Principles for Responsible Investment: Investors Must Commit to Engaging Policymakers

The recent mobilisation by institutional investors over the climate change issue has captured media attention around the globe, clearly demonstrating the power investors have when it comes to engaging policymakers.

The recent mobilisation by institutional investors over the climate change issue has captured media attention around the globe, clearly demonstrating the power investors have when it comes to engaging policymakers.

While investor engagement with policymakers is not new, what has changed over the past decade is the emergence of responsible investors seeking policy change that promote sustainable value creation.

This goal dovetails with the needs and interests of policymakers who are interested in long-term economic growth, competitiveness, job creation, environmental protection, and social stability.

In a report published earlier this month, the United Nations-supported Principles for Responsible Investment (PRI) examined the case for long-term investors to engage public policymakers. For some the case is already clear, but for most, it’s not.

“The importance of public policy for long-term investors has grown in recent years as governments look to institutional investors as a source of long-term financing.”

The report surveyed PRI’s 1,300 signatories and found that 92% support further work to address obstacles to sustainable financial markets that lie within “market cultures, structures, and regulations.” A further 76% ask the PRI to influence public policy with respect to responsible investment.

However, of 814 investors completing the PRI’s annual reporting framework, only 332 state that they have in fact engaged with policy makers. We needed to know the reasons behind this shortfall.

Stumbling Blocks to More Widespread Engagement

The report found various reasons why organisations are failing to actively engage with policy makers. Some express scepticism about whether public policy engagement will make a difference. Others are concerned about the costs and timeframes involved, and that competitors will free-ride on their work. Most say that their organisation lacks understanding on how to influence policy processes or they fear that policy engagement is the same as political lobbying.

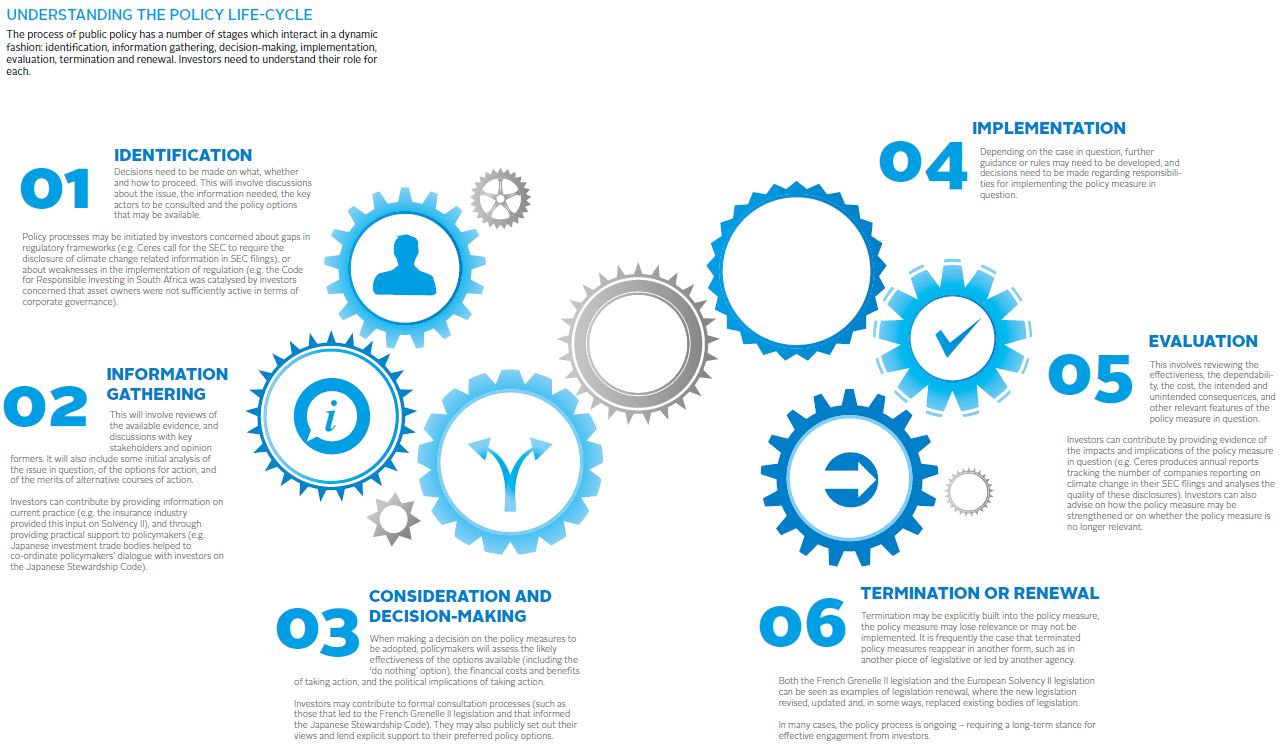

Click to enlarge

Equally, policy makers can distrust investors. “Investors say they speak on behalf of their beneficiaries, but that is not always the case,” one policy maker told us. Another reminded us that “investors are often not the most important stakeholder.” These sentiments explain why investors are often consulted late in the policymaking process, if at all. And, while some of these concerns might be legitimate, there can also be a lack of understanding by the policymaker of the varying needs and interests of market participants.

The importance of public policy for long-term investors has grown in recent years as governments look to institutional investors as a source of long-term financing. Similarly, investors have become increasingly aware of the impact of environmental, social, and economic factors on their ability to deliver long-term returns, engaging policy makers to tackle questions of market failure, such as climate change, misaligned incentives, and information asymmetry. This means that both sides must find a way to put aside their differences so that meaningful discussions about ESG (environmental, social, and governance) issues can be effected.

“The aim of policy engagement is not to replace the market, but correct it,” says Nick Robins, co-director of a United Nations Environment Programme inquiry into sustainable financial markets. “Well-developed policy can end innovation bottlenecks in order to promote research and development, develop market standards and generate higher returns. Active, engaged owners will also lead to greater accountability and governance between shareholders and corporations.”

Breaking Down the Barriers

To facilitate engagement, the PRI seeks to explain the range of policy options; regulation can be mandatory, stewardship is not, some regulation is national, some cross-border, some applies to capital markets, some specific to pension funds, and so on.

The PRI breaks this down into three categories. First, “wider economic policy,” for example, Japan’s Abenomics, or Germany’s energy policy. Second, “financial sector regulation and policy,” like the US’ Dodd-Frank or Europe’s Solvency II. And finally, “ESG regulation and policy,” like the Code for Responsible Investing in South Africa (CRISA) or France’s Grenelle Laws articles 224 and 225.

Within ESG regulation and policy there are various tools available to policymakers. At its simplest, a policymaker can enforce mandatory exclusions, like cluster munitions. Policymakers can also force investors, or the companies in which they hold positions, to report on how they manage environmental, social, and governance risks.

Case Study: Solvency II

Strengthening financial sector regulation has been a priority in the wake of the global financial crisis. However, in addressing one set of policy problems, it is not uncommon to create others. The Solvency II Directive, which sought to strengthen risk management in the insurance sector, may actually increase the sector’s focus on short-term financial performance and reduce its ability to invest in areas such as unlisted assets, infrastructure and private equity.

In the late 1990s, there was wide recognition that the insurance sector was lagging behind banking in terms of risk-based regulation. There was pressure to establish a new regulatory framework for the European insurance industry.

The need to modernise the regulatory framework received further impetus in the early 2000s following the market collapse post-Enron. The agenda was strongly supported by insurance companies, who wanted to be able to better manage their risks, and by regulators who wanted all risks (e.g. balance sheet, credit, market, operational) to be assessed and reported so they could get a better picture of the risk profile of the industry.

Solvency II was intended to consolidate relevant legislation and bring the legislation up to date with modern insurance practices. The framework has three main pillars:

- Pillar 1 sets out the minimum capital and solvency capital requirements for insurers, i.e. the ability to withstand a 1-in-200 year financial event lasting for one year.

- Pillar 2 sets out requirements for the governance and risk management of insurers, as well as for the effective supervision of insurers.

- Pillar 3 focuses on disclosure and transparency requirements.

Following preparatory work and extensive consultation with regulators and stakeholders, a legislative proposal was presented to the European Parliament in 2007, and the final version of the Solvency II Directive was adopted in November 2009.

Insurance companies played an active role in the discussions surrounding Solvency II. Much of this was led by trade bodies, such as Insurance Europe, the Pan-European Insurance Forum and the Chief Risk Officers Forum.

These trade bodies invested significant time in identifying priority issues and in developing a common agenda concerning these issues for the industry as a whole. This included whether solvency capital would be calculated using a formula developed by regulators or whether the industry could use its internal models, and the specific amount of capital that needed to be held against liabilities.

Following the financial crisis, the industry recognised the implications of market volatility and pressed for changes to reflect the nature of the risks and the characteristics of the liabilities. In particular, ways of reconciling the fact that assets were to be valued on a mark-to-market basis while liabilities were valued on a risk-free basis were considered.

This meant that insurance companies were exposed to market movements on assets but not on liabilities, which created problems in volatile economic conditions, and ignored the fact that insurance investors may not have needed to sell at these points in the economic cycle, thus reducing the incentive to invest in long-term infrastructure.

The insurance industry therefore engaged intensively with the European Commission to introduce appropriate corrective mechanisms for this problem. In 2013, a compromise was agreed that addressed investor concerns by allowing them to use mark to market valuations for both their liabilities and their assets. Following an EU Parliament vote in March 2014, the Solvency II Directive was scheduled to come into effect on 1 January 2016.

Solvency II is a case study of how financial services can work effectively with policymakers to deliver the desired policy goals, in this case strengthening the industry’s risk management processes in an economically effective manner.

However, it also highlights the risks of unintended consequences; in this case, the unintended consequence is that Solvency II may reduce insurance companies’ willingness to invest in long-term infrastructure. This is because the standard risk-based approach in Solvency II results in longer term investments carrying higher capital charges.

To promote active ownership, a number of governments have introduced stewardship codes, including Japan’s, to encourage foreign investment in companies. Stewardship codes are voluntary, but generally speaking, market forces encourage compliance. Finally, policymakers can require ESG integration, as we see with Grenelle’s article 225, requiring companies, including financial entities, to report on their commitment to sustainable development, and on the environmental, social, and societal impact of business activities.

Policy engagement is not easy. It requires time, patience, and resources. It also requires stamina. Policy engagement can be across multiple departments, or even countries. Perhaps, in the case of tackling climate change, it never ends. Policy and politics can, at times, also seem analogous. Investors need to be objective, engaging on facts.

To scale up public policy engagement, investors can use the “5C” checklist; commit, construct, clarify, collaborate, and communicate.

By committing to public policy engagement, a long-term investor will adopt a formal position statement, allocating necessary resources. Investors can assemble a structured process that promotes engagement in policy, clarifying the key policy issues that are of concern to the organisation.

Investors should collaborate to pool resources and achieve greater impact, and ensure that traditional investor bodies incorporate responsible investment in their policy engagement. Finally, investors must communicate, reporting annually on policy engagement to savers and beneficiaries.

Likewise, policymakers must actively seek the input of long-term investors, ensuring key individuals and organisations are properly represented on relevant working groups and advisory panels. Policymakers would do well to better understand the needs and interests of long-term investors and their end beneficiaries, recognising how these differ from other institutional investors, banks, and companies.

Future Outlook

Heading into 2015, there will be no shortage of critical policy decisions where responsible investors will need to collaborate and commit. At the international level, three stand out. The first is the G20 discussions on long-term financing to close the infrastructure funding gap, and the need to ensure that these policies fully incorporate environmental, social, and governance factors.

The second is the launch of the new set of Sustainable Development Goals, where there is a sharper focus on how to mobilise private capital alongside essential public finance.

The third is the climate change negotiation, culminating in the Paris Conference in December 2015 where the initial compilation of pledges made in New York will need to come to fruition.

These three priorities are of course deeply intertwined. And one of the real contributions that investors can make is to show why a joined-up policy framework is so badly needed to avoid unintended consequences of regulatory change and deliver a truly efficient allocation of capital for the long-term interests of the world’s savers.

Investors have great power at their disposal and can effect change. The good news is that policymakers appear to have their office doors open. Jean-Claude Juncker, president of the European Commission, said in an October 2014 speech: “We are facing an investment gap. We have to work to bridge that gap”. The time is now.

About the Author

Author: Helene Winch

Mrs Helene Winch is director of public policy and research at Principles for Responsible Investment (PRI) – an investor initiative in partnership with UNEP Finance Initiative and UN Global Compact.

You may have an interest in also reading…

Blended Finance’s Second Act: The OECD Renews Guidance to Effectively Align Development Goals and Investment Returns

A decade after blended finance entered the global lexicon, the challenges it was meant to address have multiplied – and

Paris-based Powerhouse Île-de-France: Leading the Way for Local Authorities

The region’s president, Valérie Pécresse, is gunning for nothing less than 100 percent when it comes to sustainable debt. Île-de-France

Kathrein Privatbank: Innovating Private Banking with Digitalisation, Sustainable Investing, and Regional Expansion

For over a century, Kathrein Privatbank has remained a benchmark for private banking excellence in Austria. By blending traditional values