No Sugar Coating for Kenya’s Cane Industry, but KISCOL has an Established Place in Industry

Increased competition and dwindling natural materials challenge some producers, but KISCOL is growing, diversifying, and ‘doing things right’…

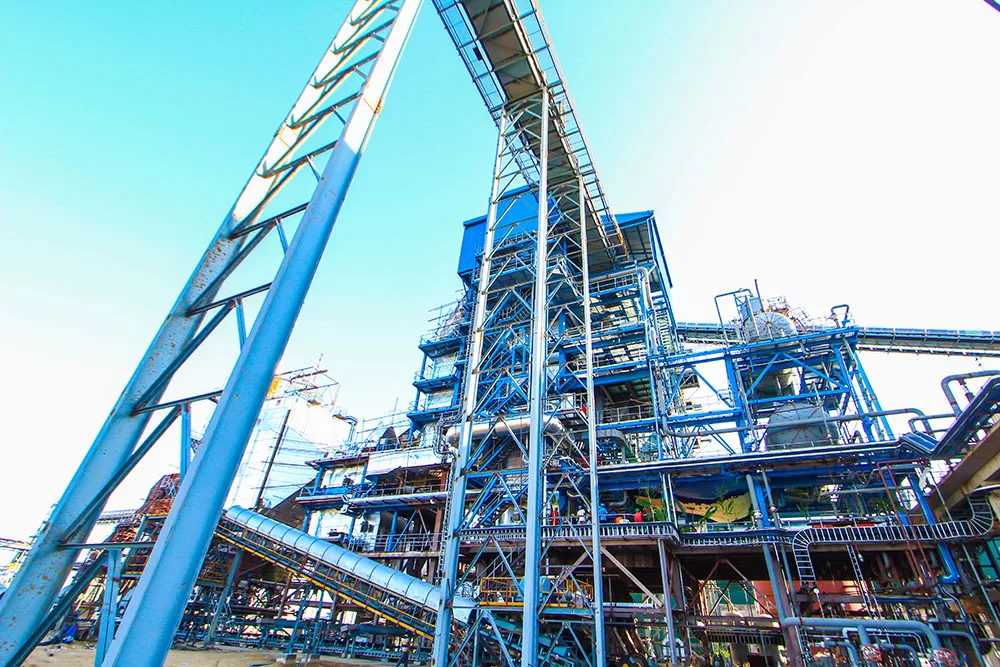

Kwale International Sugar Company Ltd (KISCOL) knows full well the sweet taste of success.

The Kenyan firm boasts a $300m processing facility, 5,500 hectares of cultivated sugarcane, a mill capable of crushing 3,300 tonnes per day, an 18MW bagasse-fired power plant, and a sophisticated irrigation and water-management system.

CFI wanted to find out more about the organisation which prides itself on producing affordable, locally grown sugar. We put some questions to the KISCOL team behind the flagship project of the Pabari Group.

CFI wanted to find out more about the organisation which prides itself on producing affordable, locally grown sugar. We put some questions to the KISCOL team behind the flagship project of the Pabari Group.

CFI: What are your hopes for the future of your business, and for the industry as a whole?

KISCOL Team (KT): In the immediate future, we plan to increase our sugar production output to 10 percent of the market share. In the long term, our plan is to create a diversified production company where we will be setting up an ethanol distillery, maximising our land bank by adding solar production to our power production — over and above the power generation from bagasse.

We also intend to set up a fertilizer plant and water utility entity by leveraging our water assets. For the industry, we foresee enhanced competition from the millers who have largely set up in the western part of Kenya, and do not have their own “nucleus”. Companies will either be forced to set up on their own or fight over the dwindling raw material.

This threat is coupled with the looming COMESA safeguards. Companies will be forced to innovate or perish. The situation may see increased imports into the country to cover the production gap.

An alternative outcome is that we may see large investors from abroad set up production entities to meet the market demand. All-in-all, the cost of sugar will remain high — which is an incentive to prospective investors.

CFI: What relevant changes to legislation or regulation would you like to see?

KT: The government set up a taskforce to look into legal and policy changes that will enhance the sugar industry. Part of that was the passing of a new Act of Parliament specific to the industry, as opposed to the existing one which covered many crops — and led to ineffective regulation.

The new Sugar Bill is currently with parliament, and this new law is welcome. We hope it will prompt a return of the sugar-development levy, particularly on imports that will go to create a development fund via financing inputs and price stabilisation.

There should also be regulation creating well defined zoning areas to avoid millers poaching one another’s raw materials. We would like a mandate for millers to bring imports into the country, rather than private individuals. This will ensure that the industry ecosystem benefits.

Lastly, we hope to have several tax-policy changes, such as exempting key inputs from taxation, to stimulate investment.

CFI: Can you pinpoint any pitfalls to help newcomers to the industry?

KT: Development of a greenfield sugar project is a capital-intensive endeavour due to our weak and segmented investment laws.

There should be a mechanism of investor protection from development until commercial operations begin. Any new investor should try to seek guarantees from government prior to investing.

CFI: Do you have any anecdotes to illustrate your progress over the years?

KT: When we were setting up the project, land prices within our area we around $500 per acre. As we speak, the price sits at $6,000 per acre; some are close to $10,000. This has created an increased demand.

Another issue is quality of life: the southern coastal region of Kenya has high poverty levels. Through investment, we’ve created employment to 2,000 local people. Money circulation has created many offshoot businesses, like hotels and eateries, rental companies, shopping centres, transport organisations.

We’re happy that as opposed to going to going to the main commercial town for shopping, one can now buy essentials within walking distance of the factory. Our infield roads have opened up many places which had been cut off from main infrastructure.

CFI: How do ESG parameters and sustainability principles affect the way your industry is run?

KT: We fully embrace these parameters and principles. KISCOL has embarked on a number of sustainability efforts. We initiated a clean development mechanism (CDM) project to sell carbon credits on Certified Emission Reductions (CERs) to the Swedish government. This helps Sweden to meet its targets under the Kyoto Protocol of the United Nations Framework Convention on Climate Change (UNFCCC).

We teamed up with CAMCO on the conceptualising, drafting, and completion of the protocols-based CDM. When it was finalised, we were invited to present the project at the UNFCCC’s 17th Conference of Parties (COP17) in December 2011 in Durban, South Africa, through the International Emissions Trading Association (IETA) to the CDM executive board.

KISCOL was nominated for the AfriCAN Climate Good Practice Award in 2013 for its initiatives in adapting to and mitigating climate change in Africa. KISCOL is climate-conscious and ensures that its carbon footprint is minimal. The very nature of our operations means that transport and logistics must be closely inter-twined along our supply chains.

We’ve acquired and introduced a robust vehicle-tracking system that saw a 30 percent reduction in the waste or misuse of company-assigned fuel. This was another step to reducing our carbon footprint. “One step at a time” has been our motto in the quest for sustainability and environmental responsibility.

Most Kenyan factories are dated and old, but there is a trend for companies to confront these issues via legislation, advocacy, and bank financing. The initial cost of compliance is high, but we foresee positive outcomes.

CFI: What are some of the challenges you are facing?

KT: Mid-term challenges revolve around the cost of inputs. The weakening shilling is increasing the overall cost of production. The economic situation here is making the cost of finance higher: banks would rather lend to the government than to the private sector.

CFI: What is the single most important requirement to becoming a global business?

KT: Good governance ensures that the business is run on clear principles. With this you can, over time, build a firm framework to grow beyond your borders. Innovation ensures that you are able to diversify your business, and keep your enterprise competitive and relevant.

CFI: How do you see the short- to mid-term prospects for your industry?

KT: In the mid-term, we foresee the unfavourable shilling-to-dollar exchange rate affecting our purchasing power for critical industry components. Shelf prices will remain high due to the higher average costs of inputs. In the long term, better governmental fiscal policy should reverse this trend.

CFI: What excites you about the business world in general?

KT: The pace of innovation. The world has transformed enormously over a short period of time, and technology has been a key catalyst. What was thought unimaginable by our forefathers is what we experience in our everyday.

CFI: What have you learned over the course of your careers?

KT: The value of people and relationships. Nothing gets done without people.

CFI: What motivates and enthuses you about the business?

KT: The limitless potential and impact that the business can have. From cane, you can have sugar, power, fertilizer, CO2 distillery — all big businesses in their own right. This means that just one crop can have a major impact on society.

CFI: What is special about your organisation’s management style?

KT: We embrace a consultative management style with input from heads of departments and their heads of sections. Information flow is two-way, with input and feedback encouraged from all employees.

CFI: Can you share some management or organisational secrets?

KT: Sugar industry business has been around for generations, so I don’t think any secrets are left. One has just to do what has continually been done, in the best way possible.

CFI: What are the key strengths of your team?

KT: Our businesses are run on values driven by:

- a) Integrity: we conduct business fairly, with honesty and transparency.

- b) Understanding: Caring, showing respect, compassion to our colleagues and customers.

- c) Excellence: We strive to achieve the highest possible standards in the quality of the goods and services that we provide.

- d) Unity: Teamwork, cohesive collaborations, strong relationships based on tolerance and mutual co-operation.

- e) Responsibility: We are sensitive to the cultures of the countries, communities and environments where we operate. Inclusivity marks our operations. We ensure that what comes from the people goes back to the people, and the soil, many times over.

CFI: How important is your support team?

KT: Support teams, in whatever cadre, are critical to improved productivity and effective results. The value of having a team that shares the company mission and vision cannot be overstated. Our support teams shore up the back-end so that the front-end shines. We encourage teamwork, cohesive collaborations, strong work-based relationships based on tolerance, and mutual cooperation.

CFI: What are the key traits of a good corporate leader?

KT: In today’s world, where everyone is to a large extent knowledgeable and has access to information, a leader should first be grounded in his or her understanding of their role. This creates confidence in people.

Secondly, a leader should be able to motivate his or her team to display eagerness and inspiration.

You may have an interest in also reading…

Cement Recycling: a Breakthrough for More Sustainable Construction

Reuse and recycle — it makes sense, even in the most basic steps of the building trade… The global construction

Finding the Inside Track to Sustainable Investment — it’s a ThirdWay Speciality

ThirdWay Partners, with offices in Kenya, London, Mozambique, South Africa and Spain, and expanding its presence in Argentina this year,

More Than a Bank: Banco Azteca as a National Platform for Social Resilience

A financial institution’s value is not proven in moments of calm—it is tested in moments of crisis. Banco Azteca, one