Inclusive Markets Are Not Born: How UNCDF is Supporting Inclusive Digital Economies

Inclusive Markets Are Not Born: How UNCDF is Supporting Inclusive Digital Economies by Advancing the Right Policies and Regulations

If you were asked to describe in one word how digital has transformed finance, you wouldn’t be able to do it. Consider a few points.

First, when it comes to the key players in the financial ecosystem, the pond has a lot more fish. In the age of digital finance, capital relies on digital rails provided by mobile network operators. For that matter, in emerging markets across Africa and Asia, telecom companies like Airtel, Vodafone, MTN, and Orange are not only digital service providers. They are effectively financial service providers. And in this new financial ecosystem, the bank is not the central actor for most customers. The mobile network operator is. They serve as the link between banks, financial service providers, super platforms, and the mobile devices that are now the most important tool to access finance. And MNOs are not only facilitating the flow of commerce, but the flow of personal and financial data that can unlock finance from lender to recipients. Then, of course, there are the super platforms where commerce, capital, search, social media and financial inclusion are intersecting at global scale and unprecedented speed: Google, Facebook, and Alipay just to name a few. And if that wasn’t crazy enough, these actors are often in competition with each other.

“For more than 25 years, well before the rise of the digital economy and before anyone was considering a 4th Industrial Revolution, the UNCDF worked with national governments in more than 40 countries to improve the use of financial services.”

If the complexity around access to capital has increased, so has the complexity around the challenges of regulating finance. A central driver of this complexity is the conflict between securing data privacy and validating digital identity. On the privacy side, there are questions relating to service channels, including who and under what conditions can cash agent distribution networks be leveraged; on the payment side, who can be an issuer and under what conditions; and on the store of value, where are funds held and what is the legal treatment? On the digital ID side, how can consumer protection be assured and mechanisms for redress be leveraged when such protection has been violated? Then, of course, there are the critically important efforts of supporting anti-money laundering/combating the finance (AML/CFT) policies and tools.

So, when you aggregate all of these challenges, they all meet at a fundamental question for advancing sustainable development: How can we ensure that financial regulation enables effective flow of finance while also promoting the financial health of the widest swath of people? Answering this question is most critical in the world’s least developed countries (LDCs) where the financial needs are greatest and the flows of formal finance are scarcest.

The answer lies in an irrefutable reality. That innovative and inclusive markets do not just happen. They need policies and regulations to create the environment to function effectively, especially in the financial services sector. Said simply, inclusive policies lead to inclusive markets. So, how can regulators design and enact those regulations and policies?

For more than 25 years, well before the rise of the digital economy and before anyone was considering a 4th Industrial Revolution, the United Nations Capital Development Fund (UNCDF) worked with national governments in more than 40 countries to improve the use of financial services. Since 2010, our focus gravitated towards digital financial services,

If there is one aspect of our experience that remains relevant in this new age of finance, it is that smart policymaking can help technology contribute to inclusive markets. But getting the right policies and regulations in place are probably more important than at any other time. If legal reforms fail to capture the potential of new business models and technologies, then the prospect of ‘being left behind’ is all too real, and the impacts will be all too severe, particularly for the worlds most marginalised communities. This is particularly the case given how the gap in access to digital financial services falls hardest on women and rural communities. Yet, despite the urgency, governments are not always sure where to start with policy or regulatory reforms and how to apply available information and resources.

In response, UNCDF has launched a Policy Accelerator, precisely to provide direct support to policymakers and regulators to bridge the gap between knowledge and implementation. The interdisciplinary team of specialists collaborate with regulators and policymakers to design a practical policymaking process that leverages global research, relevant publications, and peer network engagement. In addition to ongoing support for policymakers and regulators across Africa, Asia and the Pacific, we work closely with partners who share our goals to create enabling regulatory environments.

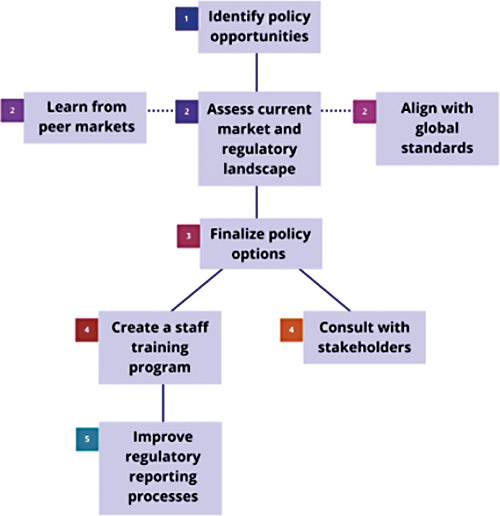

UNCDF’s method entails:

- Identifying the policy opportunities, whether it is economic development, financial inclusion or policy harmonisation

- Assessing the current market and regulatory landscape, while looking to learn from peer markets and align with global standards

- Working with policymakers and regulators to identify the most suitable options available to them

- Creating a framework for dialogue and consultation with stakeholders (like service providers and civil society).

Once the government decides on the best policy/regulatory option for the moment, UNCDF works with them to develop impact metrics and create a training program for the regulators and supervisors.

Leveraging this method in 2020, UNCDF has trained more than 75 regulators and provided focused technical assistance to 15 countries. Eight policies have been introduced or improved, despite the upheaval of a global pandemic. This success is recognised by financial support for the programme from the European Union, the Government of France, and the Bill and Melinda Gates Foundation.

Perhaps our best achievement is the launch and operation of the “Africa Policy Accelerator,” with support from the Bill and Melinda Gates Foundation. The “Africa Policy Accelerator” is UNCDF’s bespoke platform to provide targeted technical assistance and capacity building for policymakers and regulators in14 African markets with potential to ‘leapfrog’ to digital finance and benefit women’s financial inclusion and regional harmonisation. UNCDF is augmenting its work on the ground by contributing knowledge and policy guidance through the G7 Partnership for Women’s Digital Financial Inclusion in Africa as part of France’s 2019 G7 Presidency. With our participation in this high-level forum, we are looking to support policymakers and regulators to conduct country-level research on barriers to women’s economic empowerment to address critical policy and regulatory gaps, focusing heavily on francophone markets in West and Central Africa.

Looking ahead, UNCDF will leverage its approach, experience and expertise in financial inclusion towards the creation of the UNCDF Policy Toolkit. The Policy Toolkit will be a freely available collection of practical resources – including downloadable templates, worksheets, and sample materials — that will enable regulators and policymakers to nimbly respond to the complex changes in markets and with inclusive policies and regulations.

Rather than proposing a new model for policymaking and regulatory development, we designed our Policy Toolkit in a sequence that parallels a logical approach to policy and regulatory design, while being adaptable so that users can apply it to ocal contexts. The resources within the Policy Toolkit focus on a stage, topic, or task related to the policymaking process, such as:

- Identifying policy opportunities for DFS,

- Assessing the current market, and

- Improving regulatory reporting processes.

For example, instead of brainstorming your own list of stakeholder interview questions, we’ve drafted 50+ questions organised by theme and sector that you can use as a jumping off point. Or if you are looking for opportunities to improve regional harmonisation of digital financial services, we outline a sample process with supporting materials to help you work through it systematically.

We anticipate the Policy Toolkit will be fully live, and available to policymakers and regulators, by Q2 2021.

Digital finance will not become simpler with time. More actors will enter the pond and new technologies will alter the landscape. And one of, if not the most critical factor, in preventing this complexity from becoming a barrier to inclusive growth is delivering the right policies and regulations. UNCDF is ready to do its part to help policymakers and regulators deliver those policies and regulations. Innovative and inclusive markets are not born. They are made. We will work to keep making them now and into the future.

About UNCDF

The UN Capital Development Fund makes public and private finance work for the world’s 46 least developed countries (LDCs).

UNCDF offers “last mile” finance models that unlock public and private resources, especially at the domestic level, to reduce poverty and support local economic development.

UNCDF’s financing models work through three channels: (1) inclusive digital economies, which connects individuals, households, and small businesses with financial eco-systems that catalyse participation in the local economy, and provide tools to climb out of poverty and manage financial lives; (2) local development finance, which capacitates localities through fiscal decentralisation, innovative municipal finance, and structured project finance to drive local economic expansion and sustainable development; and (3) investment finance, which provides catalytic financial structuring, de-risking, and capital deployment to drive SDG impact and domestic resource mobilisation.

By Ahmed Dermish Lead Specialist, Policy and Regulation for Inclusive Digital Ecosystems, UN Capital Development Fund

You may have an interest in also reading…

Accenture on Generative AI: Surfing the Next Wave of Digital Transformation

Artificial intelligence is here to stay, and, with suitable caution that should be a good thing, argues Bashar Kilani. Generative

Africa Leapfrogging Challenges with its Mobile Solutions Boom

From fintech payment systems to drone-delivery of medical services, the continent is on a roll. Africa is embracing innovation continent-wide

Mitigating AI Gender Bias Risks in the Workplace

AI is transforming the workplace, providing unparalleled opportunities for efficiency. However, like any powerful tool, AI also presents its own