IFC: The Art and Science of Benefits Sharing

Non-renewable natural resource projects – that is oil, gas, and minerals – are usually seen as part of a nation’s wealth. Accordingly, their use for the long-term sustainable development of a country is a prime objective of any legitimate government. The role of government in establishing a framework to manage and invest revenues derived from oil, gas, and mining projects is crucial to ensure that the sector contributes positively to sustainable development.

The fair sharing of the net benefits of natural resource developments, i.e. benefits in excess of costs, between government, investors, and other stakeholders, is important to ensuring that projects and their positive impacts are durable and resilient to change over time. Investors, governments, communities, and other stakeholders share a strong interest in a reasonable distribution of benefits.

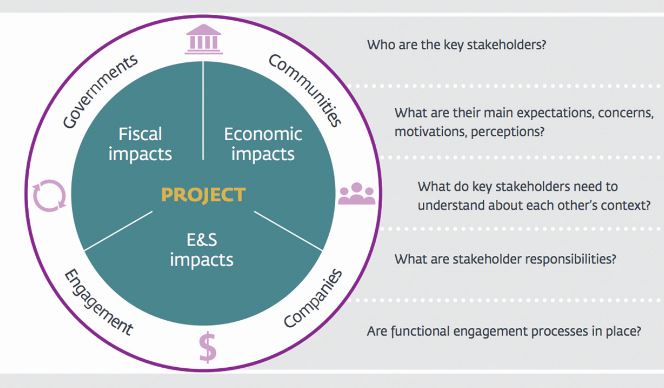

Figure 1: IFC Stakeholder Framework and Areas of Project Impact

Most private-sector investors realise that projects that are good for the host country and communities, and whose benefits are perceived to be shared reasonably, are less likely to face disruption, renegotiation, or even expropriation. Terms and conditions that deliver shared benefits are more likely to survive changes in societal expectations, political regimes, or market disruptions and reward investors over the long run for the capital and skills deployed and the risks taken. As developers better understand this connection and experience stakeholder challenges and even social conflict, their interest in a dialogue to create shared benefits and value is growing.

“High levels of cross-shareholding and concentrated ownership in the banking sector and the overall market means related-party transactions, particularly lending, remain a key challenge.”

The International Finance Corporation (IFC) recognises the important technical and economic differences between the oil, gas, and mining industry, and understanding project and country specifics is crucial. Nonetheless, the three sectors share certain characteristics that distinguish them from any other industry, including high degrees of uncertainty and risk (geological, exploration, technical), price volatility, long project lead times with significant capital expenditures up front, and often a large footprint with environmental social effects.

These factors profoundly influence how, when, and to whom benefits and costs accrue and the process by which a durable benefit sharing agreement across stakeholders can be reached. In this light, an overall approach to assessing benefit sharing that covers oil, gas, and mining is proposed.

The IFC Approach

Guided by its development mandate, IFC looks carefully at an extractive project’s potential to contribute to a country’s economic and social development, and how project costs and benefits will be distributed when considering a potential investment. IFC also reviews the profitability of the proposed investment and the underlying economics of the project to make a financial decision on whether or not to put its own capital at risk. These factors are considered throughout the life cycle of an IFC investment along with other key criteria that determine IFC’s engagement, including IFC’s prospective role and value addition, strategic fit with World Bank Group country engagement, and institutional priorities as well as general compliance with policies.

A full investment cycle from early review to investment and eventual exit from a project consists of many steps and can unfold over many years, especially in the natural resource sector, where projects have long lead times and face high levels of uncertainty.

An assessment of prospective project development impacts and benefit sharing is an integral part of IFC’s investment appraisal approach. A benefit-sharing assessment typically considers:

- The country and community context, the processes by which sharing was determined and how proceeds are managed and used;

- Environmental and social issues and risks, mitigation measures, and opportunities to enhance outcomes beyond mitigation as well as stakeholder expectations and concerns;

- The overall distribution of diverse, uncertain and sometimes unquantifiable benefits and costs across affected stakeholders, using IFC’s stakeholder framework (Lysy, Bouton, Karmokolias, Somensatto and Miller 2000). The timing of these, which are grouped by financial, economic, environmental and social impacts, is also reviewed.

IFC will assess the broader context, starting with the role of the natural resource sector in the country, its economic contribution to date, its prospects, and government vision for its future. Understanding country and sector governance issues and capacity, as well as expectations and concerns by host governments can help determine whether a project will likely contribute to sustainable development.

The assessment includes a review of “traditional corruption”, as it may occur during the acquisition of mineral rights. IFC looks carefully at the private investors in projects it is asked to support. This is done both to satisfy IFC of their integrity and the possible presence of political insiders whose presence may be an indication of a sweetheart deal. Where corruption is a factor, IFC will not invest.

Poor country and sector governance often poses an impediment to the transformation of resource wealth into sustainable development. The engagement of the World Bank (WB), the International Monetary Fund (IMF) and other development actors in a country will help judge the risks along the value chain and verify a country government’s commitment to reform and change.

IFC reviews ex ante the risks weak governance poses to key project development benefits. In general, IFC makes careful judgments about whether it should support natural resource projects where governance is weak but development pay-off may be significant, such as supply chain development, shared infrastructure, investment in local communities. IFC also considers project-specific arrangements that can help reduce governance risks, such as technical assistance to build local capacity in revenue management, enhance transparency and accountability. IFC supports the global transparency agenda and initiatives like the Extractive Industries Initiative (EITI). Also, IFC has taken the lead among other development finance institutions by championing full revenue and contract disclosure in its projects.

Understanding who the key stakeholders are, what their aspirations, concerns, and expectations of a project are, and what drives these is important for judging the reasonableness of a benefit sharing settlement and its legitimacy and durability over time. If project realities are not commensurate with stakeholder perceptions – be they informed or not – a project may be at risk. Typically, key stakeholders include the government (federal and sometimes subnational), citizens at large, affected communities, and investors.

As part of its due diligence before investing and part and parcel of project supervision, IFC through its performance standards requires a stakeholder analysis and engagement plan for the range of stakeholders that are interested in the project. Stakeholder engagement plans must be scaled to the risks and impacts, the development stage of the project and tailored to the characteristics and interests of affected communities.

Stakes in project may go much beyond the immediate project boundaries and the directly affected communities, and they can be high. Especially, projects that are big in scale and are transformational for an entire country or even region, national expectations and concerns will inform project-level dynamics and vice-versa.

At the core, IFC assesses a project’s costs and benefits and their distribution across stakeholders, in three broad, overlapping areas of impact. IFC considers a variety of questions as part of its due diligence and decision-making process:

- Fiscal impacts: How are the net financial benefits of projects shared through profit sharing, taxation, and in other ways – at both the national and subnational levels of government and with communities and others?

- Economic impacts: What additional economic costs and benefits are generated and shared, such as jobs and training, the introduction of technologies, spending with local suppliers, investment in infrastructure, the supply of energy, such as oil, gas, coal and electricity, or the supply of other raw materials at competitive prices to local industry and households?

- Environmental and social impacts: What are the positive and negative environmental impacts and risks that the project brings and who bears them? How do impacted communities, including vulnerable groups within communities, gain or lose from the development in other ways?

IFC Experiences and Lessons Learned

As both a development institution and an investor, IFC is in a unique position to simultaneously share the perspectives of investors, host countries, and other stakeholders. As a result of balancing these dual roles over many years, through commodity price cycles and industry change, a number of lessons have emerged that have a bearing on how to assess and secure a durable benefit-sharing arrangement:

1. Uncertainty is a key feature throughout the project life cycle

A project’s expected business outcomes and performance over time are exposed to many uncertainties. The future values of key drivers of project performance, such as costs of production and commodity prices, are uncertain and can be volatile. Even the scale and quality of a resource may not be fully known until late in the development and its extraction. And there may be substantial technical and production challenges that need to be addressed.

Projects may require many billions of dollars, may take years to come to fruition and many more to generate a financial return once operational. Against this backdrop, the planning of programs intended to benefit communities may be difficult, given business and other uncertainties.

Government policies and regulations can change and other political events may have major impacts on a project’s success and commercial viability. Tax frameworks and agreements and their impacts on projected benefit sharing that seemed reasonable at the outset of a project may look very different in the future. For example, much-higher-than-expected commodity prices over the last decade boosted the profitability of natural resource projects and companies. A number of governments came to believe they were not receiving a fair share of project benefits because their incomes from taxes did not increase in parallel – partly because tax structures and agreements were not designed to cope with these changes.

The considerable deterioration in prices for various commodities in the recent past, as well as the notable price volatility generally seen during the last years, has changed the conversation again, bringing into relief the uncertainty that medium- to long-term investors and governments face in this sector.

2. Every project is unique

Individual projects vary greatly in their size and life cycles, the richness of the resource, ease of access, cost of extraction, profitability, and impacts on people and the environment. Oil and gas is a different business from mining. However, gas is also very different from oil, and mining projects vary greatly from one another.

In regulating the natural resource sector, governments must strike a balance between accommodating the special circumstances of projects and maintaining a transparent, standard, and manageable regulatory framework and a bureaucracy that supports it. The way a project is treated and perceived depends on its host country and community context, the present and future economic role of the natural resource sector, and the government’s vision for it as an engine for sustainable development.

Investors seek acknowledgement for the uncertainty and unique project circumstances they face and value stability of the arrangements that govern their obligations to the government and other stakeholders. Especially for megaprojects, investors and governments may enter negotiations about specific aspects as regards project development and benefit sharing. While deal-by-deal negotiation allows for greater tailoring to project specifics, legitimacy rests heavily on transparency of process, symmetry in the access to information, and technical know-how and capacity. This may not be achieved in many weak governance countries.

3. Government policy impacts benefit sharing

Governments face multiple competing demands and the policy objectives they set impact benefit sharing—including whether, when, and how to develop their natural resources. Although the overriding objective of most governments is to ensure their country benefits to the greatest extent from its natural resources, there are many different ways they may try to ensure this. Government commitment to transparency and accountability, due process and prudent public financial management are key.

Good policy does not necessarily require governments to maximise the net revenue they receive from every project. The benefits of offering standard terms and conditions may outweigh the costs and complexity of trying to implement a more sophisticated tax system or setting terms and conditions project by project. New, emerging countries may be best served by setting relatively attractive terms to encourage a steady flow of new investment. It may also be an appropriate long-term strategy for building a robust, lasting industry, as some of the most important, resource-producing countries, such as Australia, Canada, Chile, and Peru demonstrate.

Governments may accept less tax income in return for investors helping them achieve other development objectives. For example, investors may be expected to increase local procurement and skills development, build, manage, and provide affordable access to infrastructure (power, rail, roads) for use by others, or process production locally rather than export raw materials.

Governments play an important role in providing an enabling environment for private-sector actors so that natural resource projects can link into the local economy and generate benefits for as long as resources are economically recoverable.

4. Perceptions and expectations matter

Diverse stakeholder groups have different perceptions and expectations about natural resource projects and their potential impacts. In particular, countries and communities with little experience developing natural resource projects may have difficulties to fully understand all of the issues, including the scale and nature of future impacts. Even when projects have been constructed and in operation for some time, it can be difficult to fully capture the economic and social impacts that have accrued over decades. Many older projects lack baseline data which can further impede tracking and may breed distrust of company practices and government policies.

Expectations and perceptions by host communities and other affected stakeholders will have a bearing on project success. Stakeholders are unlikely to share equal access to information or understanding of a project’s fiscal, economic, social, and environmental effects and impacts. Transparency and access to information are essential to manage misperceptions and enforce mutual accountability among stakeholders. In IFC’s experience, imbalance of information coupled with poor stakeholder engagement can derail an otherwise healthy project. Proactive management of diverse local expectations via honest dialogue about benefits, costs, risks, and mitigation measures can help build trust. Ideally, this creates a platform to cooperatively plan strategies to smooth costs and benefits across constituencies.

5. Processes are important

The processes by which benefit sharing is determined directly influences public perceptions about the reasonableness of the distribution of costs and benefits. This starts with how contracts were awarded, how environmental and social impacts are monitored, how affected communities are consulted to the collection and use of fiscal revenues for the economic development of the country. Transparency of processes along the value chain is important for creating accountability of key actors by enabling access to information and a better understanding of the project benefits and costs.

A process that is perceived as opaque and not inclusive can generate suspicion and negatively impact a project, as stakeholders may persistently challenge the arrangement, including any proclamations about net benefits. Even if company and government agree on what they view as a reasonable split over time, an uninformed, excluded electorate may at some point decide to change the government and the project terms as a result.

There has been a welcome trend of greater transparency about natural resource projects – including revenue flows, contract terms, and reporting to communities. But for benefit-sharing arrangements to be durable, the process must be consultative and participatory. Consultation with affected communities should start early – even during the exploration phase – and should be iterative throughout a project’s life, taking into account dynamic, environmental, and social risks. Communities must be able to register their grievances and see them addressed. Resilient agreements are those that are supported by affected stakeholders who have meaningfully participated and can influence decisions about project aspects that affect them. This may relate to land access, water management, immigration, and infrastructure development. Broad community support is central to managing project risks over time.

6. Fiscal benefits are only one part of a project’s costs and benefits

Benefit-sharing discussions usually focus on the distribution of the financial (fiscal) benefits and costs of the project between private investors and the central government. However, there is a broader range of other non-fiscal costs and benefits that need to be considered to understand the full range of impacts and opportunities of natural resource development

For example, communities are immediately – and sometimes negatively – impacted by projects near them. Their lives will be impacted in varying ways, and different groups within these communities will fare differently. In addition to tax revenue, projects may bring jobs, infrastructure, local sourcing, and competitive supplies of energy and other materials that may benefit the country as a whole or particular regions and sectors. Projects will also have environmental impacts that need to be assessed and tracked.

7. The arts and science of benefit sharing

For IFC, determining whether a project has a reasonable balance of benefits and costs depends on an informed, overall judgment based on expert, multi-disciplinary input and review. From a development and commercial perspective, IFC tests for a range of outcomes, and thresholds exist with respect to financial, economic, environmental, and social considerations. For a project to be supported, it must demonstrate, at minimum, that it is profitable, that its economic benefit to society and economic return on investment is positive and greater than its financial return, that it is compliant with IFC Performance Standards (IFC PS), and that affected communities are broadly supportive.

However, given the diversity of national contexts, geographical potential, and business arrangements, IFC has found that there is no single blueprint that can be used to determine what equitable sharing looks like. In practice, investigation and professional judgment from a diverse team of experts, representing specialty areas such as finance, engineering, environmental and social, economics, and law, to name a few, is required.

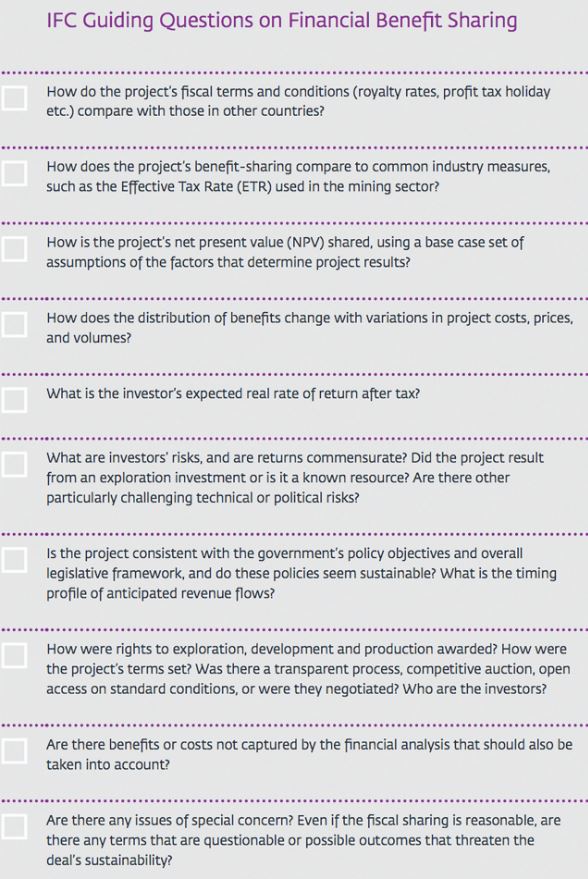

Often precise measures or cut-offs between what is acceptable, for example with respect to the fiscal sharing between the public and private sector, and what is not, are at best imperfect and at worst misleading. Rather, it is important to contextualise and assess fiscal sharing against other project characteristics and drivers, stakeholder expectations and concerns (see Figure 1), and potential impacts. Even when the overall judgment is that there is a balance of costs and benefits at a particular moment in time, circumstances can change and present risks that need to be addressed and managed carefully.

You may have an interest in also reading…

International Property Show Grows 25% – 300 Exhibitors from 80 Countries to Participate from 8 to 10 April in Dubai

Middle East’s built assets to rise by 63% to US$ 8.7 trillion by 2022 Dubai, UAE, 8 January 2014: The

CFI.co Meets Chitra Ramkrishna

Ms Chitra Ramkrishna is the Managing Director and Chief Executive Officer of the National Stock Exchange, the world’s second largest

Wangari Maathai: Attaining Peace that Endures, One Tree at a Time

A young Kenyan girl named Wangari Maathai was sent by her mother to fetch some fresh water. As she reached