The Perfect Storm in Energy Infrastructure: High-Density Hydro, Cost Deflation, and Geopolitical Security

The hypothesis is clear. The energy transition has moved from a climate-led investment cycle to a security-led industrial buildout, and the binding constraint is no longer generation cost alone. As grids strain under intermittent supply and geopolitics reprices fuel risk, long-duration flexibility becomes the scarce asset. For institutional capital, that bottleneck is where infrastructure alpha is most likely to be found.

The Drivers of LDES Alpha

The global economy is entering one of the most capital-intensive industrial transitions in modern history, shaped by two forces that now reinforce one another: technological cost deflation and the strategic imperative for national energy independence. The International Energy Agency’s World Energy Outlook 2025 is explicit that energy security has become a question of economic and national security, with vulnerabilities exposed across fuel supply chains and legacy grid infrastructure.

The first phase of the transition was driven largely by climate mandates. Increasingly, it is underwritten by structural cost advantage. By late 2025, the cost curve in renewable generation and storage had tightened to the point that it began to squeeze the pricing power of legacy coal and gas plant, a dynamic explored in The Cost Curve That Is Squeezing Coal and Gas.

A second catalyst has now hardened the investment case: geopolitics. When energy independence becomes a first-order political priority, it pulls capital towards domestic, fuel-free electricity systems and away from import-dependent risk. This logic sits behind the shift examined in Energy Security and Capital Allocation.

Multilateral institutions are mobilising around this reality. The International Renewable Energy Agency’s Renewable Capacity Statistics 2026 notes that global capacity is rising fast, but disparities across regions create acute economic vulnerability, reinforcing the need to scale domestic capacity. The European Bank for Reconstruction and Development’s Green Economy Transition Strategy 2026–30 targets €150bn in cumulative green financing to build resilience against rising geopolitical and climate risks across emerging markets.

Why the Grid Has Become the Bottleneck

As large volumes of offshore wind and solar are injected into grid architectures built for centralised thermal generation, infrastructure constraints are emerging as decisive. Recent analysis framed by the World Bank’s energy work underlines the shift: integration, congestion, interconnection delays, and balancing requirements can now shape delivered electricity prices and reliability as much as the raw cost of generation.

For infrastructure funds and sovereign portfolios, this is the investable tension at the heart of the transition. Grid bottlenecks create volatility, curtailment, and security risk, but they also create the conditions for outsized, risk-adjusted returns where scalable, localised flexibility can be deployed at speed. This is the practical meaning of “LDES alpha”: capturing premium economics by resolving system frictions rather than simply adding more intermittent capacity.

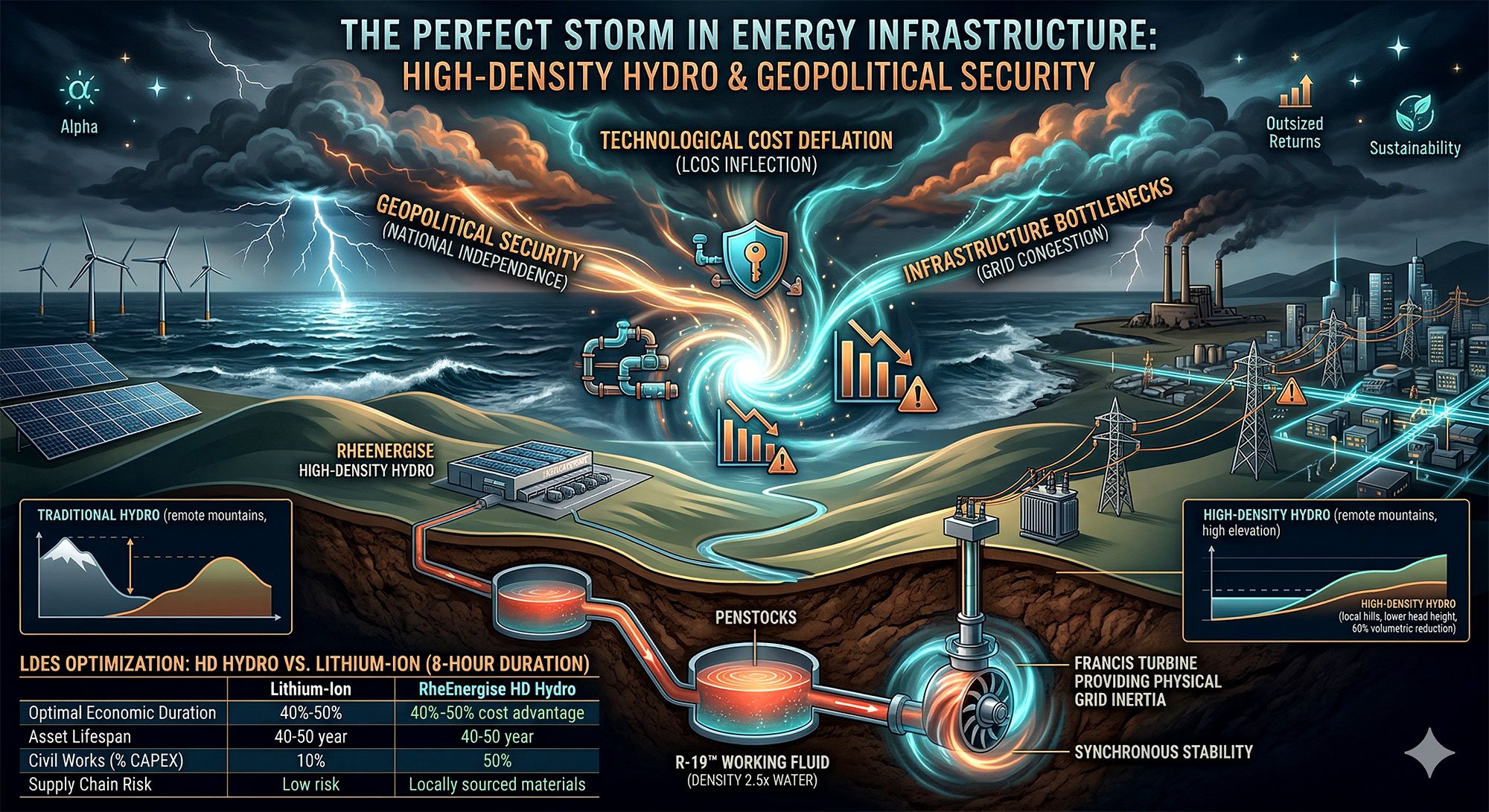

High-Density Hydro and the R-19 Breakthrough

Lithium-ion has dominated short-duration energy storage, but long-duration energy storage, typically defined as eight to 20 hours of dispatchable output, is a different economic problem. The limits are well known: 10- to 12-year lifespans, degradation, and supply-chain exposure to critical minerals and tariffs, which can make grid-scale bulk shifting expensive and geopolitically vulnerable.

A new approach is emerging to meet this requirement: High-Density Hydro, developed by UK-based innovator RheEnergise. Following a reported operational milestone in January 2026, the technology is being positioned as a bankable infrastructure asset class aimed at low-cost, domestically secure energy storage, detailed in the company’s Cornwood commissioning announcement.

The Physics of R-19: Re-Engineering Gravitational Potential Energy

Traditional pumped hydro storage is built on gravitational potential energy. In simple terms, energy stored depends on mass, gravity, and vertical elevation, commonly expressed as E = mgh. Because water density is fixed, conventional pumped hydro requires substantial head height, which limits viable sites and often pushes projects into remote and environmentally sensitive terrain.

RheEnergise changes the equation by substituting water with a proprietary working fluid, R-19, described as an environmentally benign mineral powder suspension with a density about 2.5 times greater than water. In practical terms, increasing the mass term by a factor of 2.5 reduces the head height required for the same power output by the same factor, a mechanism explained in Energy Systems Catapult’s analysis of high-density pumped hydro.

The system is engineered for low viscosity behaviour, with larger-bore pipes designed to counter drag effects and maintain round-trip efficiency of about 80 percent, also discussed by Energy Systems Catapult. By reducing head height requirements, High-Density Hydro can operate on smaller, gentler hills. The overall system is described as about 60 percent smaller volumetrically than comparable water-based installations, with tanks and penstocks buried underground to reduce footprint and planning friction.

Scale-up is always the credibility test for deep-tech infrastructure. RheEnergise has addressed manufacturing repeatability by partnering with Cambridge-based engineering consultancy 42 Technology, which has described its work on a semi-automated on-site processing plant in its Cornwood project note. The design intent is straightforward: as project pipelines scale, production of the core fluid remains replicable, local, and operationally reliable.

The Economics of LDES: HD Hydro Versus Lithium-Ion

For allocators, long-duration storage is judged by levelised cost of storage and by upfront capital expenditure. A key distinction is scaling behaviour. Lithium-ion is modular chemistry: extending duration from four hours to 12 hours requires the linear addition of cells. High-Density Hydro scales duration mainly through larger tanks and more fluid while keeping expensive turbomachinery broadly unchanged, which pushes down marginal cost per unit of stored energy as duration rises.

Conventional pumped hydro is often dominated by civil works, with tunnels, dams and large-scale ground engineering frequently accounting for 65 to 70 percent of total capital cost. High-Density Hydro is positioned as materially smaller, with civil works estimated at about 12 to 20 percent of total cost, which is cited alongside other cost comparisons in the context of long-duration storage competition and levelised economics, including BloombergNEF’s assessment that novel technologies are closing in on lithium-ion on longer durations in Lithium-Ion Batteries Are Set to Face Competition From Novel Tech for Long-Duration Storage.

On this basis, RheEnergise estimates High-Density Hydro could be 40 to 50 percent cheaper than lithium-ion for an eight-hour application. The wider analytical ecosystem cited by the project includes the Roland Berger LDES Council work and academic analysis by Schmidt and Staffell (Oxford University Press), with early-stage investor material also available via Republic.

Core Financial and Technical Parameters

| Parameter | Lithium-Ion Battery Arrays | RheEnergise High-Density Hydro |

|---|---|---|

| Optimal Economic Duration | One to four hours | Four to 20-plus hours |

| Asset Technical Lifespan | 10 to 12 years | 40 to 50-plus years |

| Round-Trip Efficiency | 85 to 90 percent | About 80 percent |

| Civil Works as Share of Total CAPEX | Minimal | Reduced to about 12 to 20 percent |

| Geopolitical Supply-Chain Risk | High (critical minerals, tariffs) | Low (locally sourced civil works and fluid production) |

Beyond direct cost metrics, High-Density Hydro is positioned as a domestic value-retention play. With local civil works and local fluid production, the company argues that more than 80 percent of project capital value can remain within the local economy, aligning with the geopolitical pivot towards energy security and industrial resilience.

The Inertia Advantage: Stability as a Revenue Stream

Energy arbitrage is only the baseline business case for storage. The higher-margin opportunity sits in ancillary services that keep the grid stable as thermal plant retires. Historically, the mass of spinning turbines in fossil-fuel power stations provided physical inertia that resisted rapid frequency changes. As asynchronous wind and solar grow, system inertia falls, making grids more fragile.

Batteries can respond quickly, but they provide synthetic inertia, reacting after a frequency deviation begins. High-Density Hydro uses heavy Francis turbines. When operating, its spinning mass provides immediate physical inertia. The UK system operator has explicitly recognised the value of stability services in its approach to inertia procurement, including the “Stability Pathfinders” described in National Grid ESO’s stability services note. Market-level interpretation and contract implications for storage are discussed in Modo Energy’s analysis of stability pathfinders.

The commercial implication is revenue stacking. The model described is that an HD Hydro asset can earn wholesale arbitrage while also securing longer-term stability contracts, commonly described as six- to 10-year arrangements, for providing physical inertia. The operational detail that enables this is the ability to keep turbines synchronised, including through clutch systems, even when not discharging energy, so that inertia services can be delivered independently of energy dispatch.

- Wholesale arbitrage, capturing daily spreads by absorbing excess generation and discharging into peak demand.

- Stability services, monetising physical inertia through contracts designed to stabilise low-carbon grids.

The January 2026 Inflection Point at Cornwood

Institutional capital rarely treats novel infrastructure as bankable without operational proof. RheEnergise reports that this threshold was crossed on 27 January 2026, when it commissioned its first 500kW High-Density Hydro demonstrator at the Sibelco Cornwood kaolin mine in Devon, operating at predicted power under real industrial conditions, as set out in the company’s press release. The deployment is also covered in sector reporting on the site’s industrial application in International Mining.

For RheEnergise, this demonstrator is presented as the catalyst for commercial-scale utility projects in the 10MW to 100MW range. For investors, the credibility signal is not just that the fluid behaves as modelled, but that the processing plant and the operational system can run consistently in a real-world setting, supported by 42 Technology’s description of the manufacturing approach in its Cornwood insight.

Curtailment, Congestion, and the £16bn Prize

The Cornwood milestone arrives at a sensitive moment for the UK power market. Curtailment has become a costly symptom of grid constraint. When transmission capacity cannot absorb peak generation, the system can end up paying wind to turn off while paying gas in another region to turn on, a market failure that wastes clean electricity and pushes costs onto consumers.

Industry analysis and policy commentary point to rising volumes of discarded wind energy, including the UK-focused discussion in the Renewable Energy Foundation’s note on discarded wind energy. Academic research on power market and system implications is also set out in Cambridge material such as EPRG Working Paper 2503.

RheEnergise argues that locational agility changes the storage proposition. Using GIS mapping, it reports identifying more than 6,500 viable deployment sites across the UK, discussed in a separate company note on market potential in its BEIS and EEF-related press release. The investment case presented is that High-Density Hydro can be placed close to constrained nodes, absorbing excess wind during congestion and dispatching during evening peaks, thereby reducing the effective curtailment penalty and improving system efficiency.

The Infrastructure Alpha Proposition

Return to the hypothesis. The energy sector is caught in a reinforcing cycle: renewable cost competitiveness is eroding the economics of legacy fossil generation while geopolitical risk is making fuel dependence a strategic liability. In this environment, the scarce asset is not intermittent generation. It is dispatchable flexibility that stabilises the system, reduces curtailment, and improves energy security.

High-Density Hydro is positioned as a response to that scarcity, combining long asset life, low supply-chain exposure, and an ability to monetise both energy shifting and physical inertia. With the January 2026 Cornwood commissioning framed as a de-risking milestone, the technology is being presented as a bankable category for allocators operating in a long-duration storage market projected towards $4trn. The deeper point for capital allocation is that the next phase of the transition will be won not only by building generation, but by financing the buffering systems that make a high-renewables grid reliable, investable, and secure.

You may have an interest in also reading…

Turning Promises Into Reality – The Business Case for Gender Equality in Achieving the SDGs

By Paula Tavares and Otaviano Canuto As world leaders gathered this month for high-level talks at the 74th United

Iraqi Government & Industry Gather to Drive Oilfield Optimisation in Iraq

Under the patronage of HH Sheikh Mohammed Bin Maktoum Bin Juma Al Maktoum, the fourth Iraq Mega Projects Conference and

Poland Votes: PiS Stranglehold on Power in the Balance

Clutching at straws. With the slimmest of margins, voters in Poland opened a narrow path for the pro-EU opposition to