Business in Times of Corona: Steering Economies by Dead Reckoning

Ridiculed and even vilified last week for refusing to drive interest rates deeper into negative territory, President Christine Lagarde of the European Central Bank proved ahead of the curve as she urged – up to four times in about thirty minutes – Eurozone governments to meet the impending recession with vast outlays of cash.

Ridiculed and even vilified last week for refusing to drive interest rates deeper into negative territory, President Christine Lagarde of the European Central Bank proved ahead of the curve as she urged – up to four times in about thirty minutes – Eurozone governments to meet the impending recession with vast outlays of cash.

As the US Federal Reserve’s move to slash interest rates by 50 basis points showed over the weekend, central banks have no meaningful monetary instruments left to provide the support needed. Predictably, markets were unimpressed by the rate cut and continued their slide on Monday. Only decisive action on the fiscal side can offer a measure of succour to frightened and highly volatile markets driven by thoroughly spooked investors.

Ms Lagarde’s appeal seems to have resonated in The Hague and Berlin where an unprecedented spending splurge is in the making. On Monday, the Dutch government hinted at the strength of its resolve by reportedly preparing a €90 billion emergency package to help businesses and workers survive the crisis. Finance minister Wopke Hoekstra, until just a few days ago the stingiest member of Prime Minister Mark Rutte’s cabinet, left no room for doubt as he displayed a surprising eagerness to deploy his country’s formidable hoard of cash. Mr Hoekstra explained that now is the time to tap into the reserves accumulated during a decade of thrift.

Next door, Germany mulls an equally forceful intervention to keep its economy afloat, and possibly, humming. Finance minister Olaf Scholz promised to ready a ‘big bazooka’ to avert the impending crisis. As a first step, state-owned development bank KfW received an additional €93 billion in government-backed guarantees, raising its financial firepower to just under €550 billion.

Economy minister Peter Altmaier had his own whatever-it-takes moment and said that the administration is making an ‘unlimited pledge’ of support to businesses of all sizes. The intervention by Messrs Scholz and Altmaier signals an abrupt end to Germany’s ‘black zero rule’ – the dogmatic policy that outlaws fiscal deficits. In a perhaps even more stunning sign that times have changed, Chancellor Angela Merkel suggested over the weekend that she might look away if severely hit countries such as Italy and Spain flout EU fiscal rules. Valdis Dombrovskis, executive vice-president of the European Commission, on Monday obligingly confirmed that the rule book has been binned. From now on, Eurozone economies are to be steered by dead reckoning.

For its part, the European Commission announced plans to redirect up to €37 billion in EU funds to initiatives that support businesses whilst finance ministers consider resuscitating the €410 billion European Stability Mechanism (ESM) set up in the wake of the 2008-09 banking crisis. After a six-hour video conference of finance ministers on Monday, Eurogroup president Mario Centeno said that the members will do – you guessed it – ‘whatever it takes’ to restore confidence and support a speedy recovery. However, ESM access is tied to strict fiscal conditions which need considerable relaxing before the fund can be of any use.

The expectation – really more of a hope – is that northern largesse may trickle southwards and help support the weaker European economies. Together, the liquidity support measures thus far unveiled, equal about 10 percent of EU GDP. That volume of funding, committed in under a week, surely dispels any lingering doubt that European governments are stuck in their more usual ‘too little, too late’ mode.

In an almost complete reversal of attitudes to markets and businesses, the Dutch government declared it will simply not allow flag carrier KLM to founder under any circumstances whilst Paris was noticeably hesitant to offer a similarly iron-clad guarantee to Air France. Though both companies merged in 2004, they have retained their respective hubs and maintain a significant degree of operational and financial autonomy – a frequent source of friction.

Now that governments have stepped up, corporations should try to resist their natural urge to batten down in the face of the corona storm. It is only a matter of days before bargain hunters step in to put a floor under the market. In Europe, preliminary guesstimates are that the economic impact of the corona crisis may cause a manageable 1 percent contraction of GDP, as opposed to the 1.4 percent growth forecasted before the virus hit.

Meanwhile, more nimble small businesses are beginning to improvise ways to maintain a semblance of cash flow. Sensing an opportunity as patrons are confined to their homes, a growing number of restaurants manage to keep their kitchen open by offering delivery services. Distributors of movies have started to offer early releases of their blockbusters on streaming platforms. Online services and logistics are the two sectors most likely to fare reasonably well as economies adapt to new and shifting realities. Out of the box thinking has become a crucial survival strategy. Corporate orthodoxy offers few, if any, answers to the burning questions that surface as economies navigate uncharted waters.

In an example perhaps worth emulating, business leaders in India are working on a Corona Vow that includes a promise not to profiteer and a pledge to invest in workforce skill development. The vow also tables a few useful suggestions such as ‘content disruption’, an opportunity for both advertisers and platforms to serve the needs of the vast number of people who suffer imposed idleness.

According to Shivaji Dasgupta of brand advisory firm Inexgro, content providers stand to do well from the crisis as long as they move smartly and quickly to engage a newly captive audience. In particular, Mr Dasgupta calls on newspaper, magazine, and book publishers to seize the moment and reclaim part of the market share lost to the print industry’s disruptors.

The new times bring not just fear and uncertainty but also opportunity. For businesses it remains, however, of paramount importance to keep calm and carry on whilst being alert to shifting consumer demand and changing consumption patterns. Help is on the way.

You may have an interest in also reading…

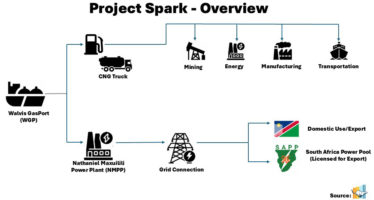

Project Spark: Powering Southern Africa’s Future Through a Balanced Energy Mix

Namibia’s first gas-to-power plant aims to address the region’s chronic energy shortages through a pragmatic, balanced approach that blends innovation,

The Hidden Titan: Why the American Rail Network is the Unsung Engine of Global Commerce

While attention often centres on congested highways and crowded airspace, a quieter system underpins the movement of goods across the

PwC: ‘When it Comes to Securing the Future, There’s No Time Like the Present’

ESG and sustainability priorities are increasingly important business considerations; PwC Luxembourg is on the case… Goodbye theory, hello action —