Global Banking Alliance for Women – GBA: Banking the Female Economy

Inez Murray

Inez Murray is the CEO of the Global Banking Alliance for Women, a global consortium of financial institutions driving women’s wealth creation. Its 34 member banks work in 135 countries to build innovative, comprehensive programs that provide women entrepreneurs with vital access to capital, markets, education, and training.

CFI: What is the Global Banking Alliance for Women?

Inez Murray: It’s a consortium of banks with programmes and services directed at women. These banks have specific strategies that target women, both as owners of small and medium enterprises and as consumers. Our goal is to make targeting the female economy a mainstream strategy for banks. This will not just advance women’s financial inclusion but will also benefit the estimated eight to ten million very small, small and medium enterprises that are owned by women worldwide.

CFI: Can you please tell us a bit more about the female economy? Why should banks reach out to women?

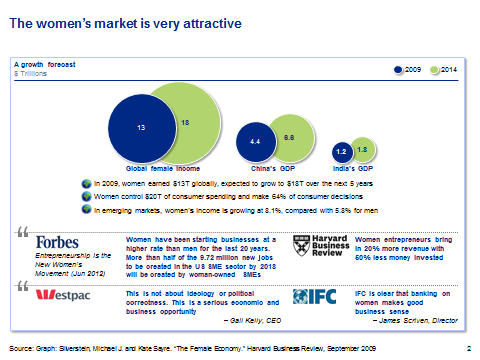

Inez Murray: Women are currently the biggest growth market in the world. According to a study recently published in Harvard Business Review their earnings are expected to reach $18 trillion globally in the next few years – bigger than the economies of China and India combined. A study by Goldman Sachs shows that women make the majority of household decisions as they relate to the welfare of the children. So for example in the UK, you’re talking about women making 85% of the decisions over kid’s clothing, 80% over food, and 70% over childcare and schools. Women represent a major market opportunity for many corporations – and not just those in the financial sector. In the US, women-owned businesses are growing at a faster rate than their male-owned counterparts do. But there’s also a $300 billion credit gap for women-owned SMEs, particularly in the Middle East, Africa and Latin America.

CFI: How are data analytics changing the way banks reach the female economy?

Inez Murray: At GBA, we’re basically building the business case for the female economy by getting data from our members on performance. For example, Westpac is an Australian bank with one of the oldest women’s market programmes, and certainly one of the most successful. They reach 2.6 million Australian women, representing an $97 billion market opportunity. And they are actually able to disaggregate their database to show performance statistics, such as women generating higher savings balances in their accounts. Women generally pay back loans at a better rate than men do. Garanti Bank, the second largest bank in Turkey, has found that the proportion of non-performing loans is 50% lower for women-owned businesses than it is for those owned by men, and that the bank’s cross-selling to women is 2.5 times more effective.

CFI: What is “pink washing?”

Inez Murray: Pink washing is claiming to have a gender programme or women’s market initiative, without this really being so. It’s a bit like green washing. For example, we know of a bank with a women’s programme which solely consists of a credit card with a mirror on one side. But there’s nothing in their programme which really benefits women. It’s important to develop a greater understanding of this market but also to develop the metrics to really measure effectiveness. That way, we can ensure that banks don’t get away with pretending they have programmes oriented toward the female economy.

CFI: What do banks need to do to reach women?

Inez Murray: First, they need to understand the market opportunity, including the segments within the female market. So at minimum, we’re talking about SMEs and consumers. Banks typically segment the consumer market by income. On the SME side, you sometimes segment by annual revenues and sometimes by phase of business: Start-up, growth, and expansion phase. Banks need to understand the needs of the segments they serve and create a value proposition for their customers. Next, they need a senior champion inside the bank, who’ll be behind the initiative. And from a delivery and cost perspective, banks need to figure out what they should do themselves and what they should outsource. In many cases we see banks forming strategic alliances with educational institutes, women’s organizations, etc. rather than developing educational programmes themselves.

What we’ve learned from best practices in our network is that women need access to information in order to make decisions. So this isn’t a simple product fix. In fact, it’s rarely about the product; it’s about the execution. For example, women generally need support in improving their levels of financial literacy. Women come in looking for loans as SME owners but often don’t have financial statements prepared.

They also need access to networking opportunities, so most programmes combine educational events with networking. That way, women can network with each other, generate business opportunities, and learn from each other. In some cases, we have programmes that link women clients to market opportunities. Some banks work with corporations to develop supplier diversity programs, making an effort to procure from women-owned SMEs.

For the latest news about banks targeting the women’s market: http://www.gbaforwomen.com/newsletters/current/

GBA Data Analytics: Key Lessons and Results

Data Collection

Although a majority of banks capture the gender of customers, many are not disaggregating data by gender (either because of IT challenges or because they do not understand the importance). In a just released banking survey in Latin America, the Inter-American Development Bank found that half the banks surveyed do not know the gender composition of their SME lending portfolio. Of those that do collect such information, only 28% use it.

By contrast, in a survey conducted by the Global Banking Alliance for Women [GBA members include 34 banks operating in more than 135 countries.] of its members, 80% are disaggregating data by gender. There is strong buy-in on serving the women’s market across its membership. Tracking performance is key to building and maintaining the business case.

Defining women customers can be complicated. This is true for women as consumers as well as business owners. Since many accounts are jointly owned, emerging best practice is to categorize accounts as belonging to women if the woman is the primary account holder. It gets more complicated for SMEs. In the GBA survey, we found that there were a number of variations in the definitions used for women SMEs (for instance, some banks define the gender by accountholder others do so by the ownership percentage of business, by management, or use a combination of these definitions).Use of Data

GBA members reported using a wide variety of sex-disaggregated measures:

80% of respondents track women SME outreach indicators; 70% track risk levels by gender; 60% track product diversity metrics; and 50% track profitability of their women’s market programme.

Many banks are using more complex customer satisfaction measures that allow them to measure how well they are serving women. For instance, some banks use Net Promoter Scores (NPS), disaggregated by gender, to measure the advocacy rate of both female and male customers as this is a known driver of profitability. They are then able to compare NPS in the market with their main competitors. Products per customer, disaggregated by gender, is an important measure that is also being used.

Some banks use a share-of-wallet measure, which allows them to quantify how much of the household expenditure is being allocated to financial services and to which bank specifically.

Diversity and inclusion measures are widely used and reported by GBA members. We found that 90% of GBA members are tracking women’s staff and management ratios, while 60% are tracking staff promotion and attrition rates by gender.

Social metrics are the least commonly tracked and used by banks. However, many of the current operational and financial metrics tracked by the leading banks are very effective tools for understanding customer needs, behaviour, and aspirations.Reporting

GBA banks seem to be using women-focused metrics mostly for business optimization purposes, but some do report them publicly and to their board.

There is an opportunity to influence external stakeholders which may exert pressure to introduce regular reporting of women-focused metrics.Challenges in Tracking Gender-Disaggregated Indicators

A majority of respondents stated that the inadequacy and inefficiencies of systems posed a major challenge.

Other challenges included understanding how to define women owned SMEs, the inability to distinguish between business and personal data, and the lack of awareness about gender-disaggregated data.

Although most banks stated that they disaggregate data by gender, some considered this to be a major challenge.

Sharing of best practice on data collection and metrics, and support in increasing awareness on the importance of gender-disaggregated data among senior management, were factors widely cited in the survey as needed by member banks.Data Analysis – Building the Business Case

In recent interviews with banks (GBA members and non-members) on the barriers that are faced in serving the women’s market, the GBA found that 80% of the interviewees believed that proving the business case is a key barrier for banks. Many banks also cited segmenting their customer base as a key challenge.

To build its case, the GBA conducted deep-dive analysis with some of its members and found a strong quantitative case for serving women as a distinct customer segment

In our analysis of a select number of GBA members, we found that:

In most cases the risk profile of women is lower than that of men (lower non-performing loans across segments);

Women loans are more profitable (higher return on assets and higher profit margin);

Women tend to have robust balances in their savings accounts, more consistently than men do.

With a women’s market program, some banks are able to grow their women customer base at a level that is twice the rate of men’s;

In established programmes, women’s loyalty and advocacy (as measured by Net Promoter Scores) is higher than men’s.

You may have an interest in also reading…

Driving Through the Storm: How Ford Avoided a Bailout and Steered Towards the Future

The 2008 financial crisis brought the American auto industry to the brink of collapse. While General Motors and Chrysler relied

Raiffeisen Certificates: Investing in Capital Markets — with Protection

No one wants unnecessary risk — least of all Austrians, who traditionally display caution when investing in capital markets… Raiffeisen

Ten Recent Technology Advances That Asset Allocators Should Have on the Radar

A CFI.co briefing on the engineering breakthroughs, grid innovations and early deployments that are compressing cost curves and reshaping the