Business in Times of Corona: A Gathering Storm Darkens the Prospects of Africa

South African President Cyril Ramaphosa

Even before the corona virus made its presence known, market analysts had no need for prescient powers to predict trouble ahead for South Africa. Already in February, consumer and business confidence had approached a 30-year low as the country’s anaemic economy hobbled from one recession to the next. The reforms announced by President Cyril Ramaphosa in 2018 to reboot a state hollowed out by rampant corruption have so far failed to materialise largely due to the reluctance of the ruling ANC to update its dark view of private business.

Insofar as the party still clings to a philosophy, as opposed to naked power, it tends towards a highly regulated, centralised, and nationalist model that favours the state as the primary driver of development. Whilst President Ramaphosa seems aware that previous policy recipes have utterly failed to yield the desired results, and must now be ditched, his administration cannot act decisively until the ANC climbs on board.

The 2020 budget, unveiled mere days before the first corona cases were reported, offered a fig leaf of sorts to the party: Finance Minister Tito Mboweni assured all and sundry that the government will not ‘pursue the path of austerity’ and instead proposes to implement its reform agenda incrementally. As a first step, Mr Mboweni explained that the public sector wage bill is to be cut by $10.5 billion over the next three years. The government will also seek to stem the losses at state-owned South African Airways and power utility Eskom, both long-plagued by mismanagement and haemorrhaging cash.

The absence of bold moves to tackle the crisis, and the expected impact of the corona pandemic, led Moody’s to downgrade the country’s sovereign credit rating to junk status (Ba1 negative). Moody’s was the last of the major rating agencies to do so. It cited the continued deterioration in fiscal strength and structurally weak growth as the prime reasons for depriving South Africa of its prized investment-grade rating. The agency also pointed to the growing debt-to-GDP ratio, fast approaching 90%, as a cause for concern. Finally, Moody’s expects the ‘unprecedented deterioration’ of the global economic outlook to exacerbate South Africa’s fiscal challenges and complicate the emergence of effective policy responses.

Now under a 21-day lockdown, and with its economy grinding to a halt, the country seems at a loss over the next steps to take. Over the weekend, local analysts warned of a gathering storm: “Hold on to your hats,” advised Bianca Botes of Peregrine Treasury Solutions who fears a major selloff of rand-denominated paper that could result in $11 billion leaving the country, subjecting the already strained currency to additional downward pressure.

Business Unity South Africa (BUSA), the largest and arguably most vociferous of the country’s employers’ associations, on Saturday released a statement that deplored the ‘unfortunate’ timing of Moody’s downgrade and warned that higher interest rates will hamper the business ventures that are needed to promote ‘inclusive’ economic growth. BUSA also noted that South Africa is about to embark on a ‘hard journey’ that will take many years to complete.

Meanwhile, trade union federation Cosatu calls for a stimulus package to limit the social damage as the country deals with the pandemic. Cosatu spokesperson Sizwe Pamla said that an ‘economic firestorm’ looms and asked both the government and the private sector to intervene ‘aggressively’.

Nearly all principal actors agree that the present crisis is much more dangerous than the previous one. In 2008, South Africa boasted a budget surplus and registered strong economic growth which allowed the country to avoid a downturn and insulate its economy from the global malaise. Though GDP dipped to minus 1 percent in 2009, it bounced back the next year and kept growing nicely until 2013 when the average pace of 3 percent annually started tapering off.

Whilst growth dissipated, the national debt rose from about 25% of GDP in 2008 to 58% last year. Late February, the National Treasury forecasted a budget deficit of 6.8%, the largest in 28 years, by the end of the fiscal year in March 2021. Disconcertingly, these bleak numbers do not take into account the effects of the corona pandemic. “We’re starting off this crisis in a far worse position than we started off the global financial crisis,” says Chief Economist Johann Els of the Old Mutual Investment Group.

There is, however, a possible silver lining to be found in President Ramaphosa’s renewed determination to use the pandemic to press home the urgent need for structural reform. On Monday, Finance Minister Mboweni was told to go ahead with the reform agenda and do what is necessary to restore investor confidence. Mr Mboweni spoke of a ‘hallelujah moment’ and said that a new unit will immediately be set up – pointedly not at the National Treasury – to prepare the ground and propose a raft of quick and targeted measures to kickstart the economy. Pundits immediately wondered if the president’s newfound determination is shared outside his own faction in the ANC and if the setting up of a commission is enough to allay concerns.

Minister Mboweni suggested that the country may ask the World Bank and International Monetary Fund (IMF) for assistance in meeting the escalating cost of public health interventions. However, he emphasised that the country does not yet need financial support and will not be asking for a wider IMF bailout. Commenting on Moody’s downgrade, Mr Mboweni said that the move provides a renewed impetus to implement the structural reforms he has long been pleading for.

Meanwhile, the IMF has boosted its emergency lending facilities by an additional $50 billion, including $10 billion on generous concessional terms for low-income countries. The fund is particularly worried over the triple threat faced by the countries of Sub-Saharan Africa as the pandemic spreads. Abebe Aemro Selassie, head of the IMF’s African Department, writes that the growth outlook for the region will be significantly lower with government revenues declining just as spending needs mount. Mr Selassie warns that measures to curb the spread of the virus will have a direct impact on local economies. He also expects demand for African exports to fall in tandem with investments. Finally, Mr Selassie points to the sharp drop in oil prices which will severely hurt exporters such as Angola and Nigeria.

So far, the IMF has received requests for emergency financing from 20 countries and expects another 10 to follow shortly. The African Development Bank (ADB) is also ready to offer help and last week successfully placed its largest-ever social bond, raising $3 billion to help fight the corona virus. Bids amounted to $4.6 billion, prompting the ADB to mull additional issues. The bank noted strong interest particularly amongst socially responsible investment funds and central banks. The 3-year bond was offered at a modest 0.75 percent interest rate.

You may have an interest in also reading…

Lord Waverley: Africa Enters an Age of Optimism

The upcoming UN General Assembly (UNGA) in New York presents an opportunity for world leaders to assess the drivers of

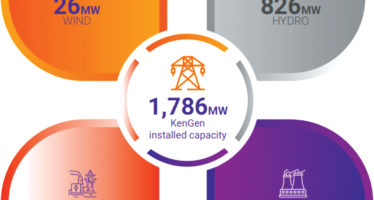

KenGen Powering East Africa’s Clean Energy Future

Kenya Electricity Generating Company PLC (KenGen) stands as East Africa’s leading power producer, entrusted with the mandate to develop, manage

Sango Capital: Reframing Africa’s Investment Landscape for a New Global Cycle

As global capital seeks diversified growth and risk-adjusted returns, Sango Capital reaffirms Africa’s position as a compelling frontier. From shifting