Corporate Knights Capital: Sustainability Reporting – Empowering Responsible Investing for Long-Term Prosperity

Toronto

Last September, the Rockefeller Brothers Fund announced its pledge to divest its fossil fuel holdings as part of a larger divestment movement that aims to derive the industry of up to $50bn. Later that month, the Montreal Carbon Pledge was launched where investors commit to measure and publicly disclose the carbon footprint of their investment portfolios on an annual basis. To date, investors representing assets under management of $1.2 trillion have committed to the pledge.

Add to the above the fact that there is currently about US$45 trillion of assets under management by 1,314 United Nations Principles for Responsible Investment (UNPRI) signatories – up from only $4 trillion back in 2006. UNPRI signatories commit to integrate six principles covering environmental, social, and governance issues into their investment decision making and ownership practices.

Clearly, responsible investing is growing in importance – not only because it is good for our planet’s long-term prosperity but also because there is mounting evidence that it can lead to superior investment returns. For instance, by subjecting equities from the high-carbon sectors in a given index to a performance test, related to normalised greenhouse gas emissions, and removing the ones with a below-average performance relative to sector peers, it is possible to obtain a portfolio of securities with a lower carbon footprint while achieving superior total returns compared to the original index.

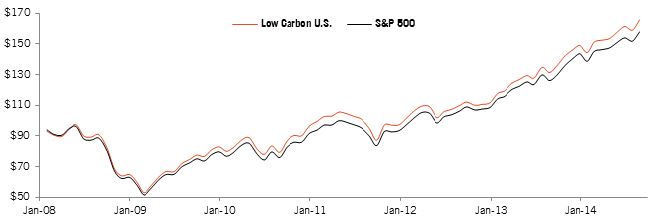

The Low Carbon US

In the simulated case below, the “Low Carbon US” achieves a 56.7% reduction in normalised greenhouse gas emissions with the bonus of an extra 7.8% in total returns compared to the original index over the time period January 1, 2008 to August 31, 2014.

“The increased investor appetite for responsible investing has been made possible in part by the remarkable rise in the availability of sustainability data.”

The increased investor appetite for responsible investing has been made possible in part by the remarkable rise in the availability of sustainability data. Over the past decade, the number of corporate sustainability reports – the most common format for corporations to disclose their periodic environmental, social, and governance performance – has grown to 7,445 in 2013, from a mere 644 in 1999. A combination of heightened investor demand, activism, and mostly regulatory intervention, coupled with a move towards greater transparency initiated by leading corporations, have all combined to drive increased sustainability disclosures.

Figure 1: Historical Performance of the Low Carbon U.S. vs. S&P 500 (January 2008 – August 2014).

For instance, on October 17, 2014, the Singapore Stock Exchange announced its intention to adopt a comply-or-explain mechanism for sustainability reporting for all its listed companies. When implemented, this piece of regulation will add to the inventory of close to 170 policies in force around the world that are meant to encourage or mandate corporate sustainability reporting.

More, Not Better

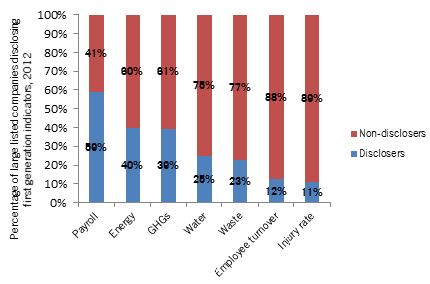

While the number of sustainability reports has increased substantially, a closer look reveals some important findings. In its latest analysis of sustainability disclosure trends among the world’s stock exchanges, Corporate Knights Capital found that a sizable chunk the world’s large listed companies are failing to disclose their performance on the seven basic sustainability metrics – employee turnover, energy, greenhouse gas emissions (GHGs), injury rate, payroll (total employee compensation), waste, and water. These seven basic indicators are objective measures of corporate sustainability performance that are broadly relevant for companies in all industries. Moreover, they are generally accepted as being the most widely tracked core sustainability metrics by various stakeholder groups including investors.

For instance, only 39% of the world’s 4,609 large listed companies disclosed their GHGs for the year 2012. For water, that percentage is 25%. As for employee turnover rate, it is a paltry 12%. While disclosure rates vary by sector, it means that a majority of the world’s large companies are still not disclosing these seven basic sustainability metrics – in the case of GHGs, arguably the most universally recognised strategic sustainability issue, it has not been reported by 61% of the world’s large listed companies. Even more disconcerting is the finding that only 128 (2.8%) of the all the world’s large listed companies disclosed all the seven basic sustainability metrics for the year 2012.

Figure 2: Sustainability Metrics Reporting by Large Listed Companies, 2012.

Essentially, the remarkable rise in the number of sustainability reports has not been accompanied by a similar increase in the reporting of the basic sustainability metrics.

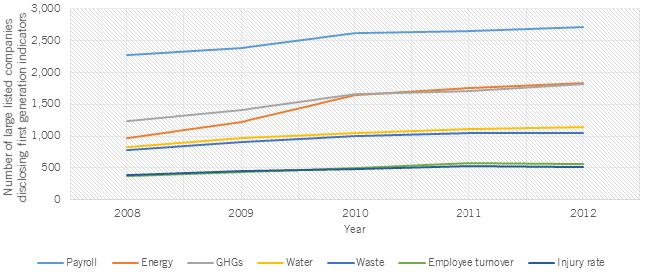

Equally troubling is that disclosure rates on the seven basic sustainability indicators appear to be plateauing. As one illustration, the number of large listed companies that disclosed their energy use increased by 88% from 2008 to 2012 but only by 5% from 2011 to 2012. A similar reporting slowdown is occurring on the other six metrics.

Clearly, a majority of companies are still not transparent enough to allow investors to make well-informed investment decisions over the long-term horizon by integrating foundational sustainability criteria. A point has been reached where virtually all of the large companies which would have engaged in the reporting of the basic sustainability metrics have done so already and the remaining large companies likely have little or no intention of doing so under present circumstances.

Investors Demand Data

This is in stark contrast to investors’ growing interest in building sustainable investment strategies. Despite the notable progress made in corporate sustainability reporting, as is shown above, there is still much room for improvement – not only in terms of quantity but also in terms of consistency and timeliness. While virtually every company has reported on their financial performance six months after their year-end, only 63% of these companies have disclosed their sustainability performance by then.

It is therefore not a surprise that In October 2014, the United Nations Principles for Responsible Investment (UNPRI) and Ceres’ Investor Network on Climate Risk (INCR) launched an initiative to convey investors’ demands for more timely, comparable, and material disclosure of corporate sustainability information to the International Organization of Securities Commissions (IOSCO) in order to inform their investment decisions.

Figure 3: Basic Sustainability Metrics Reporting by Large Listed Companies, 2008 – 2012.

The IOSCO stands in a critical position in this regard through its direct relationship with member stock exchange regulators. Investors of all description are encouraged to demand swift and decisive action from the IOSCO to provide greater clarity around sustainability reporting requirements, ideally to be integrated as part of existing financial disclosures.

The necessary tools are already available. For instance, IOSCO can take inspiration from UNCTAD’s Best Practice Guidance for Policymakers and Stock Exchanges on Sustainability Reporting Initiatives to facilitate a consistent implementation of corporate sustainability reporting requirement among member exchanges. This guidance is a voluntary technical aid to assist stock exchanges and regulators who have responsibility for corporate reporting practice and are contemplating the introduction of a new initiative – or further development of an existing one – to promote corporate sustainability reporting.

Johannesburg Model

The relative success of the Johannesburg Stock Exchange in spurring sustainability disclosure amongst listed companies through the implementation of the listing requirement incorporating the King III Code of Corporate Governance stands as a benchmark for aspiring investors and stock exchanges around the world. Ceres’ Investor Listing Standards Proposal, Recommendations for Stock Exchange Requirements on Corporate Sustainability Reporting, which engages global stock exchanges via the World Federation of Exchanges (WFE) on a possible uniform reporting standard for sustainability reporting by WFE members may also serve as a basis for the implementation of corporate sustainability reporting requirements among member exchanges.

Likewise, governments stand in a pivotal position to influence corporate sustainability reporting and are encouraged to renew their efforts in this direction. Existing policies around the world vary in many respects in terms of whether they are mandatory or voluntary, broad or narrow (i.e. applies to various industries as opposed to only one or few specific industries), and prescriptive or principles-based (i.e. states which specific items of sustainability performance metrics are to be reported and how).

These wide differences in the type of policies may in part explain the differences in disclosure performance by the large listed companies of the seven basic sustainability metrics among the world’s stock exchanges as shown in Corporate Knights Capital’s latest report on corporate sustainability disclosure trends. However, it was found that there is a strong association between policies that are mandatory, broad, and prescriptive and better corporate sustainability disclosure performance. Policy-makers may use this finding as a framework to identify case studies and benchmarks for implementation in their own jurisdictions.

Disclosure Frameworks

The advent of non-governmental standard-setters such as the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board (SASB), and voluntary disclosure frameworks such as the CDP and the Climate Change Reporting Framework, have without any doubt helped to popularise sustainability reporting. However, there exists a proliferation of fragmented and often competing reporting standards and frameworks when it comes to sustainability reporting which may bring confusion to both the reporters and the users.

A rapid and successful conclusion of the work among the participants to the Corporate Reporting Dialogue will bring about much needed clarity and comparability in corporate sustainability reporting which will encourage more corporations to embrace more coherent and useful disclosures of sustainability performance. The Corporate Reporting Dialogue brings together financial reporting standard-setters and sustainability reporting frameworks to promote greater alignment, consistency, and comparability between corporate reporting requirements, standards, and frameworks. An endorsement by the major groups of users of corporate disclosures – both financial and non-financial – of the outcome of the work of the Corporate Reporting Dialogue will also help in determining the de facto global standard in corporate reporting.

The explosion in corporate sustainability reporting over the last ten years or so has certainly helped to fuel the remarkable rise in responsible investing. Responsible investing is a much heralded practice whereby investment decisions consider long-term economic, social, and environmental sustainability. However, current corporate sustainability reporting practices are at odds with the needs and level of interest from investors such that a renewed effort is needed to bring sustainability reporting to the next level. Governments, regulators both private and public, business and non-business organizations, and investors all have an important role to play to make this happen. i

About the Authors

Doug Morrow has eight years of experience in the equity research and consulting industries, with a focus on environmental, social and governance (ESG) investment research and product development. He is currently Associate Director of Thematic Research at Sustainalytics. Prior to joining Sustainalytics he worked for three years at Corporate Knights Capital, where he helped launch the world’s first suite of sustainable smart beta indices, and at ICF International (ICF) where he consulted for the Inter-American Development Bank, The Blackstone Group and the International Finance Corporation. Doug also worked for three years at Innovest, where he helped develop one of the world’s first carbon tilted corporate bond indexes (in partnership with JP Morgan Chase) and long/short equity products (with UBS). Doug is a member of the United Nation’s International Standards of Accounting and Reporting (ISAR) Group of Experts on Sustainability Reporting and the Association of Chartered Certified Accountants (ACCA) Global Forum for Sustainability. His work has been cited in the Financial Times, New York Times, Business Week, Environmental Finance and The Globe and Mail.

Doug Morrow has eight years of experience in the equity research and consulting industries, with a focus on environmental, social and governance (ESG) investment research and product development. He is currently Associate Director of Thematic Research at Sustainalytics. Prior to joining Sustainalytics he worked for three years at Corporate Knights Capital, where he helped launch the world’s first suite of sustainable smart beta indices, and at ICF International (ICF) where he consulted for the Inter-American Development Bank, The Blackstone Group and the International Finance Corporation. Doug also worked for three years at Innovest, where he helped develop one of the world’s first carbon tilted corporate bond indexes (in partnership with JP Morgan Chase) and long/short equity products (with UBS). Doug is a member of the United Nation’s International Standards of Accounting and Reporting (ISAR) Group of Experts on Sustainability Reporting and the Association of Chartered Certified Accountants (ACCA) Global Forum for Sustainability. His work has been cited in the Financial Times, New York Times, Business Week, Environmental Finance and The Globe and Mail.

Michael Yow is the lead analyst at Corporate Knights Capital. Michael works with clients to analyze and benchmark their sustainability performance and disclosure practices so that they become industry leaders. He leads the corporate sustainability assessment function, including the annual Global 100 Most Sustainable Corporations in the World ranking. He is in charge of research on various sustainability topics and is the co-author of an annual report assessing corporate sustainability disclosures among the world’s stock exchanges. Michael is also involved in academic research work at York University. Before joining Corporate Knights Capital in 2011, Michael worked as a consultant in international financial and fiduciary services. Michael holds a Master in Business Administration from the Schulich School of Business, York University.

Michael Yow is the lead analyst at Corporate Knights Capital. Michael works with clients to analyze and benchmark their sustainability performance and disclosure practices so that they become industry leaders. He leads the corporate sustainability assessment function, including the annual Global 100 Most Sustainable Corporations in the World ranking. He is in charge of research on various sustainability topics and is the co-author of an annual report assessing corporate sustainability disclosures among the world’s stock exchanges. Michael is also involved in academic research work at York University. Before joining Corporate Knights Capital in 2011, Michael worked as a consultant in international financial and fiduciary services. Michael holds a Master in Business Administration from the Schulich School of Business, York University.

About Corporate Knights Capital

Corporate Knights Capital is an investment advisory and research firm based in Toronto, Canada, with over a decade of experience quantifying corporate sustainability. Corporate Knights Capital’s parent, Corporate Knights, Inc., publishes the world’s largest circulating responsible business magazine, and serves as the secretariat for the Council for Clean Capitalism. It is a global leader in building investment strategies that integrate high quality corporate sustainability data. Corporate Knights Capital is a certified B Corporation and a proud signatory of the United Nations Principles for Responsible Investment. Its mission is to accelerate the transition to long term, sustainable capitalism by building world-class investment portfolios for the global investment community.

You may have an interest in also reading…

Belarusian Entrepreneur Denis Primakov Is Developing an Efficient System for Transporting Perishable Products

Despite the fact that the transportation of goods by car in the United States has always been and still is

Middle-Market Direct Lending

A Lucrative Alternative Asset Class The US is home to some 200,000 companies dubbed “middle-market” — typically with EBITDA up

UNCTAD: A Policy Compact to Get Investment Flowing Again

James Zhan suggests world leaders make a joint effort to formulate effective investment policies to help build investment firepower to