UNCDF: A Roadmap for Financial Inclusion

South Africa

Nephathli is a man from Lesotho, formerly a mineworker in South Africa. His family’s main source of income is the profit made on the sale of chickens and eggs. Nephathli’s income varies from month to month depending on how many eggs or chickens are sold. His children are trying to make a living. However, they are struggling to find a stable income leaving Nephathli responsible for the entire family. Three of his nine children have passed away, leaving behind orphaned grandchildren.

Nephathli and his wife keep their cash in a safe place at home rather than in a bank. He also tries to save a little every month, mostly to pay for his grandchildren’s school fees. “I was not able to even open a bank account because of the little money that I get.” While Nephathli acknowledges that a bank would be a good place to borrow money from in order to buy a dairy cow or a tractor, he feels he does not qualify not having a bank account or the money for one.

Lesotho is characterised by a poor, but not indigent, population maintained largely through social support structures and remittances. While the adult population enjoys some access to banking services, these are by no means universally provided.

“It is increasingly recognised that it takes a broader ecosystem of providers to deliver the diverse set of financial services that the poor require as opposed to a singular focus on micro-finance institutions only.”

However, the kind of financial services that people use (including high-cost bank accounts, low-value community or home-based savings, high-cost informal loans, funeral cover, and informal remittances) are not helping to lift them out of poverty, but are merely offering ways to “get by.” Thus, financial access measured in terms of uptake is not the issue in Lesotho but rather how to extend the reach of these services. The bigger question is: How can financial services be leveraged or re-engineered to more effectively alleviate poverty and support economic growth?

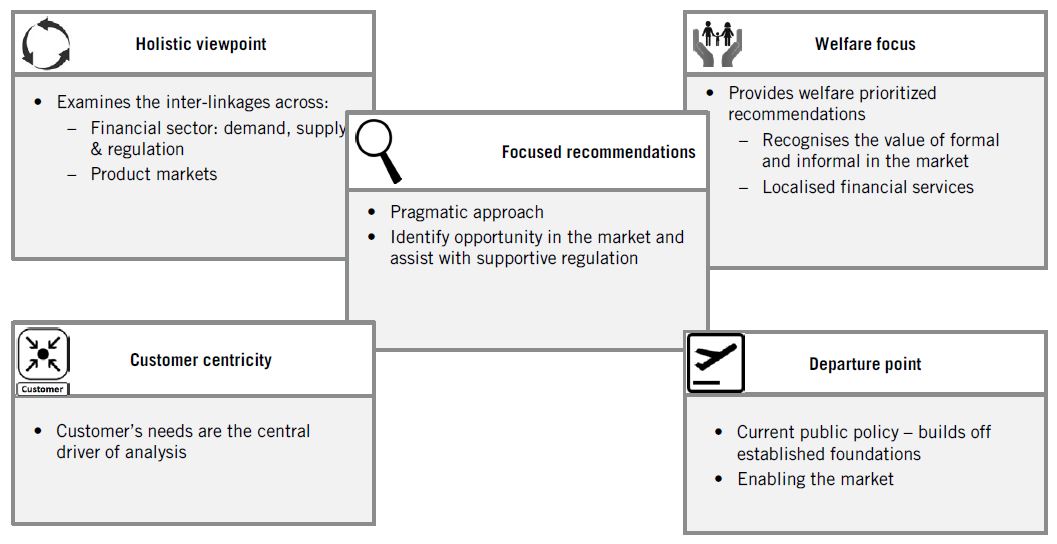

Making Access Possible

The recent MAP (Making Access Possible) diagnostic and planning framework in Lesotho was able to identify the financial inclusion priorities by unpacking and understanding the current customer needs and their usage of existing services. When filtering the financial inclusion priorities through the lens of actions most likely to contribute to poverty alleviation and economic growth, three key roadmap priorities were identified: Directly improve household welfare through efficiency gains and risk mitigation; take small steps towards enhanced growth via highly targeted productive credit and inward investment promotion; and increase financial sector intermediation to support investment and growth.

MAP is a UNCDF (United Nations Capital Development Fund) multi-country diagnostic and planning framework to support financial inclusion through a process of evidence-based country diagnostic and stakeholder dialogue, leading to the development of national financial inclusion roadmaps that identify key drivers of financial inclusion and recommended action.

MAP is a powerful tool towards the achievement of financial inclusion goals and aspirations across the globe. Through its inclusive approach and stakeholder engagement, and a comprehensive diagnostic, and practical, action-oriented strategies/roadmaps, MAP can enable governments and stakeholders to translate their high-level aspirations to reality. MAP generates key data that can be used in efforts to enhance decision-making and monitor progress as called for by the GPFI (Global Partnership for Financial inclusion).

Why MAP? MAP value proposition.

MAP is set apart from other financial inclusion initiatives in a number of ways. It combines three key components: A country diagnostic, a country-level stakeholder process and roadmap, and a global learning, dissemination, and advocacy drive to impact the financial inclusion agenda in a unique way. MAP is evidence based, customer centric and data driven, enabling factual and insightful discussions across a range of financial inclusion issues.

The MAP analytical framework and methodology amalgamates three tested approaches including UNCDF’s collaborative country-level programming framework (deployed in forty countries) that does not preconceive the role of different stakeholders but seeks to work within the practical realities to optimise and coordinate the efforts.

Broadening the Ecosystem

It is increasingly recognised that it takes a broader ecosystem of providers to deliver the diverse set of financial services that the poor require as opposed to a singular focus on micro-finance institutions only. Strategies that remain focused on only one of these providers such as microfinance institutions, private sector, cooperatives, or a single activity such as institution-building are missing the bigger picture and also unlikely to enable systemic change that will drive universal financial inclusion. This is based on the view that competitive markets are the means through which innovation and competition will result in falling transaction costs together with the scale and sustainability required to overcome the significant levels of exclusion that remain (Porteous, 2004, Honohan and Beck, 2007).

Financial transactions play an integral role in the daily lives of most people, especially those living in poverty. Yet, they are compelled to use informal, often sub-optimal services. Research has shown that poor households use a range of informal methods to manage their daily needs, including storing savings at home, with others, and with banking institutions; joining savings clubs, savings-and-loan clubs, and insurance clubs; and borrowing from neighbours, relatives, employers, moneylenders, or financial institutions. These mechanisms are not ideal, particularly in protecting the poor from short-term and long-term household risks and shocks.

Greater financial inclusion can contribute to multiple developmental priorities as laid out in the Post-2015 Development Agenda and the Sustainable Development Goals (SDGs) currently being negotiated at the United Nations. By reducing vulnerability to economic shocks and boosting job creation, financial inclusion can be a key driver of both poverty reduction and inclusive economic growth while at the same time promoting greater equality.

Increased financial inclusion for women has been shown to lead to their enhanced economic and social empowerment. Without inclusive financial systems, poor people must depend on incomplete or inferior informal mechanisms to deal with shocks. While building assets and small enterprises, they must rely on their limited earnings.

Greater Constraints

For firms, particularly small and start-up firms that are subject to greater constraints, access to finance can be associated with innovation, job creation, and growth. For these reasons, access to financial services can play a key role in the transformative Post-2015 Development Agenda across the three dimensions of sustainable development, economic, environmental and social. This explains why financial inclusion appears as targets under a number of likely SDGs being considered by the UN General Assembly.

Financial inclusion has also become a priority for policy-makers and regulators in financial sector development globally. Since 2009, the G20 has noted the importance of financial inclusion, particularly in its contribution to financial sector deepening, and has noted its contribution to economic growth. The G20 has gone further by setting out Nine Principles of Financial Inclusion and has underscored the importance of data with the adoption of the Basic Set of Financial Inclusion Indicators.

The MAP diagnostic and planning framework enables governments and other stakeholders to better understand the financial inclusion context in their country, by providing data and insights on demand for and supply of financial services as well as the policy, legal, and regulatory framework.

Reflecting the high priority placed by governments on financial inclusion, some 38 countries have made a commitment to expand financial inclusion as part of the Maya Declaration launched by the Alliance for Financial Inclusion (AFI). Many of these commitments include the adoption of national strategies for financial inclusion – and MAP can help in the development of these.

It is hoped that through the efforts of global programmes like AFI and the Maya Declaration, together with the powerful analysis and diagnostics provided by MAP, people like Nephathli can benefit from access to appropriate financial services. By understanding the needs and demands of households like Nephathli’s, policies as well as product and service solutions can be developed that better serve their needs and reduce inequalities of access. With greater access to a range of financial services, poor and low-income households and businesses can, increase consumption, manage risks, and expand income, and build assets.

About UNCDF

UNCDF is the UN’s capital investment agency for the world’s 48 least developed countries. It creates new opportunities for poor people and their small businesses by increasing access to microfinance and investment capital. UNCDF focuses on Africa and the poorest countries of Asia, with a special commitment to countries emerging from conflict or crisis. It provides seed capital – grants and loans – and technical support to help microfinance institutions reach more poor households and small businesses, and local governments finance the capital investments – water systems, feeder roads, schools, irrigation schemes – that will improve poor peoples’ lives. UNCDF programmes help to empower women, and are designed to catalyze larger capital flows from the private sector, national governments and development partners, for maximum impact toward the Millennium Development Goals. For more information, please visit www.uncdf.org and subscribe for news, follow @UNCDF on Twitter and UN Capital Development Fund on Facebook.

UNCDF is the UN’s capital investment agency for the world’s 48 least developed countries. It creates new opportunities for poor people and their small businesses by increasing access to microfinance and investment capital. UNCDF focuses on Africa and the poorest countries of Asia, with a special commitment to countries emerging from conflict or crisis. It provides seed capital – grants and loans – and technical support to help microfinance institutions reach more poor households and small businesses, and local governments finance the capital investments – water systems, feeder roads, schools, irrigation schemes – that will improve poor peoples’ lives. UNCDF programmes help to empower women, and are designed to catalyze larger capital flows from the private sector, national governments and development partners, for maximum impact toward the Millennium Development Goals. For more information, please visit www.uncdf.org and subscribe for news, follow @UNCDF on Twitter and UN Capital Development Fund on Facebook.

You may have an interest in also reading…

Navigating Complexity: How The Access Bank UK Limited Delivers Unmatched Trade Finance Solutions

In the rapidly evolving landscape of global trade, businesses face pressures that can disrupt even the most carefully planned transactions.

Cement Recycling: a Breakthrough for More Sustainable Construction

Reuse and recycle — it makes sense, even in the most basic steps of the building trade… The global construction

Tekcapital: Building Companies That Change Lives — And Create Value for Shareholders

Tekcapital has honed a differentiated model for discovering university inventions, turning them into real businesses, and listing them on major