FMO: Unlocking Scale Potential of Green Bonds in India – Lessons from Global Markets

Chief Investment Officer: Linda Broekhuizen

The global green bonds market has gone from strength to strength in recent years, with issuance for 2017 already exceeding $100bn, some $20bn more than the total issuance in 2016 and the first time this benchmark has been breached.

According to the Climate Bonds Initiative (CBI) State of the Market report 2017, “the climate-aligned bond universe now stands at $895bn outstanding – a jump of $201bn from the 2016 figure. This total is comprised of unlabelled climate-aligned bonds at $674bn and labelled green bonds at $221bn.”

This is an impressive figure but pales into insignificance compared to the $90tn total worth of global bond markets. And the $100bn annual issuance also needs to be measured against the OECD’s estimate that to keep average temperature rises below 2°C, $800bn must be invested every year to 2020 in renewable energy, energy efficiency, and low-emission vehicles alone.

Green bonds are debt instruments whose proceeds are being used to finance low carbon and climate resilient infrastructure/assets. They will be a crucial tool in financing the decarbonisation of the global economy that will be necessary to meet the targets of the Paris Accord and limit average temperature rises to well below 2°C. Of the green bonds issued so far, 80% of the proceeds have gone to the transport and energy sectors.

The first issuers were multilateral development banks such as the World Bank, the International Finance Corporation, the European Investment Bank, and the Asian Development Bank. They continue to be the largest issuers, but they have been joined by issuers from countries including the USA, China, a number of European nations, India, and Brazil. France recently became the second nation to issue a sovereign green bond, after Poland and Fiji became the first emerging market sovereigns to do so. Nigeria is expected to become the first African sovereign issuer before the end of 2017.

“Green bonds will be a key tool for financing climate resilient infrastructure in cities, more of which are expected to implement green bond programmes in future.”

Sub-sovereign bond issuers such as New York City and Cape Town have also joined the party. Some 70% of global greenhouse gas emissions come from cities, and many of the world’s most populated cities sit on coastlines, rivers and flood plains. For this reason, they are particularly vulnerable to negative impacts from a changing climate. Green bonds will be a key tool for financing climate resilient infrastructure in cities, more of which are expected to implement green bond programmes in future.

At the same time, issuance from corporates and commercial banks has grown. Many banks are stepping up to the challenge – banks such as HSBC, Barclays, and Bank of America have all made $1bn-plus commitments to issue green bonds. These commitments often fit into wider green financing programmes – JPMorgan Chase, for example, said this year that it wants to facilitate $200bn of green financing by 2025, while Goldman Sachs, Bank of America, and Citi have pledged to invest $150bn, $125bn and $100bn respectively.

Watch the video here:

Room to Grow

However, says the CBI, when it comes to green bonds, the market has fantastic growth potential because demand from institutional investors continues to outstrip supply. “There is significant headroom for more quality green issuance, particularly from banks and corporates. Increasing bank-based and corporate issuance is now a vital component in meeting climate finance targets & country climate plans.” Corporate issuance is growing – S&P Global Ratings reports that the sector tripled last year to $28bn and the CBI says $32.6bn of corporate green bonds were issued in the year to the end of October.

In September 2017, State Bank of India announced that it planned to take advantage of this demand by raising up to $3bn in the country’s biggest overseas green bond issue.

FMO’s Experience

FMO is the Dutch development bank and has been investing in the private sector in developing countries and emerging markets for almost half a century. With a committed portfolio of €9.0bn, FMO is one of the larger bilateral private sector development banks globally, with investments in more than 85 countries. FMO has strongly embraced green and sets ambitious annual targets to grow the green asset base. FMO partners with institutions like India’s YES Bank, who have also embedded the theme in their core strategy and contribute strongly to a greater awareness of the topic and its business potential.

In May 2017, FMO successfully priced its third EUR Sustainability Bond, a 6-year €500m transaction that attracted more than fifty investors. The proceeds will fund projects aimed at climate change mitigation (renewable energy and energy efficiency) and climate change adaptation, as well as inclusive finance projects (microfinance and SME financing). It followed a debut €0500m issue in 2013 and a second one for the same amount in 2015. More than a third (36%) of FMO’s eligible asset portfolio is in Asia, with India the biggest market at 13% of this portfolio. Most of FMO’s renewable energy investments in the country are in wind and solar power projects.

India’s Market Ripe for Expansion

India is one of the top ten global green bond markets and, according to the CBI, “to date, Indian issuers have been leaders in demonstrating best practice by having most labelled green bonds receive a review or certification from an external body”. Having bonds certified by external parties has been instrumental in ensuring international investor confidence in the green credentials of the Indian green bond market.

India is one of the top ten global green bond markets and, according to the CBI, “to date, Indian issuers have been leaders in demonstrating best practice by having most labelled green bonds receive a review or certification from an external body”. Having bonds certified by external parties has been instrumental in ensuring international investor confidence in the green credentials of the Indian green bond market.

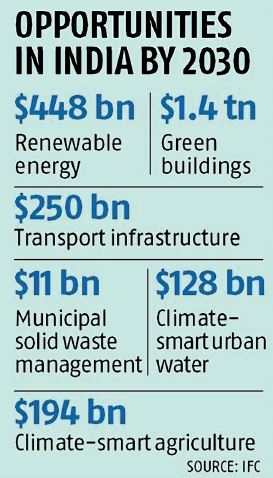

As banks’ balance sheets are becoming increasingly constrained by sector exposure limits and capital ratio requirements, we expect capital markets to play a bigger role with the investments of $2.5tn required to meet India’s 2030 climate change mitigation targets, of which around half from the private sector. “There are many bond issuers who could easily be issuing green bonds,” says the CBI. “For example, India rail bonds would qualify. Investor demand for green products is growing, the potential now exists for India to attract significant international capital via a robust green bond market to meet national climate and development goals.”

However, the market remains in its infancy, with both issuers and investors still unsure of the benefits of green bonds, says Linda Broekhuizen, FMO’s chief investment officer. The market is also held back by the lack of a local currency market – just a small fraction of the market is denominated in rupees, in part because local investors have yet to embrace green bonds and in part, because many potential foreign investors are not able to take rupee exposures. It appears that local investors do not have any meaningful green targets yet. If such targets were to be put in place, this could significantly boost green bond issuances and ultimately the greening of the economy.

One concern investors may have is that by buying into a green bond they will be sacrificing yield, but that is a misplaced fear, Mrs Broekhuizen adds. “While in certain smaller markets, concessional funding may go to green investments and drive overall pricing/yield down, the Indian market is too big for such an effect. With international investors focusing more heavily on green issues, it is likely that more and more funding will flow towards green bonds, which should then lead to pricing efficiencies for the issuers in the future.”

But for the Indian green bonds market to grow, it needs a favourable environment, with the right regulations and incentives in place, along with transparent rules and principles, she explains.

Green bonds currently face restrictions that do not apply to project financing, for example, while foreign investors face additional hurdles if they want to invest in India. To illustrate, currently foreign investors need to go through an auction in order to get an investment limit allocated. Whether or not a limit will be available and at which price, leads to a high level of uncertainty. If this specific barrier, and others, were reduced or removed altogether for green bonds, it would boost investment in the green bond sector significantly.

Mrs Broekhuizen further adds that green should not be misconceived as being restricted to renewable energy. The scope can be, and is, much larger and extends to green vehicles, energy efficient offices, household equipment, and so on. The opportunities are out there.

Lessons from China?

A comparison with China is instructive – CBI ranks it as the top “climate-aligned bond” country, responsible for more than 80% of green bonds in Asia, with issuance of more than $300bn compared to less than $25bn for India. Growth has come quickly – the country issued a negligible amount in 2015 yet is the joint leading green bond issuer for 2017, alongside France and the US.

Much of this comes down to strong government backing linked to the country’s commitment to peak CO2 emissions by 2030 at the latest, lower the carbon intensity of GDP by 60%–65% below 2005 levels by 2030 and increase clean energy to around 20% of the total.

“There is a strong government programme to invest in green initiatives, specifically via the larger state-owned banks,” says Mrs Broekhuizen. The private sector can build-on the groundwork laid down by such public programmes, she adds.

India has its own ambitious targets to cut emissions and decarbonise its economy, and green bonds can play a huge part in meeting those goals. The sustainable investor base is slowly but surely expanding, and investor appetite will increase further if India aligns its financial sector more with international best practice.

In this regard, there are already encouraging signs of progress. The Indian Green Bonds Council was formed in 2016 and this year the Securities Exchange Board of India (SEBI), the corporate regulator, released guidelines for listing green bonds that will bring greater transparency and certainty to the Indian green bond market.

With the imperative of tackling climate change, air pollution, and other sustainability issues, a positive policy environment and strong government support, India’s green bond market is well-placed to thrive in years to come.

FMO: Pushing the Green Envelope

Based on an interview with Linda Broekhuizen

Linda Broekhuizen, CIO of FMO, at FMO headquarters in The Hague, Netherlands

Its name – Platform Carbon Accounting Financials (PCAF) – lacks a certain je ne sais quoi, but its intentions are beyond reproach. For the first time, twelve banks have agreed to a single methodology for measuring the carbon footprint of their investments and loans. It took two years to hammer out the formula which is deemed crucial for gauging the environmental impact of financial services providers and for determining trends. The data also allow banks to fine-tune their policies and develop more effective strategies.

PCAF is an initiative of twelve Dutch banks, pension funds, insurers, and asset managers. The platform originates from the Dutch Carbon Pledge signed at the 2015 Paris Climate Change Conference and is open to new members. The investment management arm of insurance company Achmea joined last year. PCAF enables financial services providers to set targets and monitor compliance and progress. The measurement of the financials’ carbon footprint is, however, merely a means to an end: the decarbonisation of investment and loan portfolios in line with the Paris Cop 21 Agreements on Climate Change.

In its first report, released in early-December, the platform presented an enhanced measuring model that includes government-issued bonds, project finance, mortgages, listed equities, and corporate financing. The method assigns the carbon emissions of any given undertaking proportionally to stakeholders.

PCAF expects its methodology and data to set industry-wide benchmarks. The platform hopes to engage the country’s large pension funds – jointly managing a staggering €1.7tn in assets – which have been slow in developing carbon accounting practices. PCAF differs markedly from other initiatives to assess the role of financials in climate change inasmuch as the platform measures impact only and does not quantify risk.

One of the largest private sector bilateral development banks in the world, MFO (Netherlands Development Finance Company) is a founding member of the PCAF and enjoys a reputation for pushing the green envelope. The bank has been doing so for half a century. FMO sustains some €9bn in investments in 85 countries and was one of the first to decisively move towards the greening of its portfolio. Last year the bank issued its third sustainability bond, attracting over fifty investors who put in €500m. The funds raised are earmarked for climate mitigation and adaptation projects. Part of the resources will also be leveraged to support financial inclusion initiatives.

Over a third of FMO’s investment portfolio is deployed in Asia with India representing the bank’s largest market. FMO has partnered with YES Bank to promote environmental awareness and explore green business opportunities.

Whilst India needs around €2tn in investments if the country is to meet its 2030 climate change targets, the market has not yet reached maturity, according to FMO Chief Investment Officer Linda Broekhuizen: “Local investors have not yet embraced green targets and foreign investors are not comfortable, or able, to take on rupee exposure. Once gwreen targets are put in place, and a transparent legal framework has been erected, green bonds will become much more common in India.”

Mrs Broekhuizen is, however, adamant that green bonds do not sacrifice yield: “While in certain smaller markets, concessional funding may go to green investments and drive overall pricing/yield down, the Indian market is too big for such an effect. With international investors focusing more heavily on green issues, it is likely that more and more funding will flow towards green bonds, which should then lead to pricing efficiencies for the issuers in the future.”

About the FMO

FMO is the Dutch development bank. As a leading impact investor FMO supports sustainable private sector growth in developing countries and emerging markets by investing in ambitious projects and entrepreneurs.By reaching out to underserved markets, we invest in some of the world’s most challenging business environments. The countries that we work in often have a fragile private sector, little job security and high poverty rates. FMO believes that a strong private sector leads to economic and social development, and has a more than 45-year proven track record of empowering people to employ their skills and improve their quality of life. FMO focuses on three sectors that have high development impact: financial institutions, energy, and agribusiness, food & water. With a committed portfolio of EUR 9.0 billion spanning over 92 countries, FMO is one of the larger bilateral private sector developments banks globally. For more information please visit www.fmo.nl. This article has previously been published in CFO Insights.

FMO is the Dutch development bank. As a leading impact investor FMO supports sustainable private sector growth in developing countries and emerging markets by investing in ambitious projects and entrepreneurs.By reaching out to underserved markets, we invest in some of the world’s most challenging business environments. The countries that we work in often have a fragile private sector, little job security and high poverty rates. FMO believes that a strong private sector leads to economic and social development, and has a more than 45-year proven track record of empowering people to employ their skills and improve their quality of life. FMO focuses on three sectors that have high development impact: financial institutions, energy, and agribusiness, food & water. With a committed portfolio of EUR 9.0 billion spanning over 92 countries, FMO is one of the larger bilateral private sector developments banks globally. For more information please visit www.fmo.nl. This article has previously been published in CFO Insights.

You may have an interest in also reading…

The Intelligent Framework: Why Lenovo’s Governance Leads the Asia-Pacific Tech Wave

In the global technology sector, where innovation cycles are compressed and disruption is constant, corporate governance has become a decisive

The Midas Touch, or Not So Much? The Mythical Metal vs Shares

Gold is the age-old standard that once underpinned our modern currencies; what value does it have in physical form? In

From Penetration to Inclusion: How CRC Credit Bureau Is Re-Engineering Nigeria’s Credit Ecosystem

Nigeria’s journey towards broad-based financial inclusion has accelerated markedly in recent years, with credit penetration emerging as one of the