Schafer Cullen: Why Discipline Still Defines Value Investing

In an equity market often driven by momentum, narrative and short-term positioning, Schafer Cullen continues to make the case for a more traditional discipline: buy good companies cheaply, insist on dividends, protect the balance sheet, and give time for value to emerge. The firm’s approach is rooted in classic value investing, but its relevance lies in how it applies that philosophy to modern portfolio construction, income generation and risk control.

Value investing is one of the most overused labels in asset management. In crowded markets, almost every manager claims some attachment to “value”, even when the underlying process owes more to relative pricing or cyclical timing than to genuine valuation discipline. Schafer Cullen takes a much narrower view. Its definition of value investing remains anchored in the framework Benjamin Graham recommended at the end of his career: focus on companies that are cheap on price-to-book, price-to-earnings and dividend measures, and then hold them for the long term. In Schafer Cullen’s interpretation, this is not nostalgia. It is still a rigorous filter for identifying businesses where valuation, income and staying power align.

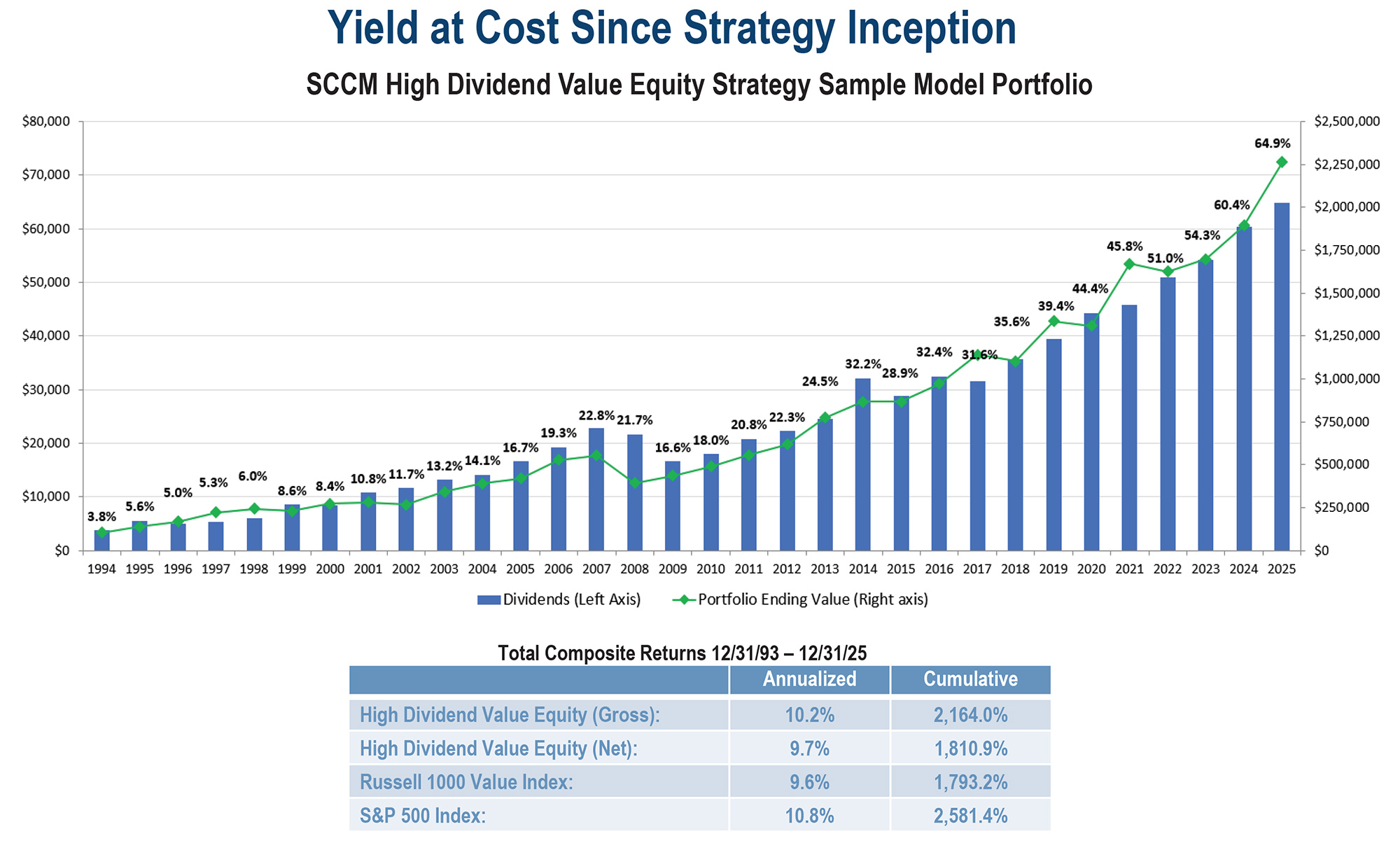

That emphasis on dividends is central. At Schafer Cullen, dividends are not treated simply as a source of income; they are viewed as a form of downside protection and a signal of corporate durability. The firm argues that dividend growth is especially important, though yield itself also matters. Its historical reference point is telling: over the past 60 years, there have been 12 recessions, and in each one dividends rose, even where earnings and share prices fell sharply. For the firm, that pattern explains why dividend-paying equities can help stabilise investor outcomes when markets turn hostile. Income is valuable in itself, but it also changes the behavioural and financial profile of an equity strategy by providing part of the return stream independently of market sentiment.

This becomes especially relevant in a concentrated portfolio. Schafer Cullen’s flagship strategies often hold only 30 to 45 names, which means each position must justify its place through a combination of valuation, quality and long-term potential. In that setting, the most important risk controls are not abstract factor models alone, but balance-sheet strength, close analysis of changes in consumer interest, and careful monitoring of management quality and business evolution. The firm is candid about the reality of concentrated investing: some holdings will periodically fall out of favour and appear to be value traps. Yet one of its core beliefs is that apparent weakness often creates future opportunity. After rigorous reanalysis, some of the most uncomfortable holdings can go on to become the strongest contributors over the following year or two. That does not mean every weak stock deserves patience. The firm acknowledges there are situations where the analysis proves wrong and where even a disciplined value process must accept error.

“At Schafer Cullen, dividends are not treated simply as a source of income; they are viewed as a form of downside protection and a signal of corporate durability.”

The difference lies in time horizon. Schafer Cullen does not frame value as a quick mean-reversion trade. When initiating a position, it is typically looking for a minimum holding period of three years, allowing time for research catalysts to unfold. In many cases, particularly where stocks remain attractive on a price-to-earnings basis, holdings may stay in the portfolio for as long as a decade. The kinds of catalysts the firm regards as most reliable are concrete rather than fashionable: better managers, new products, entry into new markets, or strategic shifts that can drive earnings growth and eventually support multiple expansion. This is a patient form of investing, but not a passive one. It is based on the idea that value is unlocked through business progress, not simply through the market changing its mind.

That patience also shapes how the firm thinks about downside protection. Rather than defining defensiveness through sector labels or low-beta positioning, Schafer Cullen argues that smoothness is best judged over a long enough measurement period. For that reason, it has settled on a five-year horizon as the most meaningful way to evaluate the consistency of an equity-income strategy. In the firm’s view, five years is long enough to smooth performance across recessionary shocks and short enough to remain relevant to client outcomes. It is a practical rather than theoretical definition of resilience: not the avoidance of all volatility, but the ability to navigate cycles without permanent damage to compounding.

The same philosophy extends into the firm’s enhanced equity income approach, where covered calls are written on a portion of holdings. Here again, the aim is not to manufacture yield indiscriminately, but to manage the trade-off between current income and future upside. Schafer Cullen says decisions about how much upside to sell, and on which holdings, are driven by both fundamental and technical research. That reflects a broader point about the strategy: options are not treated as a separate overlay detached from stock selection, but as another expression of the underlying research process. The decision to bring this approach into ETF form through the launch of DIVP in 2024 was, according to the firm, a response to client demand. Even so, the move also reflects a wider trend in the market: investors increasingly want transparent, liquid vehicles that combine income with equity exposure while preserving a disciplined framework for security selection.

Schafer Cullen’s value lens has never been confined to the United States. The firm notes that international stocks and ADRs often looked dramatically cheaper than US equities, particularly in earlier decades, and that these opportunities materially supported performance. Its historical examples range from Jaguar, bought as a British spin-off, to high-quality Chinese oil and gas companies and global consumer staples such as Unilever and Diageo, which benefited from growth in emerging markets. Today, the firm caps the international share of some portfolios because it also runs dedicated international and emerging-market strategies. Still, the logic remains consistent: valuation must be compelling enough to justify the additional layers of currency, governance and liquidity risk.

On research, Schafer Cullen adopts a measured view of AI. The firm sees the technology as a significant advance in data gathering, and its analysts are already using it to improve research efficiency. But it remains cautious about overstating what automation can do for security selection. In the firm’s view, a contrarian instinct is still vital in investing, and that quality is not easily systematised. AI may help gather information faster, but genuine stock-picking still depends on judgement, context and the willingness to lean against consensus when valuations and fundamentals justify it.

This preference for measured judgement also explains the firm’s stance on stewardship. Schafer Cullen engages with management teams where appropriate, but it does not define itself as an activist investor. Effective engagement, in this model, is less about public campaigns and more about ongoing dialogue, pressure where warranted, and a readiness to exit if the original investment case no longer holds. It is consistent with the broader ethos of the firm: disciplined, research-led, valuation-sensitive, and unwilling to confuse noise with genuine value creation.

At a time when equity markets often seem to reward speed over patience and narrative over balance-sheet substance, Schafer Cullen’s approach stands out for its refusal to overcomplicate the essential. Buy cheaply. Demand dividends. Focus on quality. Stay patient. And remember that in investing, as in business, the most durable outcomes are rarely the most fashionable in the moment.

Sponsored content — written to CFI.co editorial standards

You may have an interest in also reading…

Is the MBA Still Worth It? Weighing Value, ROI, and Leadership Impact

In an era of rapid disruption, does the traditional MBA still hold its weight? We explore the enduring value of

Built on Trust, Powered by Client Commitment: The XMTrading Standard

In the world of trading, trust is the ultimate currency, and transparency is the gold standard. XMTrading, a broker that

The Economics of Christmas

Unwrapping the Global Trends in Online and High Street Shopping During the Festive Season The Christmas season has long been