Otaviano Canuto, IMF: Trade Opening Could Be a Source of Growth for Brazil

International trade has undergone a radical transformation in the past decades as production processes have fragmented along cross-border value chains. The Brazilian economy has remained on the fringes of this production revolution, maintaining a very high density of local supply chains, the flipside of which has been low levels of trade integration with the rest of the world. Such option has meant opportunity costs in terms of foregone productivity gains and a reversal might contribute to restoring economic growth in that country.

International trade has undergone a radical transformation in the past decades as production processes have fragmented along cross-border value chains. The Brazilian economy has remained on the fringes of this production revolution, maintaining a very high density of local supply chains, the flipside of which has been low levels of trade integration with the rest of the world. Such option has meant opportunity costs in terms of foregone productivity gains and a reversal might contribute to restoring economic growth in that country.

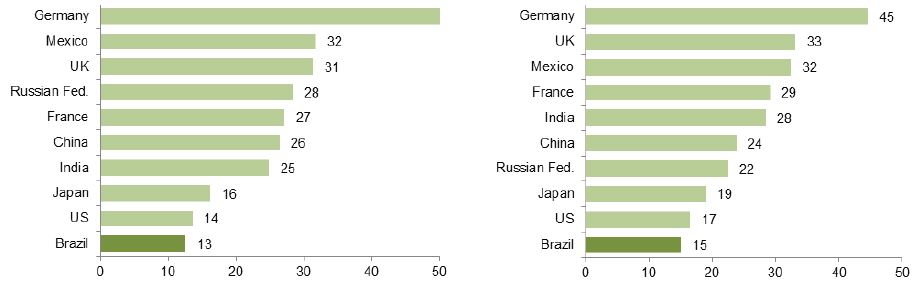

In terms of foreign trade, Brazil is a relatively closed economy. While the Brazilian economy is financially integrated abroad and relatively open to foreign direct investment, it is closed in terms of foreign trade. Its degree of trade integration as measured by ratios of exports and imports to GDP rank the country among the closest economies (see figure 1).

As one can see in the graph, Brazil’s size does not explain its low level of trade penetration: “Even among the six countries with a larger economy than Brazil, the average trade-to-GDP ratio is 55 percent. In fact, just looking at size of GDP we would expect Brazil’s trade to stand at 85 percent of GDP, three times the observed 28 percent.”

“It looks hard to state that the recent performance and macroeconomic prospects of Brazil can be predominantly explained by the commodity price super-cycle.”

As demonstrated by Canuto, Fleischhaker, and Schellekens (2015b), even when taking into account other dimensions of country size (surface area and population) and other features often associated with trade openness (urbanisation rate, manufacturing share in GDP) still Brazil stands out as a case of relatively low trade integration.

Brazil’s trade figures contrast with those of its peers and reflect the fact that the country’s economy remained relatively segmented from a deep transformation that took place in the global economic geography in the last decades. From 1990-2008, world trade volume expanded at a pace of six percent annually, well above the global real GDP growth of 3.2 percent a year over the same period. To a large extent, such high elasticities of trade with respect to global growth was the expression of an underlying mutation taking place in production processes and in the global economic geography.

A Reshaped Global Economic Geography

In recent decades, international trade has gone through a revolution, with the wide extension of the organisation of production in the form of cross-border value chains. This extension was a result of the reduction of tariff and non-tariff barriers, the incorporation of large swaths of workers in the global market economy in Asia and Central Europe, and technological innovations that allowed modularisation and geographic distribution of production stages in a growing universe of activities. International trade has grown faster than world GDP and, within the former, the sales of intermediate products has risen faster than the sale of final goods.

Figure 1: Trade Penetration. Source: Canuto, Fleischhaker and Schellekens (2015a).

Selected large Economies: Exports as percent of GDP (2013) (left) and Imports as percent of GDP (2013) (right).

The geography of industrial production has changed dramatically, with unskilled labour-intensive sectors moving out of advanced economies rapidly. Although the “hollowing out” of such jobs in advanced economies may have been, to a greater or lesser extent, determined by biases in trends of technological progress, the transfer of unskilled labour-intensive segments of supply chains has been part of the explanation. On the other side of such transfers, low-income countries have experienced rapid economic growth processes stemming from the structural transformation that has resulted from the large-scale migration of workers from subsistence to modern tradable activities.

Sharp changes in relative prices in the global economy have accompanied this process. While labour prices fell – as well as prices of manufactured products, according to their labour intensiveness – prices rose for natural resource-intensive goods, following an increase in demand coming from economically-growing low-income areas.

The logic of value chains was also extended to sectors beyond manufacturing. Producers are opting for less self-sufficient, in-house capacities, choosing instead to subcontract activities that are not essential to their business. This is also one reason for the expansion of services in GDP accounting in recent decades. Commodity chains have increasingly relied on sophisticated services both upstream and downstream. The content of services embedded in industrial products has also increased. Additionally, technological innovations have increased the marketability of various services, as expressed in the growth of international trade in services.

The opportunities and challenges of the international industrial division of labour are reconfigured in this new world of cross-border value chains. For low-income economies, one can say that it has become relatively easier – especially for small countries – to increase their local industrial production, since joining the market through labour-intensive segments of existing chains allows them to circumvent the limits of (a lack of) scale and sophistication in local markets. Nevertheless, such entry is volatile and can easily be undone and relocated soon after any adverse signal comes out. This process of entry – with easy exit – corresponds to a window of opportunity for local accumulation of skills and a leap forward.

For high- and middle-income economies, in turn, it has become increasingly difficult to maintain competitiveness in those segments. It should also be noted that some technological trajectories currently in early stage – such as 3D printing – may require the substitution of qualified for unqualified labour in a wide range of segments of existing chains, partly reversing the spatial dynamics described above.

Middle-income economies are also facing a new landscape in other aspects. On the one hand, technological spill overs, productivity increases, and wider market access are now facilitated via entry at points that require intermediate sophistication levels within existing value chains. On the other hand, the consolidation of existing value chains raises the stakes in terms of the competition for core positions. For consolidated and mature branches, creating new chains and challenging established ones is the only alternative.

The Flipside of Low Trade Integration

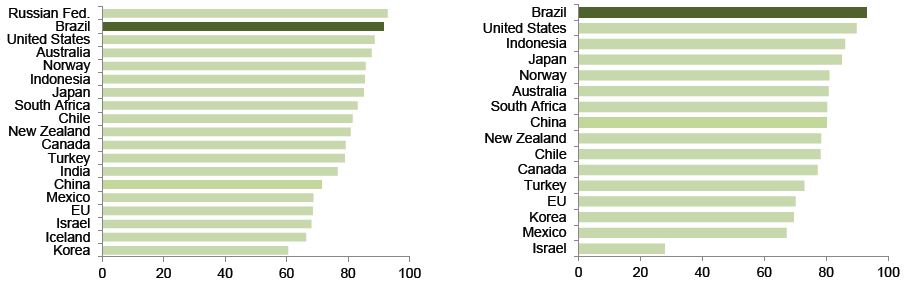

Value-added trade statistics give a view of how Brazil maintains a level of density in its chains of domestic industrial production above what one would expect in the case of a middle-income country. Figure 2 shows ratios of value added relative to gross exports in various countries. While the weight of commodities partly explains why the ratio is so high in the case of the total export bill (left side), the index is also very high in manufacturing branches (93 percent), as illustrated on the right side of figure 2.

The high level of domestic value added in exports shows that the fragmentation of the production process along cross-border value chains has largely bypassed Brazil. Geographic distances from advanced economies – reduced but not completely annulled by revolutions in transport and communications – partially explain why Brazil’s production-chain density remains well above its notional counterfactual. After all, in many branches, cross-border production chains are regional and focus on dynamic markets of high-income countries (Asia, Europe, and North America).

However, the Brazilian deviation from its notional density levels also reflects trade and local-content policies which have remained more prevalent than in most of Brazil’s peer countries including China (World Bank, 2014). Likewise, Brazil’s precarious logistics and high transaction costs in trading across borders are incompatible with the logic of cross-border value chains.

Figure 2: Domestic value added as percent of exports. Source: Canuto, Fleischhaker and Schellekens (2015a).

Eliminating these factors would reduce the deviation between actual and notional densities, leading to a corresponding closure of less competitive production chain segments and a rise in import substitution. On the other hand, the businesses left standing would be more competitive and final products would have lower production costs and/or higher quality. Furthermore, in dynamic terms, such as when the adjustment implications of changing chain densities unfold, gains would increase by dint of greater technological spill overs and market extension relative to the current scenario.

Brazil has remained outside the process of cross-border production fragmentation. The technological dynamics and cost reductions in the global economy due to the increase in value-chain fragmentation have been significant, increasing the opportunity cost of the ongoing gap between actual and notional production densities.

There are few exceptions, like Embraer, which operates in the centre of its own global value chain. The automotive Mercosur regional network also seems to escape the rule, but it is in fact the extension of a chain with a low degree of integration with the rest of the world. High coefficients of value-added to exports demonstrate local levels of production far above what one would expect for a middle-income economy with average levels of technological sophistication.

Opening Up to Support Brazil’s Growth Agenda

Opening up and integrating more deeply in global value chains would result in the closure of uncompetitive production chain segments and their substitution with imports. The surviving businesses would be more competitive due to access to imported inputs, allowing them to create products of lower costs and higher quality. Furthermore, in dynamic terms, integration in global value chains would allow scarce domestic resources such as skilled labour to be reallocated to the most productive firms and activities, increasing overall productivity.

In an economy with a propensity to face skilled-labour shortages and a generalised aspiration of rising worker purchasing power, productive activities would be strengthened by the availability of cheaper local consumer goods and equipment, as wage and investment costs would be lower. That would facilitate the creation of global value chains with a core in the country in natural resource-associated industries, where there clearly exists a greater scope.

Brazil’s immersion into global value chains would allow the country to leverage its comparative advantages which clearly exists in natural resource-associated industries but which could also emerge in specific activities in manufacturing or services, once industries have access to cheaper inputs.

As productivity gains from participation in global production networks increase, so does the opportunity cost associated with the ongoing closed-ness of the Brazilian economy. The alternative approach, vertically integrated supply chains behind protectionist barriers, is likely to be futile in the longer term. Despite rising trade barriers, Mercosur’s coefficient of imports from China has continued to increase in recent years (World Bank, 2014). Private investors understand this, as they shy away from activities which are viable only under permanent protection.

Of course, public policy support remains essential. However, this support should be more horizontal in nature, rather than further encouraging the ongoing high density of production chains and perpetuating the extraordinary closed-ness of the Brazilian economy.

About the Author

Otaviano Canuto is the executive director at the Board of the International Monetary Fund (IMF) for Brazil, Cabo Verde, Dominican Republic, Ecuador, Guyana, Haiti, Nicaragua, Panama, Suriname, Timor Leste and Trinidad and Tobago. Views expressed here are his own and do not necessarily reflect those of the IMF or any of the governments he represents.

Otaviano Canuto is the executive director at the Board of the International Monetary Fund (IMF) for Brazil, Cabo Verde, Dominican Republic, Ecuador, Guyana, Haiti, Nicaragua, Panama, Suriname, Timor Leste and Trinidad and Tobago. Views expressed here are his own and do not necessarily reflect those of the IMF or any of the governments he represents.

Mr. Canuto has previously served as vice president, executive director and senior adviser on BRICS economies at the World Bank, as well as vice president at the Inter-American Development Bank. He has also served at the Government of Brazil where he was state secretary for international affairs at the ministry of finance. He has also an extensive academic background, serving as professor of economics at the University of São Paulo and University of Campinas (UNICAMP) in Brazil.

The views expressed are those of the author and do not necessarily reflect the views of the IMF.

References

Canuto, O, Fleischhaker, C, and Schellekens, P (2015a). The cost of Brazil’s closed economy, Financial Times – January 14.

Canuto, O, Fleischhaker, C, and Schellekens, P (2015b). The curious case of Brazil’s closed-ness to trade, World Bank Policy Research Working Paper 7228 – April.

World Bank (2014). Implications of a changing China for Brazil: A window of opportunity? – World Bank.

You may have an interest in also reading…

Brazil: Arrest of Fraudsters Decreases Deforestation Rate

One man can make a difference. Since Brazilian authorities in August 2014 issued an arrest warrant and forced Ezequiel Antônio

Phased Time Table for Liquidity Coverage Ratio

A Basel Gift for EMEA? The Basel Committee governing body endorsed the revised Liquidity Coverage Ratio (LCR) on 6th January

NSE’s Resilience Blueprint: Scale, Trust, And Sustainable Market Growth

In an era where market participation is widening, technology loads are compounding, and volatility can arrive without warning, the National