IMF on MENAP: Call for Focus on Job Creation

The near-term economic outlook for the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) region has weakened. Difficult political transitions and increased regional uncertainties arising from the complex civil war in Syria and the ongoing developments in Egypt weigh on confidence in the oil-importing countries.

The near-term economic outlook for the Middle East, North Africa, Afghanistan, and Pakistan (MENAP) region has weakened. Difficult political transitions and increased regional uncertainties arising from the complex civil war in Syria and the ongoing developments in Egypt weigh on confidence in the oil-importing countries.

Meanwhile, domestic supply disruptions and weak global demand are reducing oil production, notwithstanding recent upward pressure on oil prices arising from increased geopolitical risks. Growth in the MENAP region is expected to decline to 2¼ percent this year (¾ percentage point below our May 2013 projections). Growth is expected to pick up in 2014 as global conditions improve and oil production recovers. Substantial downside risks weigh on this outlook, and, more worrisome, growth will remain well below levels necessary to reduce the region’s high unemployment and improve living standards. In this setting, the region risks being trapped in a vicious cycle of economic stagnation and persistent sociopolitical strife, underlining the urgent need for policy action that will enhance confidence, growth, and jobs.

Oil Exporters: Heightened Risks to Oil and Fiscal Positions

Domestic oil supply disruptions and lower global demand are set to markedly reduce growth in MENAP oil exporters to about 2 percent this year after several years of strong performance. Renewed oil output disruptions in Iraq and Libya, falling oil exports in Iran in response to tightening sanctions, and a modest fall in oil production in Saudi Arabia reflecting a still amply supplied global oil market imply a fall in regional oil production this year, for the first time since the global crisis. By contrast, the non-oil economy continues to expand at a solid pace in most countries, supported by high levels of public spending and a gradual recovery of private sector credit growth. A recovery in oil production and a further strengthening of the non-oil economy will likely lift economic growth in 2014.

“A large aggregate fiscal surplus of about 4¼ percent of GDP masks underlying vulnerabilities.”

A large aggregate fiscal surplus of about 4¼ percent of GDP masks underlying vulnerabilities. Half of the MENAP oil-exporting countries cannot balance their budgets and have limited buffers against shocks. Most countries are not saving enough to allow for continued spending for future generations once hydrocarbon reserves are exhausted. Some countries have started to unwind fiscal stimulus this year; still, without further adjustment, the region’s governments will start spending from their savings by 2016. External balances are also falling because of lower oil production, rising domestic consumption, and insufficient fiscal savings.

Risks to this outlook are broadly balanced for the countries of the Gulf Cooperation Council (GCC) and tilted to the downside for the non-GCC countries. On the upside, increased geopolitical uncertainties may push oil prices higher. Further supply disruptions caused by weak domestic security or a difficult external environment could reduce oil production in some countries, especially outside the GCC, while benefitting growth in oil suppliers with spare capacity (mostly in the GCC) as they compensate for the shortfall. On the downside, slowing global oil demand, for instance caused by lower growth in emerging markets or rising supply from unconventional sources could reduce oil prices and/or induce members of the Organization of the Petroleum Exporting Countries (OPEC), particularly in the GCC, to cut back supply.

Apart from oil, a main downside risk for all oil exporters in the region is the possibility of slower nonoil private sector growth and higher unemployment and inequality if governments’ efforts aimed at diversification do not bear fruit.

In this environment, policies should focus on strengthening fiscal positions and engaging in structural reforms to bolster private sector growth, diversification, and job creation. Oil exporters need to consolidate their budgets to ensure fiscal sustainability while minimizing the impact on growth and enhancing equity. Structural reforms should include strengthening the business climate and competitiveness, especially in the non-GCC countries; measures to support diversification; fostering credit to small and medium-sized enterprises; and improving incentives for private sector employment of nationals and female labor force participation.

Oil Importers: Complex Political Dynamics and Security Challenges

The economic recovery in the MENAP oil-importing countries has once again been delayed. Heightened security concerns, rising political uncertainty, and delays in reforms continue to weigh on confidence, preventing a recovery in investment and economic activity in many countries. The devastating civil war in Syria and recent developments in Egypt have sparked concerns about regional spillovers, further complicating economic management. While there are nascent signs of improvement in tourism, exports, and foreign direct investment in some countries, the economic recovery in the MENAP oil importers remains sluggish, with growth of about 3 percent, in 2013–14, significantly below the growth rates necessary to reduce persistent unemployment and improve living standards.

Domestic and regional factors are the main sources of downside risks. Insufficient improvement in economic conditions risks aggravating sociopolitical frictions and dealing additional setbacks to transitions in many countries, thereby reinforcing delays in the economic recovery, potentially leading into a vicious cycle. In addition, a deterioration of conditions in Egypt would further damage confidence and recovery prospects. Increased escalation of the conflict in Syria would intensify pressures on neighboring countries (Iraq, Jordan, Lebanon) as refugee inflows would rise sharply. Under a plausible adverse scenario, assuming domestic and regional risks partially materialize, growth could fall to 1¾ percent next year, though a stronger shock or a combination of domestic and external shocks could halt growth to zero and significantly raise unemployment. In addition, geopolitical tensions might lead to a spike in oil prices, which, if sustained, would reduce growth and widen fiscal and external deficits (though for some countries in the Mashreq, the effects would be mitigated because of strong linkages to the GCC). A weakening in the external environment, for example, lower-than-anticipated growth in the BRICS (Brazil, Russia, India, China, South Africa) and/or the GCC countries, or a protracted period of slower European growth, would weigh on tourism, trade, remittances, and capital flows.

Small external and fiscal buffers make MENAP oil importers highly vulnerable to shocks. Foreign exchange reserves are running low, and current account deficits remain substantial in many countries. High or rising public debt levels are of concern, driven by persistently large fiscal deficits, which in turn reflect strong pressures for subsidies and other social spending amid high unemployment. Even as countries are realizing the need for fiscal consolidation, fiscal deficits are still rising in most countries, and medium-term plans for fiscal consolidation remain unclear.

In this environment, characterized by significantly increased risks due to heightened political uncertainty and rising regional tensions, policy goals are threefold: (1) fostering economic activity and creating jobs to help sustain sociopolitical transitions, (2) making inroads into fiscal consolidation to restore debt sustainability and rebuild buffers protecting the economy from unanticipated shocks, and (3) embarking without delay on structural reforms that will improve the business climate and governance, and enhance equity:

Creating jobs. High and rising unemployment amid a strained social fabric and heightened political uncertainty in many countries calls for an urgent focus on spurring economic growth and job creation. Delays in the revival of private investment suggest the need for government to play a key role in shoring up economic activity over the near term. With limited room for widening fiscal deficits in many countries, consumption spending on broad-based subsidies needs to be re-oriented toward growth-enhancing public investment, while improving protection of vulnerable groups through well-targeted social assistance. External partners could support this priority by providing additional financing for public investment spending and basic services based on the existence of adequate policy frameworks.

Fiscal consolidation. With concerns about debt sustainability rising and fiscal and external buffers eroding, most countries need to start putting their fiscal house in order. This said, in some cases, there may be scope for phasing the fiscal adjustment over time to limit its impact on economic activity in the short run. The feasibility of such phasing will depend on a credible medium-term fiscal consolidation strategy to ensure continued willingness of domestic and foreign investors to provide adequate financing. Consideration needs to be given to supporting fiscal consolidation through greater exchange rate flexibility, which can help to soften the shortterm impact of fiscal consolidation on growth and help to rebuild international reserves.

Structural reforms. A bold structural reform agenda is essential for propelling private sector activity and fostering a more dynamic, competitive, and inclusive economy. Reforms need to be focused on a multitude of areas, including improving business regulation and governance, expanding access of businesses and consumers to finance, enacting labor market policies that support job creation and employment opportunities, and protecting the vulnerable through welltargeted social assistance. Early steps in these areas can help to signal governments’ commitment to reforms and can help improve confidence.

The region’s need for improving economic conditions and living standards is tremendous, as is its human and economic potential. Delays in economic recovery and rising unemployment underscore the urgency of policy reforms. Early progress across all three priority areas—supported by the international community through scaled-up financing, enhanced trade access, and technical assistance—is essential to begin achieving the much-awaited dividends from the recent economic and political transitions.

You may have an interest in also reading…

Blackstone’s Data Centre Push: When Private Capital Opens The AI Rails To Public Investors

As the AI boom shifts from model-building to infrastructure-building, data centres have become the new industrial real estate. Blackstone’s reported

How Will Artificial Intelligence Affect the Economy?

Artificial intelligence (AI) is the name given to the broad spectrum of technologies by which machines can perceive, interpret, learn,

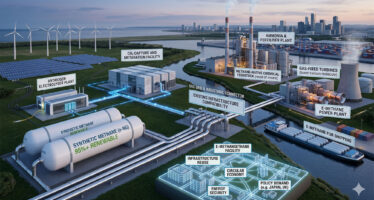

Synthetic Methane’s Opening Window for Investors and Policy Makers

Synthetic methane is moving from technical curiosity to investable relevance because it offers something rare in the transition: a lower-carbon