Ernst & Young, Argentina: Tax Reform Affects Stocks and Dividends

On September 23 of last year a law (nr. 26,893) was introduced which significantly amend the Argentine income tax law. It was published in the Official Bulletin.

On September 23 of last year a law (nr. 26,893) was introduced which significantly amend the Argentine income tax law. It was published in the Official Bulletin.

As an introduction, the main amendments are aimed at levying income tax over the sale of shares and membership interests by natural resident persons and parties domiciled abroad, as well as the distribution of dividends earned by those parties.

Part of the amendments introduced by the new law were already known to tax advisors and businesspeople, who were well aware that the income tax exemption over the sale of shares by people and companies domiciled abroad would end soon in view of the continuously increasing tax pressure observed in Argentina in the last few years at federal, provincial and municipal levels.

Main Amendments Introduced

Below is a brief analysis of the main amendments introduced by the law and a particular focus on the two most significant changes affecting mainly transactions arising from the sale of shares and membership interests, as well as dividend distributions:

“The issue becomes more complex when both parties, i.e. the stock seller and buyer, are foreign residents.”

Purchase and sale of shares – natural resident persons:

- According to Income Tax Law, natural persons shall pay taxes over habitual income, while companies shall pay taxes over habitual and non-habitual income.

- In this sense, a significant amendment introduced by the law intends to levy taxes over capital gains in the case of natural persons, stating that they shall pay taxes over income from the sale of shares, membership or equity interests, securities and bonds, among others, and from the sale of depreciable personal property, even when those transactions were not habitual.

- Income from the purchase and sale of shares, membership or equity interests, securities and bonds, among others, shall be subject to a 15% rate.

- However, apart from the taxability of shares, the law established an income tax exemption over income from the purchase and sale or disposal of shares, securities and bonds, among others, listed on stock exchanges and securities markets and/or authorized for public offering.

Purchase and sale of shares – foreign residents:

- Until the law was enacted, natural persons and companies domiciled abroad (foreign residents) were exempted from income tax as to income from the purchase and sale of shares. The law has abrogated that exemption.

- The law has taxed such income at 15%. Below we will make reference to the tax base on which that rate may be applied.

Distribution of dividends:

- According to the law, the distribution of dividends or earnings in cash or in kind (except for shares and membership interests) obtained by foreign residents and natural persons residing in Argentina shall be subject to a 10% withholding.

New Tax Scenario for Foreign Residents

As previously stated, until the law was enacted, foreign residents were subject to an exemption on capital gains obtained upon the sale of shares. In fact, section 73 of, Presidential Decree No. 2284/1991, exempted from income tax income derived from the purchase, sale, exchange, barter, or divestiture of shares, bonds, or any other securities obtained by foreign beneficiary natural or artificial persons. Finally, the law abrogates one of the few appealing tax planning tools offered by Argentina to foreign investors.

As the law becomes effective, foreign residents intending to dispose of their equity interests in Argentina shall pay income tax at a 15% rate. Note that income tax shall be settled through a withholding at source to be paid on a single and final basis.

Now, which is the applicable tax base?

According to the new legislation, any of the following methods may be chosen:

Applying a 15% rate over the 90% presumed income, as established by section 93(h) income tax law, or

Applying the rate at issue over the base arising from deducting from the price paid the expenses incurred in Argentina (including the cost of the shares acquired) by those foreign residents in order to obtain, maintain and keep equity interests, provided that those expenses have been expressly recognized by Argentine tax authorities (actual income).

In the first case mentioned (presumed income), the withholding to be made shall arise from the following formula: Stock sale price x 15% x 90%.

In other terms, the tax shall arise from applying the actual 13.50% rate (15% x 90%) to the sale price of shares and/or equity interests. If, while negotiating, the parties agreed that the stock seller should receive the price free of withholdings, the rate shall be accordingly grossed up to 15.61%.

One significant aspect consists in documenting the withholding assessment and payment to tax authorities. In fact, the issue would not be controversial if the stock buyer was an Argentine tax resident as the new legal provisions could be reasonably implemented.

The issue becomes more complex when both parties, i.e. the stock seller and buyer, are foreign residents.

In this regard, the law states that the buyer of shares or member interests shall assess and pay the tax to Argentine tax authorities. Currently, as this new provision has not been regulated yet, it would not be possible to pay the tax to these authorities. This situation clearly generates doubts and uncertainties because there are several cases in which the parties involved in the transaction are unable to comply with a legal provision, which gives rise to a potential risk upon tax authorities’ intention to impose penalties due to the failure to pay the tax levied on the transaction.

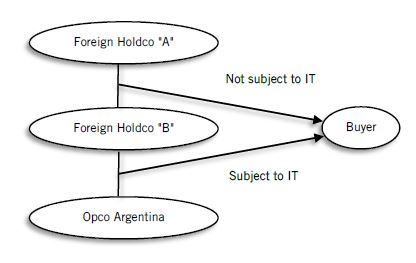

Another aspect to be considered in this new scenario is whether the sale or disposal of indirect equity interests is taxable. Chart 1 will clarify the situation.

Chart 1

The new legislation does not clarify anything in this regard. Consequently, we interpret that, upon the lack of an express provision, income tax shall only be levied on the direct sale and/or disposal of shares and membership interests of Argentine artificial persons. In the particular case of the chart above, the sale of Opco Argentina’s shares by the Foreign Holdco “B” shall be subject to income tax, while Buyer shall pay the tax withheld from the Foreign Holdco “B”. On the contrary, the indirect sale would not be subject to tax.

Note that the law does not expressly extend to foreign residents the exemption to natural persons residing in Argentina and selling listed shares. Consequently, it is not yet clear enough whether the sale of Argentine companies’ listed shares by foreign residents shall be subject to income tax.

Finally, the potential application of double taxation treaties signed between Argentina and the countries in which the stock seller resides shall be analyzed in each particular case in order to evaluate whether: (i) lower rates set forth by the law are applicable, or (ii) those treaties reserve the tax power in the country where the stock seller resides.

Tax on the Distribution of Dividends and Earnings

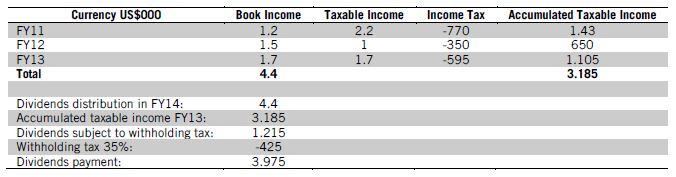

The law introduced a significant amendment to income tax law with respect to dividend taxability. Until the law was enacted, the distribution of dividends was subject to an income tax withholding as a single and final payment known as equalization tax. The name was chosen because the withholding is applied over the distribution of book earnings exceeding accumulated tax earnings. In the event of surplus, it shall be subject to a 35% withholding or treaty rate. The intention of lawmakers upon implementing such taxation method was to prevent shareholders from availing themselves from exemptions set forth by income tax law for the benefit of the companies distributing dividends.

The amount of income subject to the equalization tax to be considered at the time of the distribution of dividends will result from the following calculation:

Amount of dividends – Sum of [Income assessed by income tax law – income tax + dividends and earnings received not computed when assessing such income (i.e. dividends from subsidiaries)].

The table below shows an example of a calculation of the equalization tax on dividends:

As previously mentioned, apart from the so-called equalization tax, Argentine companies (corporations, limited liability companies and, in general, all business companies) shall make a 10% withholding when distributing dividends or earnings to natural persons, whether or not residing in Argentina, and artificial persons residing abroad.

It is still pending to analyze whether the 10% withholding shall be applied to the net dividend amount of the potential equalization tax or the gross amount of dividends. We interpret that such percentage must be applied to the earning to be distributed after deducting the equalization tax amount. However, this conclusion must be ratified by the administrative order to be issued by the executive branch.

The law states that if dividends are distributed in kind, the 10% withholding shall be applied, unless the distribution was made in shares or membership interests (e.g. distribution of bonus shares).

Each particular case should be analyzed as to the application of double taxation treaty provisions in order to understand whether the abovementioned withholding percentage limits are applicable.

Final Thoughts

The new tax provisions have been clearly enacted for collection purposes. There are still many unanswered questions as to the application of the new provisions under the tax reform that we have analyzed. We have become aware of a draft administrative order that would solve part of these questions. We expect the administrative order and other regulatory provisions to be published soon in order to solve these multiple situations. i

About the Authors

Sergio Caveggia and Leonardo Favaretto

Sergio Caveggia (Partner) and Leonardo Favaretto (Senior Manager) are members of Ernst & Young’s Transaction Tax Department.

You may have an interest in also reading…

Christoph D Kauter: Leading Beyond Capital Partners with Vision and Purpose

Christoph D Kauter, Founder and Managing Partner of Beyond Capital Partners, has built a career that blends entrepreneurial vision with

Cube Labs: Transforming Scientific Discovery into Scalable Healthcare Innovation

Italy-based Cube Labs is redefining healthcare venture building by bridging the gap between academic research and global markets—delivering measurable social

The Ultimate Investment Pitch: How to Win Funding on Conviction, Not Cash

Forget glossy decks and expensive consultants. Capital is not secured through ornamentation, but through belief. The strongest pitches are built