Sanctions Against Russia Resemble a Boxing Match

The economic sanctions against Russia announced last week by the US and Europe are having a profound impact on the Russian economy — and repercussions at home. As in a boxing match, the expectation is that blows to the opponent can knock them out, despite exposure on the puncher’s side.

The US has applied several sectoral and economic sanctions against Russia since the annexation of Crimea in 2014, and during military clashes in eastern Ukraine. Nothing has been comparable, however, to what was announced last week.

Between February 22 and 27, there were sanctions by the United States on the secondary market for Russian sovereign debt securities issued after March 1, and a German decision to suspend certification of the Nord Stream 2 pipeline. There have since been announcements — by the US, the 27 members of the European Union and the G7 countries — of the freezing of assets of Russian banks and some individuals, and controls on the export of technology products. This culminated with the removal of some Russian banks from the SWIFT system and the banning of transactions with the Central Bank of Russia.

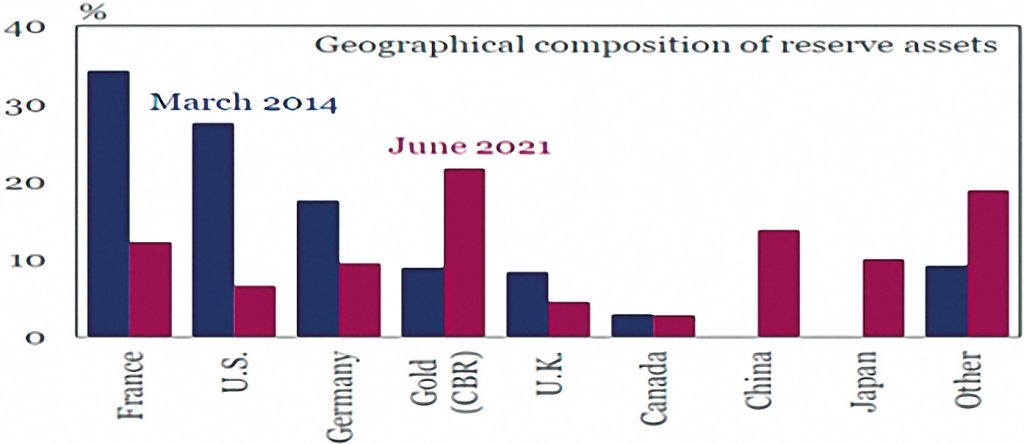

Figure 1: Bank of Russia – assets have been moved away from US and EU. Source: Bank of Russia, IIF.

SWIFT is a messaging network connecting banks worldwide that is considered a backbone of international finance. SWIFT is a consortium managed by employees of member banks, which include the central banks of the US, Europe, Belgium, England, and Japan. Based in Belgium, the consortium links more than 11,000 financial institutions in 200 countries and territories, enabling international payments. In 2021, the system recorded an average of 42 million messages each day, including payment requests and confirmations, negotiations, and currency exchanges. About one percent of these are believed to have involved Russian payments.

Would there be any alternatives for Russians to transfer and normalise their operations outside of SWIFT? Russia has an one, the System for Transfer of Financial Messages, but it cannot be a replacement. By the end of 2020, the system included only 400 participants from 23 countries. Also, China’s cross-border interbank payment system could not be a perfect replacement, at least not any time soon, as it does not incorporate SWIFT members.

Last week’s sanctions are already having a significant impact on the Russian financial system and its economy. The value of the rouble collapsed. The Central Bank of Russia put interest rates up, to limit the transmission of currency devaluation to inflation. Restrictive capital controls, and possibly bank holidays, lie ahead.

Despite the strategy of reducing exposure since the beginning of sanctions in 2014, via geographic relocation of reserves and acquisition of gold, and changing currencies in commercial transactions — a kind of “de-dollarisation” — Russia has not become invulnerable and the impact will be great (Figure 1). The GDP contraction will not be light, given the tightening of financial conditions accompanying ultra-high interest rates and banks without access to foreign currency.

And outside Russia? Of course, the receiving end of payments — creditors, asset investors — will be impacted. The consequences will only be extended if the devaluation of the corresponding assets leads to some contagion effect: withdrawal of funds by investors in mutual funds forcing their managers to liquidate other assets in their portfolios to pay for the withdrawals.

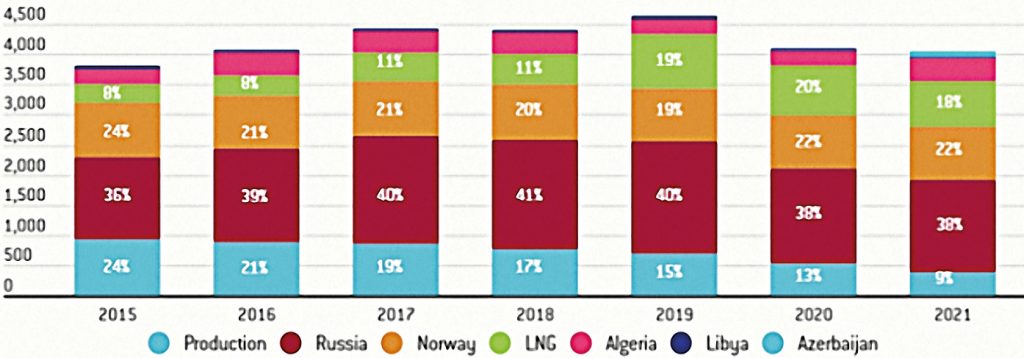

Figure 2: Annual EU27 natural gas domestic production and imports (TWh). Source: Bruegel

The sanctions were tentatively designed to minimise their effect on Russian gas imports to Europe. The sanctions are more limited in scope than the broader targeting advocated by other countries to win Germany’s support.

It will be through the rise in energy commodity prices — in addition to possible restrictions on the transport of Russian products — that the war in Ukraine will affect the economies on the other side of the fight. Also, because of a statistically proven asymmetry: what happens in the subgroup of energy commodities affects others, such as food and metals.

On top of that, the global supply of wheat will be negatively impacted, which is particularly important in regions such as North Africa and the Middle East. Russia is also a major supplier of fertilizers, palladium, and other products which may be affected by supply chain restrictions.

The inflationary shock coming from that, and higher commodity prices, will accentuate the dilemma faced by central banks on both sides of the Atlantic. How quickly and intensively can financial conditions be tightened in the face of inflation, while not bringing down the pace of economic activity? The deteriorating macro-economic outlook prompts analysts to predict that the Federal Reserve will opt for 25 basis points.

There is a fear that these economies would return to conditions like those of the early 1980s, when the second oil shock occurred while inflation was already high. The bet is that Jerome Powell and his colleagues at the Fed are not like Paul Volcker, chairman of the Federal Reserve at the time, whose option was to bring down inflation at any cost.

Returning to sanctions: of course, additional rounds extending the reach can still be adopted in new rounds of the boxing match. The Bruegel Institute, a Brussels-based think-tank, tackles scenarios such as how Europe would suffer from a halt in the flow of Russian gas (Figure 2).

The boxing match via financial and commercial sanctions has just begun. The willingness to seek Russia’s knockout in this way seems more robust than the fear of its consequences.

By Otaviano Canuto. First appeared in Policy Center for the New South.

You may have an interest in also reading…

Commissioner Gentiloni on EU Economy: Andante Ma Non Troppo

The V-shaped economic recovery expected to unfold next year is merely an illusion sourced from wishful thinking. Yesterday, EU Commissioner

Boost R&D to Ensure Sustainable Post-Covid Recovery: Economists

Increased investment in research and development is crucial to post-covid recovery, say economists calling for lasting improvements in the field.

Global Warning: Asia is Critical to Addressing Climate Change

Asia emits about half of the world’s global greenhouse gas emissions and that figure is set to increase if the