Roche: New Solutions to Old Problems? Fintech Can Change Healthcare

Author: Pablo Morales

Fintech is a term applied to technology-driven disruptions such as mobile money, blockchain, and big data analytics in payment, banking, or insurance services.

Given its digital nature, Fintech has made financial services more inclusive, accessible, and affordable by reaching millions of previously underserved populations such as the unbanked, rural, or informal sectors. This same potential in connectivity, efficiency gains, and expansive thinking can be realised in the healthcare space to transform the ways health services are financed.

Healthcare financing is a complex and evolving space with implications for economic development and individual wellbeing. Many nations firmly believe in the importance of transforming their health financing systems to attain strategic objectives such as Universal Health Care in the mid-term and have taken serious steps towards this transformational goal. But the overall results of these efforts are not quite yet as expected.

The necessary expansion of services has resulted in increases in out-of-pocket expenditure at a high cost to individuals and their families. Policymakers in every health system are faced with challenges in key areas of raising revenues, pooling resources, and conducting strategic purchasing of goods and services. Establishing a predictable and sustainable flow of funds while ensuring that the financial burden is fairly shared across society has proven no easy task.

Changing this situation requires we all take a different approach and leverage innovative ways to overcome the structural barriers preventing access to healthcare. In this respect, compared to the previous decade, the digitalisation of financial transactions and the spread of mobile phones have created a way to overcome the hurdles in healthcare financing.

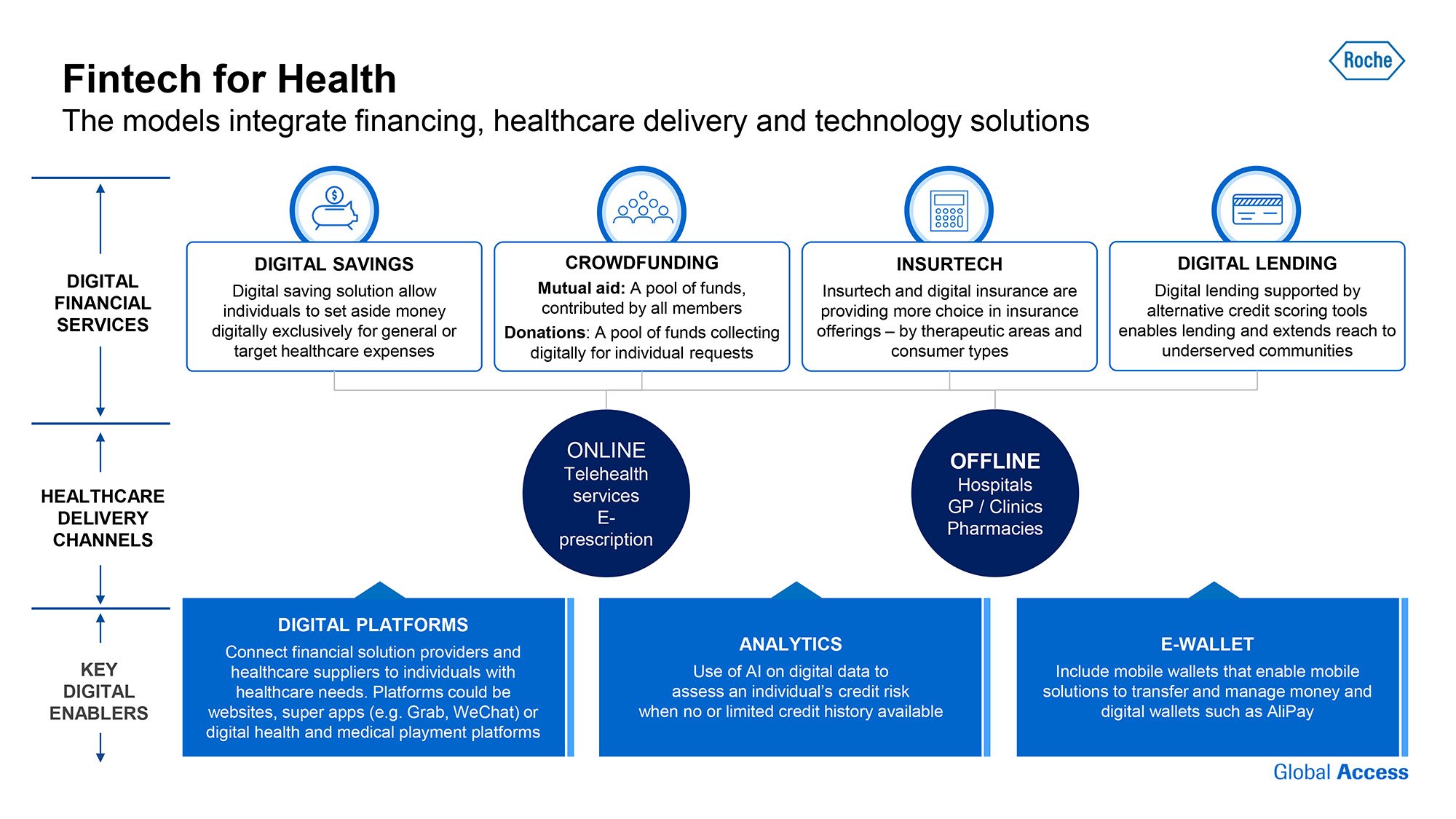

Source: ACCESS Health International

Mobile money platforms have grown in recent years, particularly in emerging markets, where base-of-the pyramid populations often lack access to basic health services but possess mobile phones. Over two billion people use at least one available mobile money service and there are currently over 900 planned or deployed mobile health products and services. Over the next few years, the global market for these solutions is expected to exceed $30bn, as stakeholders look to reduce costs, add value, and enhance the reach of health services.

The unprecedented connectedness of today’s society, together with an expanding data-processing capacity, is creating opportunities for new health financing models in response to funding gaps in current systems. These models are disrupting pre-established structures and reshaping all aspects of financial services.

One clear example can be seen in China, with Ant Financial’s mutual aid health insurance platform, Xiang Hu Bao. In less than a year since its launch in October 2018, the platform attracted over 100 million people and aimed to reach another 300 million over the next couple of years.

Xiang Hu Bao, which literally means “mutual protection”, provides its participants with a basic health plan against 100 types of critical illness, including thyroid cancer, breast cancer, lung cancer, critical brain injury, and acute myocardial infarction. Without the need for upfront payments or premiums, all participants share health risks, and the related medical expenses. It is not a health insurance product, but complements the health insurance offering in the market.

In countries with high out-of-pocket (OOP) expenditure, the lack of financial protection forces people to go without treatment — or experience catastrophic expenditure seeking care. This has opened a space for digital saving and lending platforms that can fill this space while national health systems have not yet matured. Two interesting examples are M-TIBA and Arogya Finance.

M-TIBA facilitates mobile money transfers between funders, patients, and healthcare providers. The platform directs funds from public and private funders directly to patients into a digital “health wallet” payment app for health services in M-TIBA-approved clinics, for public and private insurance premiums. For the case of Arogya, this social healthcare venture offers loans to cover healthcare needs to the traditionally unbankable, using innovative risk-assessment tools.

A Financial Journey

These initiatives share important similarities. In all cases, fintech applications borrowed from other dimensions of financial services have been redirected to healthcare services. More importantly, all of these have the potential for scalability and transferability to other countries.

These and other evolving developments across savings, lending, and payments platforms have the potential to transform healthcare across the world, by revolutionising and scaling health funding and financing mechanisms for public and private payers. In the short- and mid-term, fintech can bring substantial impacts in the healthcare space.

- Expanding the health financing base. Connectivity among digital users strengthens health system resource pooling capabilities enabling risk transferrals among groups.

- Increasing financial protection. Inclusive digital finance mechanisms can help reduce individual OOP throughout the patient financial journey.

- Supporting data-driven environments. Meaningful data generation will continue to tailor health products and services to patient needs and monitor for improvements.

- Fostering innovation in healthcare. Opens opportunity for multiple stakeholder collaboration and increased investment channeled towards the healthcare space.

Going forward, as new fintech models are developed and capabilities continue to expand, so will the practical applications of these innovations. Systems continue to integrate, allowing for quicker and more efficient decisions. This opens new avenues for public, private, NGOs and development organizations to explore ideas, pilot solutions, and share their learnings. This enables the collective intelligence required to finally leave old problems behind.

Where Roche is Going

Roche’s global track record of healthcare funding work, understanding of medical needs for the treatment of NCDs, global footprint, and expanding network puts the firm in a position to contribute to the development, co-creation, and delivery of meaningful funding and financing solutions to expand access to healthcare.

It sees fintech developments as key drivers for innovation and as strong contributors, to build the next-gen infrastructure to satisfy future global healthcare needs.

The company engages with a broad range of multisectoral stakeholders to foster a global fintech for health network that will:

- Drive connection and co-creation between Roche and Fintech players (banks, telecommunications, insurtechs, data start-ups)

- Foster a strong and dynamic fintech for the health ecosystem

- Accelerate the design and implementation of fintech models and solutions that positively impact patient access to healthcare

- Leverage fintech developments to support the advancement of Universal Health Care.

Roche is partnering with fintechs, healthcare providers, and civil society to launch promising digital mutual aid schemes and crowdfunding platforms as well as explore insurtech models that can address financial shortfalls.

Findings from these initiatives will reinforce future developments as Roche continues to pilot and learn while creating access to innovation for patients.

About the Author

Pablo Ignacio Morales is a Health Systems Strategy Leader at Roche’s Global Access organization. In his role, Pablo collaborates with public and private stakeholders to support the development of innovative and sustainable models to finance access to healthcare. He is currently exploring the potential of financial technology to strengthen health system funding in low and middle-income countries. His educational background is in Industrial Engineering and holds a Masters in Health Economics from the University of Queensland, Australia. Before joining Roche, he built a career as a Strategic Management consultant working for top consulting firms as E&Y and PwC. Additionally, as a consultant for the Inter-American Development Bank he led the design of national health policy changes in Costa Rica. Pablo Morales is currently a full-time resident in Basel, Switzerland.

You may have an interest in also reading…

Committed to the Future, Driven by Passion, Dedicated to Clients, and Steadfast on Sustainability

Swiss asset management firm keeps a tight focus on its core values, customer needs, and the drive for responsible investment

Recycling Plastic: Is it Working, and are we Doing Enough…?

Once seen as a ‘wonder material’, this by-product of the oil industry has become a global environmental menace. Millions of

Scottish Institution Leads with Gusto, by Example

Colleague-friendly, compassionate, and with wholesome social goals in mind, Scottish Friendly is going strong… Scottish Friendly is an institution dedicated