frontlines of the US-China Technological Rivalry

The United States leads in most fundamental advanced technologies, while China leads in practical implementation. China has reduced its technological reliance on advanced economies, while acquiring key positions in some supply chains. Network installation in countries of the South make them a frontline of technological rivalry between the U.S. and China.

Climb the Ladder to the Top On Your Own

China has so far been one of the successful cases of countries coming from below to upper levels of the income ladder during globalization times (Canuto, 2021). For that to happen, it combined the access to technology made available through globalization with the homework of accumulating local and idiosyncratic technological capabilities (Canuto, 1995). An ascent of local production along value chains was the result.

In turn, when, in 2019, the first Trump administration imposed restrictions on market access and technology for all subsidiaries of the Chinese group Huawei, as well as for the company ZTE, we observed that this would be only the opening salvo of a confrontation destined to endure (Canuto, 2019).

It was as if the US were sending this message to China:

“You have made good use of the opportunities to climb the ladder of technology and income, combining the technological availability provided by globalization with investments in your own capabilities, but you will have to climb the rest of the ladder alone.”

Indeed, since then we have witnessed a Chinese investment effort aimed at reducing dependence on external technological frontiers in various areas. We have addressed the cases of semiconductors and clean energy, including the refinement of critical minerals and rare earth upstream by China (Canuto, 2023). US export controls on advanced chips and manufacturing tools slowed China down at the technological frontier but did not prevent its progress. In some cases, they accelerated China’s effort to develop domestic alternatives.

The possibility of renewed Chinese access to advanced semiconductors, as well as US access to critical minerals and rare earths refined by China, allowed the two countries to holster their trade weapons in October last year (Canuto, 2025)

Technology as the Axis of Rivalry

Technology has become the main stage of strategic competition between the United States and China. Technology is no longer just a driver of productivity and economic growth: it is the “central control panel” that determines military capability, economic influence, data management, and geopolitical influence, even with global supply chains remaining deeply interdependent (Goldman Sachs, 2025).

The technological race between the US and China is now the organizing axis of their broader strategic rivalry, with the US still leading in cutting-edge innovation. However, China is rapidly gaining ground, especially in applied implementation, infrastructure, and control over essential physical inputs such as refined critical minerals and rare earth elements, as well as energy.

What is the Current State of this War?

In an interview for Goldman Sachs (2025), Mark Kennedy highlights four key arenas in this race:

“Technological innovation, practical application of the technology, installation of the digital plumbing or infrastructure underpinning the technology, and technological self-sufficiency.”

While the US remains a leader in most fundamental advanced technologies—such as cutting-edge semiconductors, artificial intelligence (AI) frameworks, cloud computing infrastructure, and quantum computing—China is rapidly closing the gap or leading in other critical dimensions. American companies dominate chip design, key semiconductor manufacturing equipment, and the development of the most advanced AI models. The US also benefits from capital markets that attract resources from the rest of the world and a strong system of research universities capable of attracting global talent (at least until the self-inflicted restrictions on such labor entry in the country since the start of the Trump 2.0 administration).

On the other hand, the US faces some domestic constraints, including shortages of skilled labor for advanced manufacturing, high factory construction costs, fragmented power grids, and regulatory hurdles that slow the implementation of infrastructure projects.

China leads in the practical implementation of technologies, benefiting from scale and coordination. This is seen in the use of robotics in manufacturing on a scale twelve times greater than that of the US (Goldman Sachs, 2025) and in physical applications of AI, such as autonomous vehicles and drones, as well as in large-scale digital infrastructure installations.

Frontlines of the Technological Race (1): Semiconductors and AI

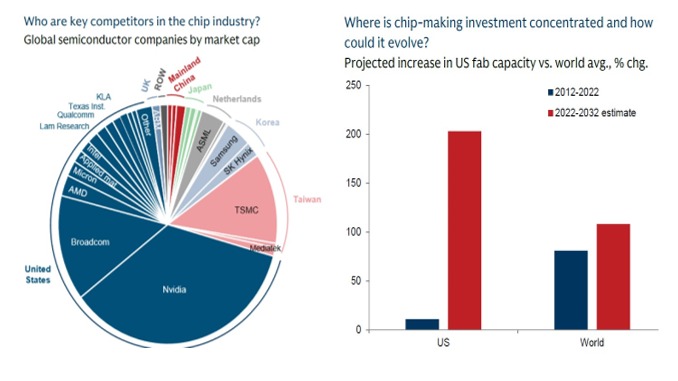

Four main battlefields can be identified in this rivalry. First and foremost, semiconductors and AI. It is always important to remember that there is not a single simple semiconductor supply chain, but rather a network of interconnected chains that extend across the globe (Canuto, 2023). Key bottlenecks include advanced lithography, etching equipment, and cutting-edge manufacturing capacity.

The US and its allies maintain a slight overall advantage, particularly in chip design and manufacturing tools (Figure 1).

Figure 1. Source: Goldman Sachs (2025)

China faces considerable technical challenges in replicating advanced lithography (Garcia-Herrero et al., 2025). It is important to emphasize that leadership in AI will depend not only on access to the most advanced chips, but also on the dissemination and adoption of models. China’s adoption of open-source and low-cost AI models has allowed for rapid real-world implementation, even with less advanced hardware and behind-frontier AI systems.

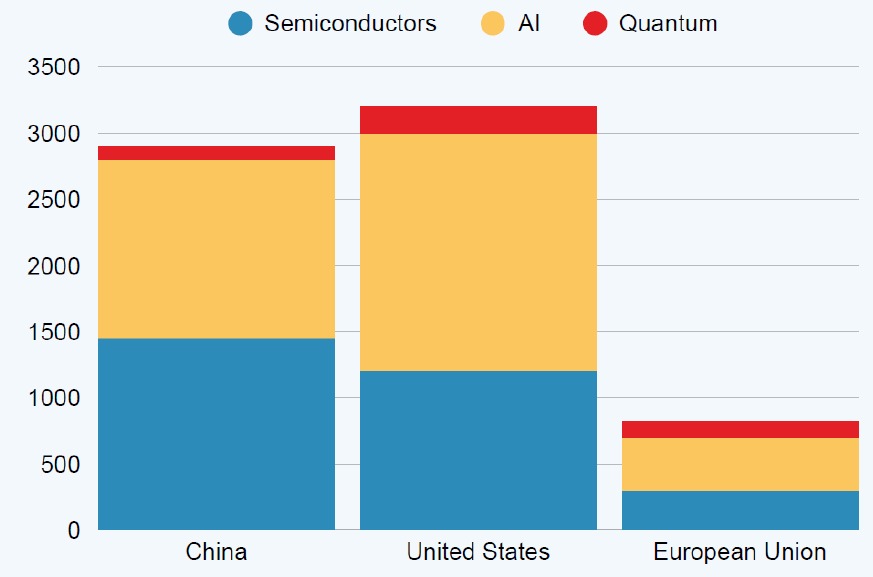

Figure 2 shows how Chinese patent filings in AI, semiconductors, and quantum computing have exhibited high growth, with China emerging as the primary challenger to US technological supremacy. However, while China has acquired significant strengths in specific subfields, it still has to deal with persistent lags in some high-level areas, particularly those targeted by international export controls (Garcia-Herrero et al., 2025). In the case of semiconductors, China’s success has been largely confined to the lower value-added parts of the supply chain, such as assembly and packaging (Canuto, 2023).

Figure 2: Radical Novelties (2019-2023)

Note: Radical novelties defined as breakthrough patents with no prior similar innovations that are subsequently replicated at least five times

Source: Garcia-Herrero et al. (2025)

In the case of AI, the edge by US products has been challenged by China’s low-cost “open” models, which are often free to use, modify, and integrate, something helped by government subsidies. Conversely, US tech groups – OpenAI, Google and Anthropic – have instead preserved full control of their most advanced technology, to profit from it through customer subscriptions or enterprise deals (Criddle, 2026).

Frontlines of the Technological Race (2): Applications

As pointed out by Angela Huyue Zhang (2026):

“While debates over the AI race between the United States and China tend to fixate on which country has the most powerful frontier models and the most advanced semiconductors, that framing is becoming outdated. As AI moves from our screens into the physical world, the question is no longer whose models hit technical benchmarks, but who can build and sustain an ecosystem that embeds AI into everyday products and services.”

As remarked by Tej Parikh (2026):

“The technology race encompasses the embodiment of AI into physical environments through sensing, control and decision-making as generating text and images. This includes intelligent manufacturing, humanoid robots and applications in other devices, such as cars, phones and wearables.”

The ecosystem matters, including complementary technologies (like robotics and electric vehicles) and the embodiment of AI.

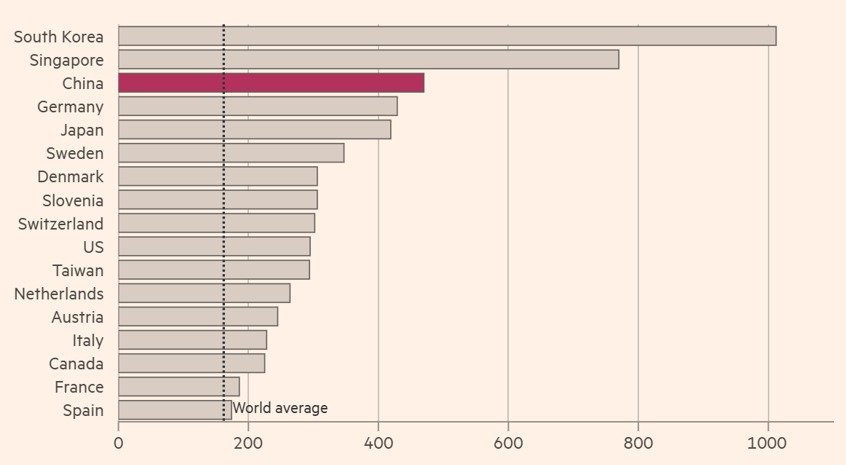

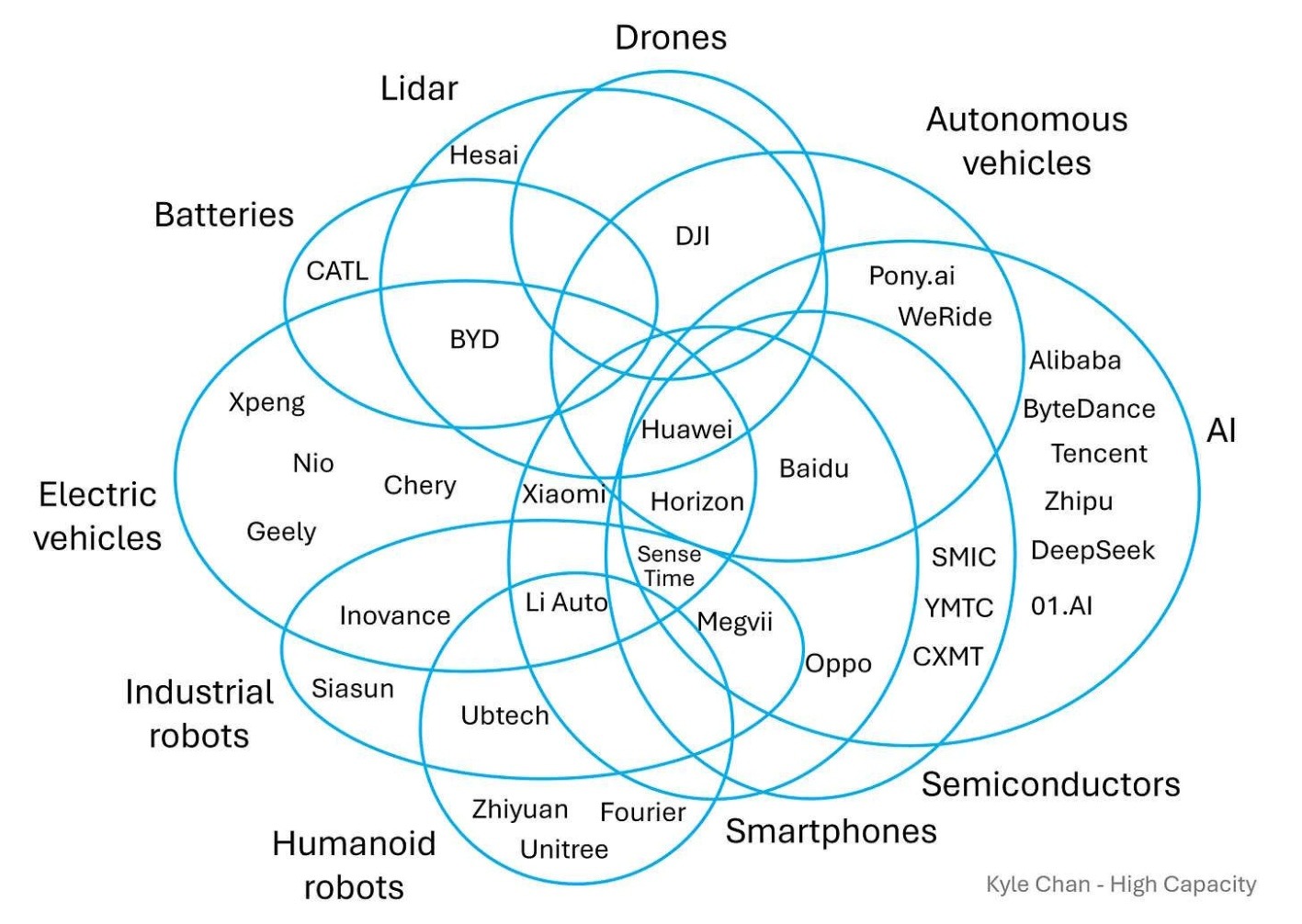

Take, for instance, robotization of industry. China has become a leader at integrating robots in industry (Figure 3).

Figure 3: Robots Installed per 10,000 Employees. Source: Parikh (2026)

By the same token, one may point out batteries, electric vehicles, and self-driving cars – what Noah Smith (2025) called “the electric tech stack”. Electric vehicles, batteries, drones, robotics, smartphones, AI and related constitute overlapping industries with a mutually reinforcing feedback loop – as in the cases of Chinese firms depicted by Kyle Chan (2025) (Figure 4).

Figure 4: China’s overlapping tech-industrial ecosystems. Source: Chen (2025)

Frontlines of the Technological Race (3): Clean Energy

The situation with clean-energy technologies appears contrary to that with semiconductors. In clean-energy technologies, China has built a prevalent position (Canuto, 2023).

The transition to clean energy requires both scientific innovation and large-scale expansion of established technologies. The U.S. remains excellent at the former, including scientific work on carbon capture, storage, and removal. The U.S. is also exploring frontiers in geothermal energy, benefiting from hydraulic fracturing expertise in the shale oil and gas industry. On the other hand, in commercial industries that are in the expansion phase, the U.S. lags China in the most critical decarbonization technologies: solar, wind, batteries, and hydrogen. The higher pace of investment in clean energy by China in the last decade has given it an advantage in learning and technology domains.

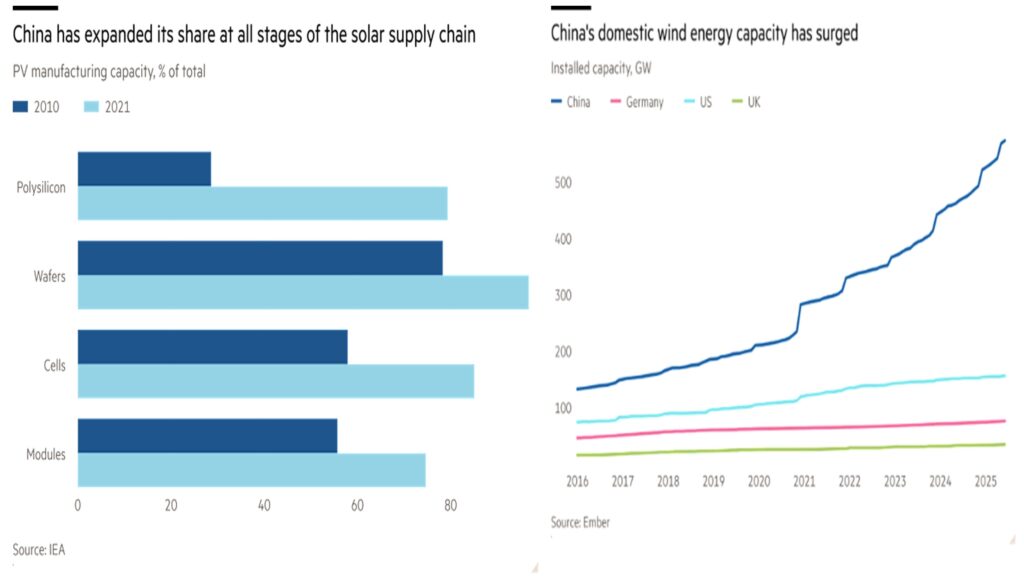

Chinese dominance is evident in solar energy (Figure 5). The 90% decline in the cost of solar energy generation over the last decade came mainly from there, with Chinese companies being responsible for 75% to 95% of each component of the value chain. Tariffs and import bans have not prevented the situation that, today, U.S. imports of photovoltaic cells come mostly from Chinese manufacturers located in Southeast Asia.

Figure 5

The Chinese are also at the forefront when it comes to electric vehicle batteries, gaining ground even from rival firms in Japan and South Korea that were at the technological forefront. Chinese producers benefited from the explosion in the production of electric cars in China, whose local consumption was subsidized by the government. The results in terms of productivity and competitiveness allowed China to acquire a predominant position in car exports (Canuto and Martins, 2024).

The challenge is more complex in the case of wind energy. China today has the majority of the world’s 10 largest producers of wind turbines, but they mainly serve the domestic market (Figure 5, right side). Turbines, with large towers and blades, require assistance and services at installation sites, and Chinese firms face difficulties abroad in this case (Canuto, 2023).

US President Biden approved in Congress and started to implement the “Inflation Reduction Act” (IRA), which was in fact mired at supporting the country’s position in producing clean energy, but President Trump has unwound the policy. And this is happening at a time in which, due to technological learning, costs of producing renewable energy have fallen enough to compete with fossil fuel-based energy.

Frontlines of the Technological Race (3): Critical Minerals and Rare Earth

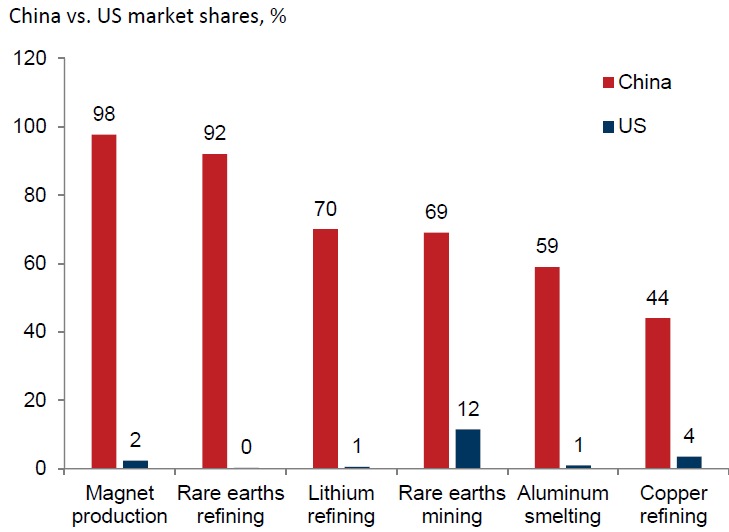

Another focal point is the rare earth and critical mineral supply chains. China dominates the mining, refining, and production of magnets, particularly for heavy rare earths used in defense and advanced technologies (Figure 6).

Figure 6: Critical Minerals Refining and Magnet Production. Source: IES; Goldman Sachs (2025)

This gives China significant leverage, even though total US demand for rare earths is relatively small in absolute terms. But it was the vulnerability of the US to the Chinese supply of rare earths that led the former to a compromise with respect to releasing Chinese access to advanced semiconductors, and the trade truce last year (Canuto, 2025).

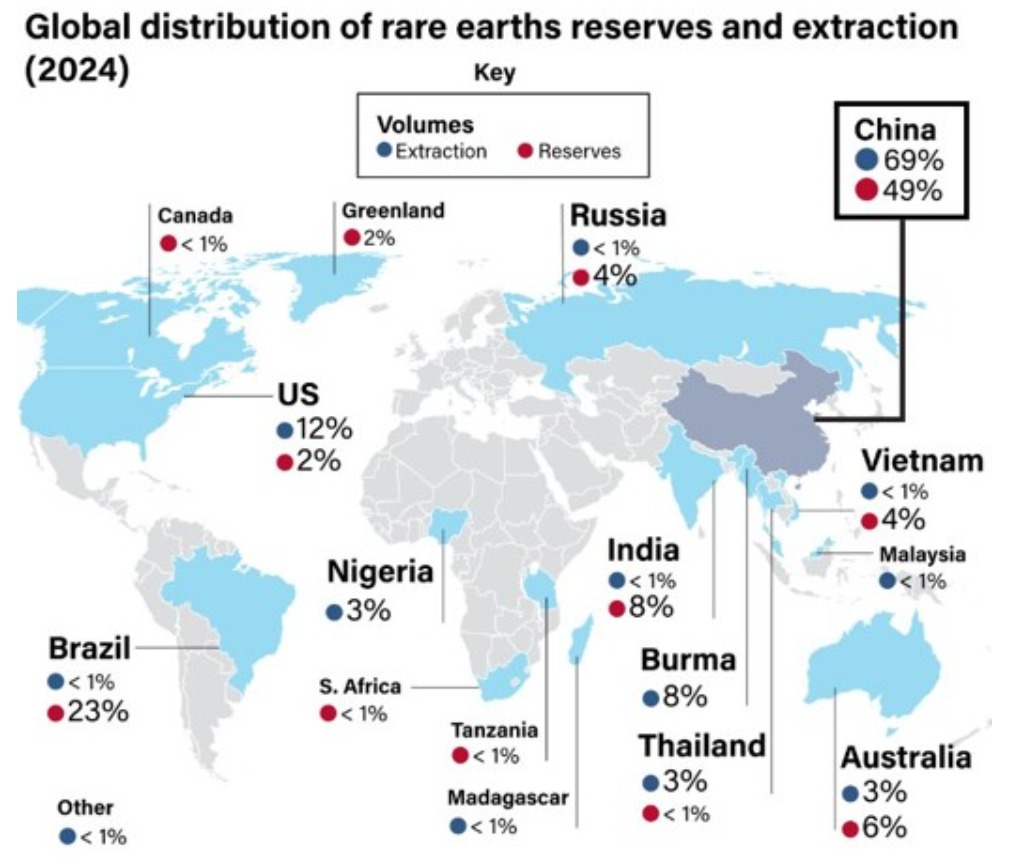

China’s territory is abundant in mineral resources, many of which are central to the production of clean-tech goods, including 72% of the world’s natural graphite and 66% of rare earth elements (Garcia-Herrero et al, 2023).

However, overall, the extraction of clean-tech minerals is spread across the globe, following the locational dispersion of deposits (Figure 7). Chinese companies have been making acquisitions abroad, purchasing a large part of the cobalt and lithium supply. Minerals are distributed across the globe, but most of the refining is in China. Recent threats by China to restrict exports of gallium and germanium represented an escalation in global competition for critical minerals and metals, i.e. yet another field for ‘proxy wars’.

Figure 7. Source: Garman, C. (2026).

In addition to the domestic extraction of key minerals, China has built up abroad a network of mineral supply agreements to supply its domestic refining industry, including cross-border acquisitions and trade agreements. These are primarily in southern and western Africa, Oceania, Latin America, and regional neighbors. Globally, as illustrated in Figure 6 above, China has a special position in terms of processing of rare earth elements, with a market share above 85%, and of silicon and cobalt, all of which are integral to the production of high-energy-density batteries, wind turbines, and solar panels.

An increase in US resilience will require diversification of sources, selective government support, and cooperation with allies. Even so, rare earth elements will continue to be a persistent vulnerability and a recurring source of geopolitical friction, now and in the near future.

Frontlines of the Technological Race (4): Availability of Energy and Infrastructure

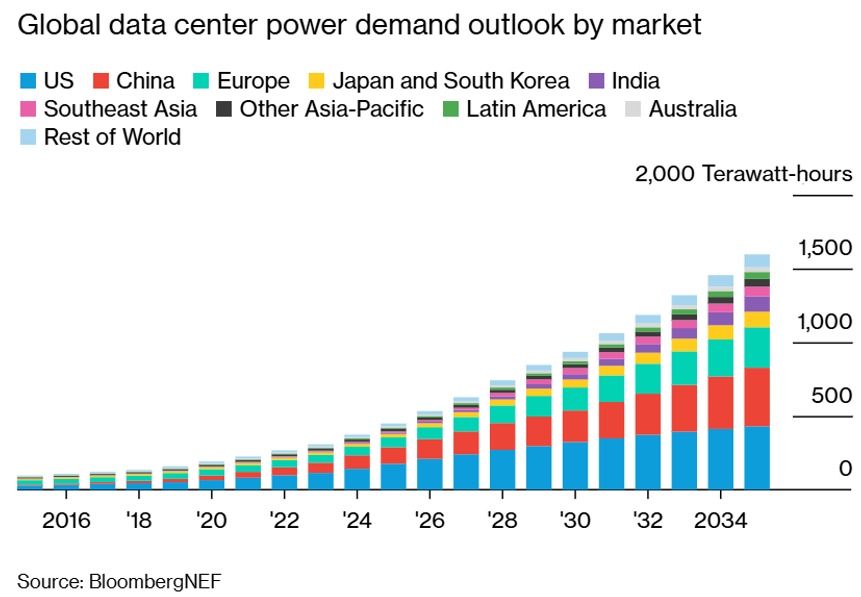

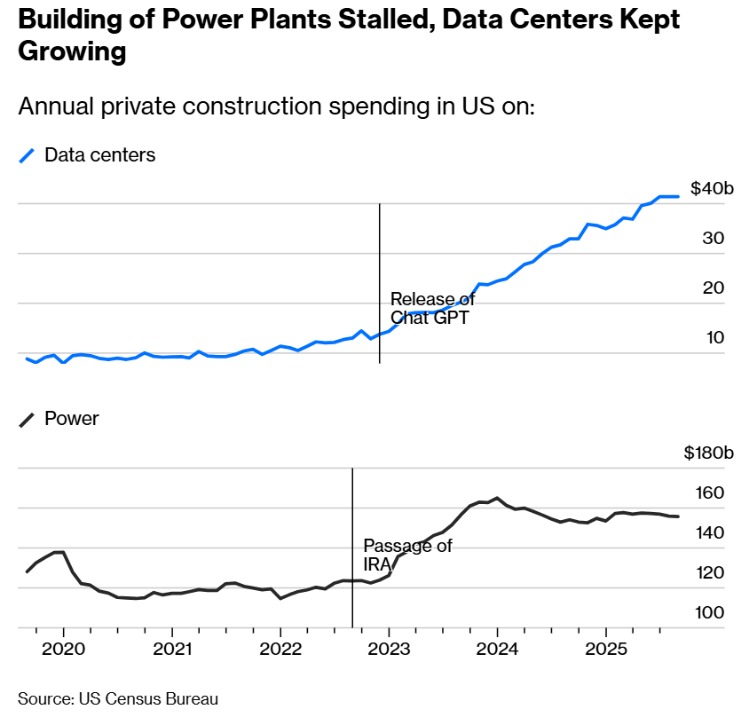

Beyond the three previous battlegrounds, the availability of energy and infrastructure must be highlighted as decisive factors. Advanced AI systems and data centers are extraordinarily energy intensive, and the electricity demand by proliferating data centers will be large. Referring to projections by McKinsey, O’Neill (2026) remarks that: “The new data centers coming online between now and 2030 will need more than 600 terawatt hours of electricity, enough to power nearly 60 million homes.”

The power demand from AI data centers shall quadruple in 10 years (Figure 8). This has not been matched by corresponding building of power plants (Figure 9).

Figure 8

Figure 9

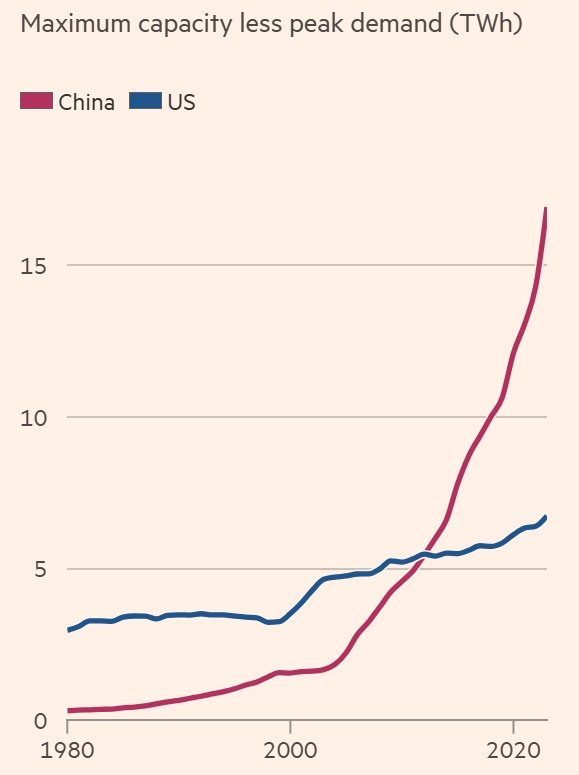

China’s abundant and coordinated investment in power generation—especially in renewable and nuclear energy—gives it an advantage. In contrast, US energy constraints and the fragmentation of the US power grid could become a limitation for AI expansion (Figure 10).

Figure 10: US-China: Electricity Generation Capacity. Source: Parikh (2026).

The “New Normal” of Firm-specific Policies

When it comes to government support via “industrial policies”, US and China differ – even if the former has more intensively applied sector- and firm-specific policies and interventions in recent times.

The US approach may be described as “hybrid and fragmented”, combining elements of wartime mobilization and Cold War competition with market-based incentives (Goldman Sachs, 2025). Policies such as President Biden’s CHIPS Act, advanced manufacturing tax credits, government loans or equity stakes, and trade partner investment pledges are designed to encourage domestic production in strategic sectors. At the same time, the US relies heavily on the private sector to lead innovation, with government policy often focused on de-risking investment rather than directing it.

The Trump administration has rolled back Biden’s IRA, while the world is moving towards a decarbonized economy. Trump has also suspended new leases for offshore wind projects and blocked several projects, while offshore wind has large component parts and needs to be built and maintained near installations. On the other hand, the US government has taken stakes in rare earth companies – keep in mind that rare earths and critical minerals matter beyond the provision of inputs to clean-energy production, and includes military and civil uses in industrial sectors.

China’s approach, by contrast, is “holistic and highly coordinated”. Long-term planning through Five-Year Plans, extensive use of government-guided investment funds, subsidized land and energy, talent development, and directed procurement all work together to accelerate progress in priority sectors. This system allows China to mobilize resources quickly and scale production after breakthroughs, though it also tends to generate overcapacity and inefficient investment.

The South as a Ground for Technological Dispute

The technological rivalry between the US and China spills over into other regions, including energy-rich countries of the “New South.” China is pursuing an initiative to “digitize countries of the South,” offering comprehensive contracts that include infrastructure, services, and data access. This could position it to control networks and data flows across much of the world’s landmass and to adapt AI models to these markets.

The Gulf and the Middle East, an energy-rich region, are considered key energy producers in the AI era. Both Washington and Beijing are competing to secure partnerships in data centers and energy in this region, with the US needing security guarantees to prevent sensitive technologies from being shared with China.

Jorge Arbache (2025) has been discussing “powershoring,” that is, the possibility of countries like Brazil exploring an industrial relocation strategy driven by the availability of green, secure, and cheap energy, aiming to attract investments from energy-intensive sectors, reduce emissions, and strengthen integration into sustainable global supply chains. It is hoped that the potential for energy production will not be captured solely as a chapter in the US-China rivalry in providing data centers for their AIs.

Final Remark

To conclude, let’s highlight the duality of paths. While the US resorts to high investment, top semiconductors and its proprietary ecosystem, China has strived to integrate good-enough models into physical applications, looking for simultaneously disseminating them around the world.

References

Arbache, J. (2025). Powershoring: a Game-Changer for Climate Action and Sustainable Industry, Green Initiative, February 4.

Canuto, O. (1995). “Competition and Endogenous Technological Change: an Evolutionary Model”, Revista Brasileira de Economia, v. 49 n. 1, p. (1995)

Canuto, O. (2019). The US-China Trade War Is Accelerating China’s Rebalancing. Policy Center for the New South, November 8.

Canuto, O. (2021). Climbing a High Ladder: Development in the Global Economy. Policy Center for the New South.

Canuto, O. (2023). A Tale of Two Technology Wars: Semiconductors and Clean Energy, Policy Center for the New South PB – 41/23, November 2.

Canuto, O. and Martins, A.J. (2024). The Automotive Transition on the Road to Decarbonization, Policy Center for the New South PB – 51/24, October 9.

Canuto, O. (2025). The United States and China holstered their weapons, Center for Macroeconomics and Development, November 1.

Chen, K. (2025). China’s Overlapping Tech-Industrial Ecosystems, High Capacity, January 22.

Criddle, C. (2026). Microsoft Warns that China is Winning AI Race Outside the West, Financial Times, January 13.

García-Herrero, A.; Grabbe, H.; and Källenius, A. (2023). De-risking and Decarbonising: a Green Tech Partnership to Reduce Reliance on China, Bruegel, October 26.

García-Herrero, A., M. Krystyanczuk and R. Schindowski. (2025). Radical Movelties in Critical Technologies and Spillovers: How do China, the US and the EU Fare?. Working Paper 07/2025, Bruegel.

Garman, C. (2026). Brazil has Increasingly Valuable Assets in a World of Great Power Conflict, Eurasia Group, January 26.

Goldman Sachs (2025). Top of Mind: The US-China Tech Race, issue 144, December 4.

O’Neill, S. (2026). The AI Bubble Is Getting Closer to Popping, Bloomberg, January 28.

Parikh, T. (2026). China Will Clinch the AI Race, Financial Times, January 18.

Smith, N. (2025). Why every country needs to master the Electric Tech Stack, Noahopinion, September 23.

Zhang, A. H. (2026). Overcapacity is China’s Biggest AI Advantage, Project Syndicate, January 7.

About the Author

Otaviano Canuto, based in Washington, D.C, is a former vice president and executive director at the World Bank, a former executive director at the International Monetary Fund, and a former vice president at the Inter-American Development Bank. He is also a former deputy minister for international affairs at Brazil’s Ministry of Finance and a former professor of economics at the University of São Paulo and the University of Campinas, Brazil. Currently, he is a senior fellow at the Policy Center for the New South, a professorial lecturer of international affairs at the Elliott School of International Affairs – George Washington University, a nonresident senior fellow at Brookings Institution, a professor affiliate at UM6P, and principal at Center for Macroeconomics and Development.

You may have an interest in also reading…

The AI Revolution in the Boardroom: AI Executives are Arriving Sooner Than You Think

The future of business leadership is no longer a distant prospect; it’s unfolding at an unprecedented pace. Artificial intelligence (AI)

La Trobe Financial: The Difference Is Discipline

In an era defined by rapid product proliferation and an ever-expanding universe of investment ideas, one principle continues to separate

Small is Beautiful in Banking: Little US Institutions Form a Financial Backbone

Yerbol Orynbayev, former Deputy Prime Minister of Kazakhstan and World Bank governor, reports for CFI.co on the American banking sector.