PwC Africa: Africa’s Finance Leaders Take Steps to Ensure the Safety of Workers

As lockdown regulations are eased all over the world, business leaders are recognising that they have a critical role to play in the safety, health and stability of their employees and customers.

While business leaders implement new policies and processes to bring employees back into the workplace and engage with their customers, they are realising the physical workplace and customer experience will no longer be the same as it was prior to the global COVID-19 pandemic. Many companies have weathered the immediate crisis by implementing safety measures, transitioning to remote work and other new ways of working, and considering what they need to survive and thrive moving forward.

Since March 2020, PwC has been tracking sentiment and priorities among finance leaders about the COVID-19 pandemic. We surveyed 989 CFOs from 23 countries during June 2020, including 41 CFOs from nine countries in sub-Saharan Africa (SSA). This survey is the fifth in a rolling series. We continue to add territories and companies to offer a robust view of how the crisis is affecting people and businesses worldwide.

When we initially commenced with our survey, almost half of CFOs were concerned about the impact of the COVID-19 pandemic on their business. At that time, many companies were in the early stages of crisis response, not yet thinking about strategies and plans for recovery. Currently, most lockdowns have been lifted around the world as leaders of nations and companies accept that economies will reopen and ultimately operate alongside a virus that remains a constant threat.

The pandemic took hold in some African countries as late as May, while others were already in lockdown by late March. Whichever phase they find themselves in, the economic fallout of the pandemic is still widespread, and the stabilisation waves of countries’ responses is likely to be long. The World Bank projects that economic growth in SSA will contract to between -2.1 percent and -5.1 percent, which will result in the region’s first recession in the last 25 years.

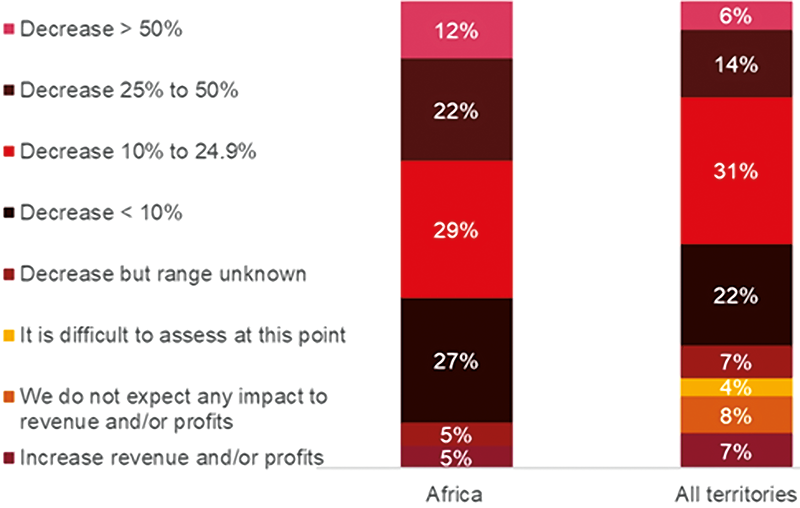

Question: What impact do you expect on your company’s revenue and/or profits this year as a result of COVID-19? Africa vs All Territories.

Source: PwC, COVID-19 CFO Pulse, June 2020. Base: Global – 989. Africa – 41.

Decline in revenue is the reality for most businesses. CFOs’ expectations of a decrease align with their concerns about the global economic downturn and financial impact, and with key economic indicators. Against this backdrop, 34 percent percent of African CFOs (compared to 20 percent globally) expect a reduction in revenue this year of 25 percent or more.

Many African countries implemented containment measures to flatten the infection curve due to capacity concerns of their healthcare systems. These containment measures, however, have tended to deepen the economic recession curve at the same time, putting pressure on businesses to generate revenue and/or profits in the immediate future.

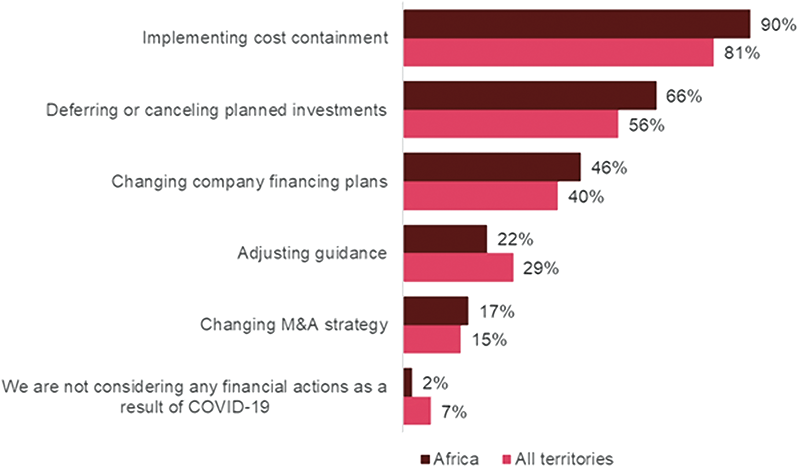

Cost Containment a High Priority

As companies settle into stabilisation, cost containment is a favoured strategy among CFOs, with 90 percent of African CFOs (compared to 81 percent globally) implementing cost containment measures and 66 percent (compared to 56 percent globally) either deferring or cancelling planned investments. Other cost alleviation actions, such as changing financing plans, adjusting guidance and changing M&A strategy, remain on the table for a minority of respondents.

“Companies are being judged on the character they’re demonstrating right now, and their actions or inaction today are sure to count for or against them in the future.”

It is notable that fewer CFOs today than in past CFO Pulse Surveys said they would consider cancelling or deferring investments in R&D. This is positive, given survey respondents’ belief in the importance of developing new products and services. Similarly, with an eye towards what measures will be needed to succeed in the post-crisis world, only seven percent of African CFOs are considering deferring or cancelling investments in digital transformation. Only 11 percent of African business leaders say they are likely to cut investments in customer experience and notably none are targeting cybersecurity or privacy.

Community Focus and Social Engagement

Many companies have already responded to the needs of local communities affected by the pandemic, and the measures taken to manage it. It is positive to note that more than half of African respondents (56 percent) say their companies have increased community and societal efforts with financial or other contributions to non-profits, or pro bono goods and services.

It is increasingly clear that corporate responsibility programmes are being recognised as fundamental. In these difficult times, it is important for companies to engage their people in determining consequential community impacts and being part of the solution, such as retraining the unemployed or creating new job opportunities.

Business leaders will also want to think about how to share their story around these efforts, including how their companies invested in employees and communities and innovated during the crisis. Companies are being judged on the character they’re demonstrating right now, and their actions or inaction today are sure to count for or against them in the future.

Question: Changes in which of the following will be most important to rebuilding or enhancing your revenue streams?

Source: PwC, COVID-19 CFO Pulse, June 2020. Base: Global – 989. Africa – 41.

COVID-19 and New Ways of Working

Most CFOs (Africa 76 percent; global 75 percent) are making plans to change workplace safety measures and requirements. Not all staff, however, will be returning to physical work sites. More than half of CFOs (Africa 68 percent; global 50 percent) indicated that they will take steps to accelerate automation and new ways of working. In Africa, 63 percent (compared to 52 percent globally) of CFOs stated they would consider making remote working a permanent feature for roles that allow it.

In addition, 83 percent of African finance leaders (compared to 74 percent globally) said they were “very confident” in their companies’ ability to provide a safe working environment, and 78 percent (Global 79 percent) were also “very confident” of meeting customers’ safety expectations.

To sustain these gains, businesses will also need to consider the tools, behaviours and incentives that will enable employees to be productive, collaborative and creative — and invest in areas that have the most impact.

A Renewed Focus on Innovation

Along with decisions about cutting investments, African CFOs are evaluating the other changes they’ve made to help manage the crisis. Many cite work flexibility (Africa: 78 percent; global: 75 percent), technology investment (Africa: 71 percent; global 58 percent) and better resiliency and agility (Africa: 80 percent; global: 65 percent) as crisis-driven developments that will improve their companies in the long run.

Around the world the pandemic has underscored the need for new skills, including empathetic leadership, resilience and agility, collaboration and digital skills, and technical and trade skills such as design, manufacturing, and cyber and supply chain management.

Many companies will find there is much work still to be done. According to our 23rd Annual Global CEO Survey, 2020 (conducted prior to the coronavirus crisis in September and October 2019), only 20 percent of global CEOs felt their programmes were very effective at reducing skills gaps and mismatches. Among African CEOs, that figure was 15 percent. Many leaders will clearly need to step up efforts and initiatives in this area to ensure that their technology investments continue to benefit the company and that the resilience they created is built to last.

Africa’s finance leaders are shifting their focus to a more prolonged recovery period. Ensuring a safe workplace is a priority as economies all over the world reopen. Stabilising supply chains also remains critical to ongoing business continuity.

As new recovery milestones are reached, we will continue to monitor how business leaders react and respond.

About the Author

Author: Dion Chango

PwC’s Africa region extends across three market areas: Southern Africa, East Africa and West Africa. Dion Shango was appointed as PwC’s new Africa CEO in 2019, following an election process in which some 400 PwC Africa partners across the continent participated.

Since being admitted to the partnership in 2008, Shango has led engagements on complex and multinational businesses and has serviced a number of large listed clients, mostly within the mining industry. He has extensive experience reporting under IFRS and of financial reporting in the mining industry.

He has also enjoyed exposure to other sectors and industries throughout his career, by virtue of being involved in the audits of companies and organisations such as the South African Reserve Bank, Vodacom, and Montecasino.

In recent years, Dion Shango’s client base has included Exxaro Resources Limited, Harmony Gold Mining Company Limited and Sasol Oil.

You may have an interest in also reading…

The Midas Touch: Physical Gold vs Gold Shares

Gold: A Hedge Against Uncertainty Gold has long been considered a safe haven in times of economic instability. As Forbes

Leading The Next Cycle: NSE’s Trust-First Agenda For India’s Capital Markets

NSE frames its leadership agenda around a single, organising idea: India’s capital markets must scale without losing stability, fairness, or

The Middle Power Dilemma: The UK and the Sovereignty Paradox in a Tri-Polar World

The hypothesis is simple. In a trade system increasingly shaped by the United States, China and the European Union, a